Classifying insurance funds in QuickBooks is a critical task for businesses to ensure accurate financial tracking and reporting. Insurance funds, which may include premiums, claims, or reserves, need to be categorized correctly to maintain clear records and comply with accounting standards. In QuickBooks, this involves setting up dedicated accounts for different types of insurance, such as liability, health, or property insurance, and consistently assigning transactions to these accounts. Proper classification not only simplifies tax preparation and audits but also provides valuable insights into insurance-related expenses and liabilities, helping businesses manage their financial health effectively.

Explore related products

What You'll Learn

![]()

Setting up insurance fund accounts

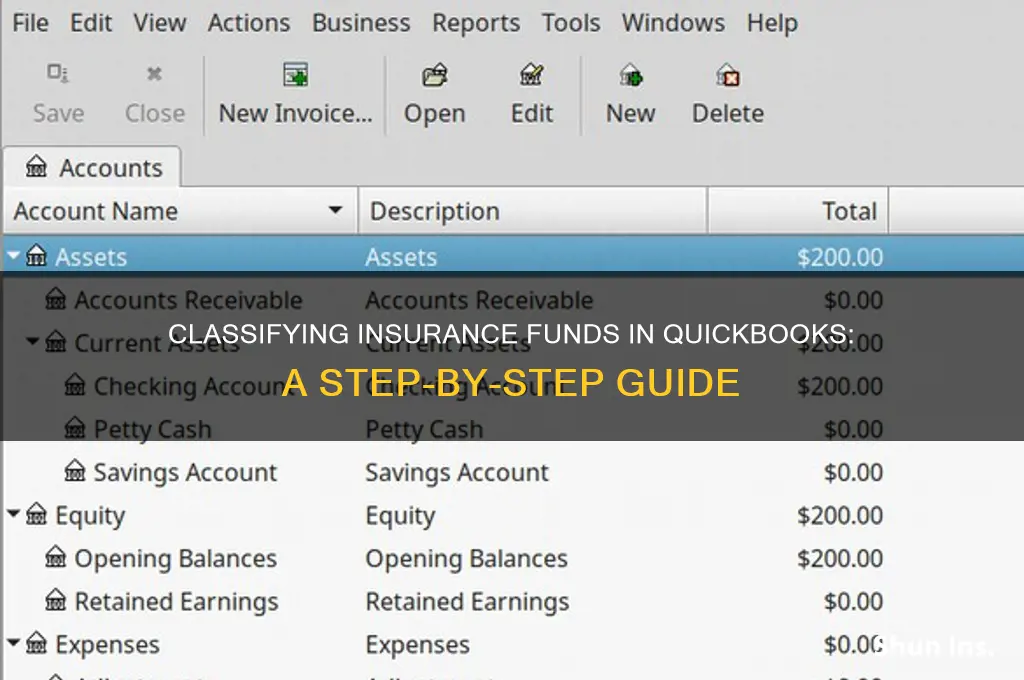

Classifying insurance funds in QuickBooks requires a structured approach to ensure accurate financial tracking and reporting. Setting up dedicated accounts for these funds is the foundational step, as it allows for clear differentiation between premiums, claims, and reserves. Begin by identifying the types of insurance funds your business manages, such as health, liability, or property insurance. Each type may necessitate separate accounts to maintain transparency and compliance with accounting standards. For instance, create distinct accounts for "Health Insurance Premiums Payable" and "Liability Insurance Reserves" to avoid commingling funds and simplify reconciliation.

Once you’ve identified the necessary accounts, navigate to the Chart of Accounts in QuickBooks and select "New" to create them. Use clear, descriptive names that align with accounting best practices, such as "Insurance – Health Premiums" or "Insurance – Workers’ Compensation Reserves." Assign each account to the appropriate category, typically under "Other Current Liabilities" or "Other Assets," depending on the nature of the fund. For example, prepaid insurance premiums should be classified as an asset until they are expensed over time, while accrued claims liabilities belong under liabilities. Consistency in naming and categorization ensures that reports accurately reflect the financial health of your insurance funds.

A critical aspect of setting up insurance fund accounts is determining the account type—whether it’s a bank, credit card, or other liability account. For funds held in escrow or as reserves, use liability accounts to reflect the obligation. Conversely, prepaid insurance accounts should be set up as asset accounts to represent future benefits. QuickBooks allows you to customize account details, such as tax lines and descriptions, which can be tailored to align with insurance-specific reporting requirements. For instance, linking insurance expense accounts to the appropriate tax line ensures compliance during tax filings.

To maximize efficiency, consider leveraging QuickBooks’ sub-account feature for granular tracking. For example, under a main "Insurance Expenses" account, create sub-accounts for "Health Insurance," "Auto Insurance," and "General Liability." This hierarchical structure simplifies reporting and provides a detailed breakdown of insurance costs. Additionally, set up memorized transactions for recurring premiums or claims payments to save time and reduce errors. Regularly review and reconcile these accounts to ensure accuracy, especially when dealing with fluctuating premiums or claims activity.

Finally, integrate your insurance fund accounts with QuickBooks’ reporting tools to gain actionable insights. Custom reports, such as Profit & Loss by Class or Balance Sheet Detail, can highlight trends in insurance spending and reserves. For businesses with multiple policies or locations, use class tracking to allocate insurance expenses accordingly. By thoughtfully setting up and managing insurance fund accounts, you not only maintain compliance but also empower your business with data-driven financial decision-making.

AAA Life Insurance: Where is its Headquarters?

You may want to see also

Explore related products

![]()

Categorizing premiums and claims

Properly categorizing insurance premiums and claims in QuickBooks is crucial for accurate financial tracking and reporting. Premiums, the payments made to maintain insurance coverage, should be recorded as expenses. Create a dedicated expense account, such as "Insurance Premiums," under the "Insurance" category in your Chart of Accounts. This ensures clarity and simplifies tax deductions, as premiums are typically tax-deductible business expenses. For example, if your monthly premium is $500, record this as a $500 expense in the "Insurance Premiums" account, linking it to the appropriate payment method (e.g., bank account or credit card).

Claims, on the other hand, represent reimbursements or payouts from the insurance company for covered losses. These should be categorized as income or reductions to expenses, depending on the context. For instance, if a $2,000 claim is paid directly to a vendor for property damage, record this as a credit to the "Repairs & Maintenance" expense account rather than as income. This approach maintains the integrity of your profit and loss statement by offsetting the actual expense incurred. If the claim is paid to your business account, create an "Insurance Reimbursements" income account to track these funds separately.

A common mistake is treating all insurance-related transactions uniformly. Instead, differentiate between premiums (expenses) and claims (offsets or income) to avoid distorting financial statements. For example, recording a claim as income when it should offset an expense can artificially inflate revenue. Use QuickBooks’ class tracking feature to further categorize transactions by policy type (e.g., health, liability, property) or department, providing granular insights into insurance costs and recoveries.

To streamline this process, set up memorized transactions for recurring premiums and create itemized templates for claims. For instance, a memorized transaction for a quarterly $1,500 premium ensures consistency, while a claim template with fields for claim number, date, and amount reduces errors. Regularly reconcile these entries with insurance statements to catch discrepancies early. By maintaining this level of organization, you’ll not only comply with accounting best practices but also gain a clearer picture of your insurance financial landscape.

Finally, consider the tax implications of your categorizations. Premiums are generally deductible in the year paid, but claims may affect taxable income if not properly offset. Consult IRS guidelines or a tax professional to ensure compliance, especially for complex policies like workers’ compensation or health insurance. QuickBooks’ reporting tools can generate detailed insurance expense and recovery reports, aiding in tax preparation and financial analysis. With disciplined categorization, you transform insurance transactions from administrative burdens into actionable financial data.

Robo-Investors: Are Your Funds Insured?

You may want to see also

Explore related products

![Quick-Books Desktop Pro 2024- [CD VERSION]](https://m.media-amazon.com/images/I/61C880HLd1L._AC_UL320_.jpg)

![]()

Tracking policy expenses

Effective tracking of policy expenses in QuickBooks hinges on consistent categorization and leveraging the platform’s tools. Begin by setting up dedicated expense accounts for each policy type—health, auto, liability, etc.—to avoid commingling funds. For instance, create a sub-account under "Insurance Expenses" labeled "Health Insurance Premiums" to isolate costs. This granularity ensures clarity when generating reports or reconciling statements. QuickBooks’ class tracking feature further refines this process by tagging expenses to specific departments, locations, or policies, enabling multi-dimensional analysis. For example, assign the class "Corporate Office" to health insurance premiums paid for headquarters staff, while "Field Operations" tags cover remote teams.

A critical yet overlooked step is linking payments to their respective policies. When recording premium payments, use the memo field to note the policy number and coverage period (e.g., "Policy #12345, Jan-Mar 2024"). This practice simplifies audits and claim reconciliations. Additionally, attach digital copies of invoices or receipts to transactions via QuickBooks’ document management feature. For recurring expenses, automate entries using the memorized transactions tool, reducing manual errors and ensuring timely recording. For instance, schedule a monthly $500 payment to "General Liability Insurance" on the 15th of each month, tied to policy #56789.

While QuickBooks streamlines expense tracking, pitfalls abound. Avoid lumping all insurance costs into a single account, as this obscures financial insights. For example, bundling health and auto insurance under "General Expenses" complicates tax deductions and budget reviews. Similarly, resist the urge to backdate entries without proper documentation, as this distorts cash flow reports. Instead, use QuickBooks’ undo/redo functions to correct errors transparently. Regularly reconcile insurance accounts against carrier statements to catch discrepancies early—a quarterly review is ideal for most businesses.

Advanced users can enhance tracking by integrating QuickBooks with third-party apps like Bill.com for automated invoice processing or Expensify for receipt management. These tools sync data directly into QuickBooks, reducing manual input and improving accuracy. For instance, Expensify’s optical character recognition (OCR) technology extracts policy details from receipts, auto-populating QuickBooks fields. However, ensure app permissions align with data security protocols to prevent unauthorized access.

Ultimately, tracking policy expenses in QuickBooks requires a blend of structure, discipline, and technology. By customizing accounts, leveraging classes, and automating processes, businesses gain actionable insights into insurance spending. For example, a quarterly report comparing health insurance costs across classes might reveal opportunities to negotiate better rates for high-claim departments. Such visibility transforms insurance from a sunk cost into a manageable, strategic expense.

Securely Ship Your Art: Essential Tips for Insuring Valuable Pieces

You may want to see also

Explore related products

![]()

Reporting insurance fund balances

Insurance fund balances in QuickBooks require meticulous reporting to ensure compliance and financial clarity. Begin by designating a specific account for insurance funds, such as a "Other Current Asset" or "Other Asset" account, depending on the fund’s liquidity and purpose. For instance, if the fund covers short-term liabilities like worker’s compensation, classify it as a current asset. Conversely, long-term funds, such as those for property insurance, may be better suited as non-current assets. This classification directly impacts your balance sheet, so accuracy is critical.

Once classified, establish a routine for updating these balances. Monthly reconciliations are ideal, as they align with typical billing cycles for insurance premiums and claims. Use QuickBooks’ reporting tools to generate a "Balance Sheet Detail" report, filtering for the insurance fund account. Cross-reference this with external documents, such as insurance statements or premium invoices, to verify accuracy. Discrepancies, even minor ones, should be investigated promptly to prevent compounding errors in future reporting periods.

Transparency in reporting extends to notes and disclosures. QuickBooks allows for memo fields or attached documents, which are invaluable for explaining fluctuations in fund balances. For example, a sudden increase might be due to a prepayment for annual coverage, while a decrease could reflect a claim payout. These annotations provide context for stakeholders, including auditors or business partners, who rely on your financial statements for decision-making.

Finally, leverage QuickBooks’ automation features to streamline reporting. Set up rules to categorize insurance-related transactions, such as premium payments or reimbursements, directly to the designated fund account. Custom reports can be created to track fund balances over time, offering insights into trends and ensuring funds are adequately reserved. By combining manual oversight with automated processes, you maintain both precision and efficiency in reporting insurance fund balances.

Understanding Bricking: Cyber Insurance Risks and Protection Strategies

You may want to see also

Explore related products

![Quick-Books Desktop Pro 2024 - [CD VERSION] lifetime](https://m.media-amazon.com/images/I/614MqWtHp9L._AC_UL320_.jpg)

![Quick Books Desktop Pro Plus 2024 | LIFETIME Version | USB | Only for Mac [software_key_card]](https://m.media-amazon.com/images/I/41xG2aOWLLL._AC_UL320_.jpg)

![]()

Managing fund reconciliations

Effective fund reconciliation in QuickBooks hinges on meticulous categorization and consistent tracking. Begin by designating distinct accounts for insurance funds, such as "Insurance Premiums Payable" and "Insurance Claims Reserve." These accounts should align with your chart of accounts and reflect the nature of the funds—whether they are liabilities, assets, or expenses. For instance, premiums paid in advance can be classified as a prepaid asset, while claims reserves should be treated as a liability. This granular approach ensures clarity and compliance with accounting standards.

Reconciliation requires regular comparison of QuickBooks records against external statements from insurance providers. Start by verifying the opening balance of your insurance fund accounts at the beginning of the period. Cross-reference each transaction—premiums paid, claims received, or adjustments—with supporting documentation. Discrepancies, such as unpaid premiums or unrecorded claims, must be investigated promptly. QuickBooks’ reconciliation tools can flag unmatched entries, but manual scrutiny is essential to ensure accuracy. For example, if a claim payment appears in the insurer’s statement but not in QuickBooks, trace the transaction to its source and correct the oversight.

Automating certain aspects of reconciliation can streamline the process. Utilize QuickBooks’ memo field to tag transactions with policy numbers or claim IDs, facilitating quick reference during audits. Set up recurring journal entries for predictable expenses, like monthly premiums, to minimize manual input errors. Additionally, leverage third-party apps that integrate with QuickBooks to sync insurance data in real-time, reducing the risk of omissions. However, automation should complement, not replace, periodic manual reviews to catch anomalies that automated systems might miss.

A critical yet often overlooked aspect of fund reconciliation is maintaining an audit trail. Document every adjustment, correction, or reclassification with detailed notes in QuickBooks. This practice not only aids in troubleshooting but also demonstrates transparency during external audits. For instance, if a claim reserve is adjusted due to a change in policy terms, log the rationale and supporting documentation directly in the transaction record. Such diligence ensures that your QuickBooks data remains defensible and reliable.

Finally, establish a reconciliation schedule tailored to your insurance fund activity. Monthly reconciliations are ideal for accounts with frequent transactions, while quarterly reviews may suffice for less active funds. Consistency is key—irregular intervals increase the risk of errors compounding over time. Assign responsibility for reconciliations to a designated team member or external accountant, ensuring accountability. By treating fund reconciliations as a disciplined, structured process, you safeguard the integrity of your insurance fund management in QuickBooks.

Mastering ACORD COI Forms: How to Accurately Report Insurance Limits

You may want to see also

Frequently asked questions

To classify insurance funds in QuickBooks, start by creating a new bank account specifically for insurance funds. Go to the Chart of Accounts, select "New," choose "Bank," and name the account clearly, such as "Insurance Funds." This ensures proper tracking and separation from other funds.

Yes, you can categorize insurance premiums and claims separately by creating sub-accounts or using expense and income accounts. For premiums, use an expense account like "Insurance Premiums," and for claims, use an income account like "Insurance Claims Received." This allows for detailed reporting and analysis.

Reconcile insurance fund transactions by matching the account balance in QuickBooks to the actual insurance fund statement. Go to the Banking menu, select "Reconcile," choose the insurance fund account, enter the statement ending balance and date, and then match transactions. Mark cleared transactions and adjust for any discrepancies.

![QuickBooks Online for Beginners Bible Edition [2 Books in 1]: The Ultimate Fast Learning Guide for QBO, filled with Step-by-Step Illustrated Explanations, Practical Examples and Common Problem Solving](https://m.media-amazon.com/images/I/61WWhskpzAL._AC_UL320_.jpg)

![Quicken Classic Deluxe for New Subscribers| 1 Year [PC/Mac Online Code]](https://m.media-amazon.com/images/I/61ypcFpjCuL._AC_UL320_.jpg)