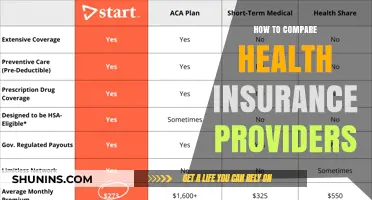

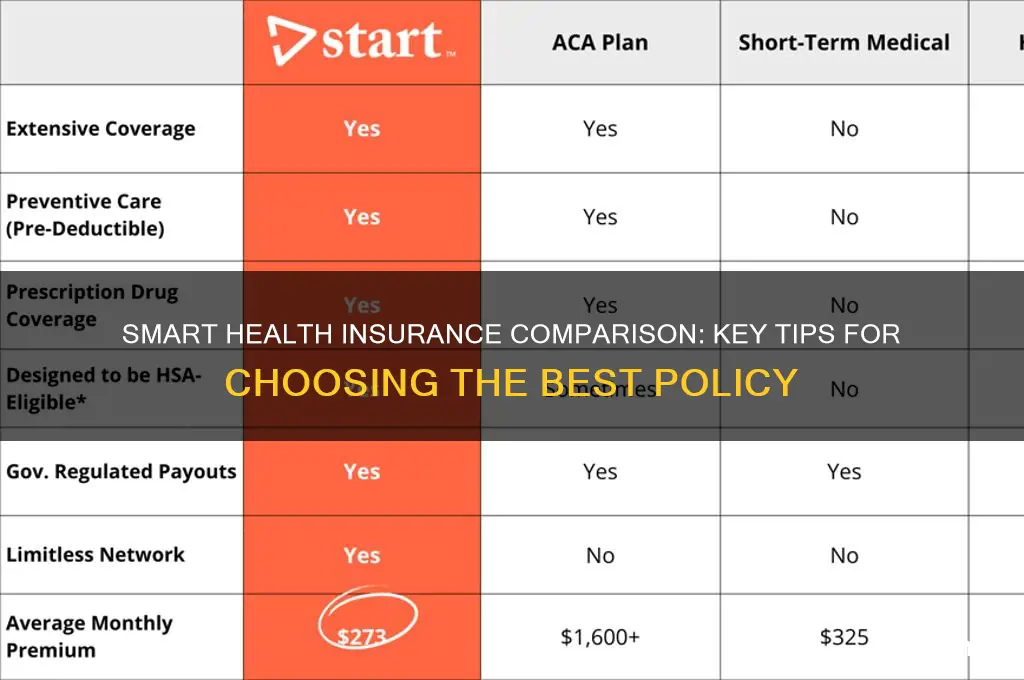

Comparing health insurance policies is a crucial step in ensuring you select the best coverage for your needs and budget. With numerous plans available, each offering different benefits, exclusions, premiums, and deductibles, it’s essential to evaluate them systematically. Start by identifying your healthcare priorities, such as prescription drug coverage, specialist visits, or preventive care, and then assess how each policy aligns with those needs. Compare key factors like monthly premiums, out-of-pocket costs, network restrictions, and coverage limits to determine which plan offers the most value. Additionally, consider customer reviews, provider reputation, and policy flexibility to make an informed decision that balances affordability with comprehensive protection.

Health Insurance Policy Comparison Characteristics

| Characteristics | Values |

|---|---|

| Coverage Type | - Individual/Family Floater - Group Health Insurance - Senior Citizen Plans - Critical Illness Plans - Maternity Plans |

| Sum Insured | - Amount of coverage provided for hospitalization and other medical expenses. - Choose based on age, health condition, and medical history. |

| Network Hospitals | - List of hospitals where cashless treatment is available. - Check proximity and reputation of network hospitals. |

| Premium | - Annual cost of the insurance policy. - Compare premiums for similar coverage across providers. |

| Deductibles | - Amount you pay out-of-pocket before insurance coverage kicks in. - Higher deductibles often mean lower premiums. |

| Co-payment | - Percentage of medical expenses you share with the insurer. - Common for senior citizen plans and specific treatments. |

| Room Rent Limits | - Maximum amount covered for hospital room rent per day. - Ensure it aligns with your preferred hospital standards. |

| Pre-existing Diseases Coverage | - Waiting period before pre-existing conditions are covered. - Varies across policies, typically 2-4 years. |

| No Claim Bonus (NCB) | - Discount on premium for claim-free years. - Accumulate over time, increasing savings. |

| Claim Settlement Ratio | - Percentage of claims settled by the insurer. - Higher ratio indicates better claim handling. |

| Waiting Periods | - Time period before certain benefits become available. - Varies for specific illnesses, maternity, etc. |

| Add-on Covers | - Optional additional coverage like critical illness, maternity, etc. - Customize policy based on individual needs. |

| Renewal Age Limit | - Maximum age up to which policy can be renewed. - Important for long-term planning. |

| Customer Service | - Reputation for customer support and claim assistance. - Check reviews and ratings. |

| Policy Exclusions | - Specific conditions or treatments not covered. - Understand limitations before purchasing. |

Explore related products

What You'll Learn

- Coverage Limits: Compare maximum payouts, exclusions, and coverage for hospitalization, treatments, and pre-existing conditions

- Premium Costs: Evaluate monthly/annual premiums, payment flexibility, and long-term affordability across policies

- Network Providers: Check in-network hospitals, clinics, and specialists included in each insurance plan

- Claim Process: Assess ease of filing claims, settlement time, and cashless facility availability

- Add-On Benefits: Compare additional features like maternity cover, critical illness, or wellness programs

![]()

Coverage Limits: Compare maximum payouts, exclusions, and coverage for hospitalization, treatments, and pre-existing conditions

Health insurance policies often tout comprehensive coverage, but the devil is in the details—specifically, the coverage limits. These limits dictate the maximum amount an insurer will pay for specific services, treatments, or conditions. For instance, a policy might cap hospitalization expenses at $500,000 per year, leaving you responsible for any excess costs. Understanding these limits is crucial, as they directly impact your out-of-pocket expenses during critical medical situations. Always scrutinize the fine print to ensure the policy aligns with your potential healthcare needs.

Exclusions are another critical aspect of coverage limits. Insurers often exclude certain treatments, procedures, or pre-existing conditions from their policies. For example, some plans may exclude coverage for cosmetic surgeries, experimental treatments, or chronic conditions like diabetes if diagnosed before the policy start date. A policy that excludes pre-existing conditions might leave you vulnerable to high costs if you require ongoing care. To avoid surprises, create a list of your current and anticipated medical needs and cross-reference it with the policy’s exclusion list.

Hospitalization coverage varies widely across policies, and the specifics matter. Some plans cover only the room and board, while others include intensive care unit stays, surgical procedures, and diagnostic tests. For instance, a policy might cover 100% of hospitalization costs up to a certain limit but require co-pays for extended stays. If you’re in a high-risk age category (e.g., over 50) or have a family history of severe illnesses, prioritize policies with robust hospitalization coverage and higher payout limits.

Treatment coverage is equally important, especially for specialized or long-term care. Policies may limit coverage for treatments like chemotherapy, physical therapy, or mental health services. For example, a plan might cover only 20 sessions of physical therapy per year, leaving you to pay for additional sessions. If you have a pre-existing condition or anticipate needing specific treatments, compare policies based on their coverage depth and flexibility. Look for plans that offer higher session limits or include alternative therapies like acupuncture or chiropractic care.

Pre-existing conditions are a common pain point in health insurance comparisons. Some policies impose waiting periods (e.g., 12–24 months) before covering pre-existing conditions, while others exclude them entirely. If you have a chronic condition like hypertension or asthma, opt for a policy with shorter waiting periods or comprehensive coverage. Additionally, some insurers offer riders (add-ons) to cover pre-existing conditions for an extra premium. Weigh the cost of the rider against the potential out-of-pocket expenses to determine if it’s a worthwhile investment.

In conclusion, comparing coverage limits requires a meticulous approach. Focus on maximum payouts, exclusions, and specific coverage for hospitalization, treatments, and pre-existing conditions. Tailor your choice to your health profile and anticipated needs, and don’t hesitate to seek clarification from insurers or brokers. A well-informed decision today can save you from financial strain tomorrow.

Overestimating Income for Health Insurance: Consequences and How to Avoid Them

You may want to see also

Explore related products

![]()

Premium Costs: Evaluate monthly/annual premiums, payment flexibility, and long-term affordability across policies

Premium costs are the backbone of any health insurance decision, but they’re not just about the sticker price. A $300 monthly premium might seem affordable now, but if it locks you into rigid payment terms or escalates unpredictably, it could become a financial burden. Start by comparing monthly versus annual premiums—annual payments often come with discounts, but they require a larger upfront commitment. For instance, a policy with a $3,600 annual premium might offer a 5% discount compared to its $300 monthly counterpart, saving you $180 yearly. However, ensure your cash flow can handle the lump sum.

Payment flexibility is another critical factor. Some insurers allow bi-annual or quarterly payments, while others penalize late payments with fees or policy cancellations. For example, a policy with a 30-day grace period for missed payments offers more breathing room than one that terminates coverage immediately. If you’re self-employed or have irregular income, prioritize policies with flexible payment schedules or autopay options to avoid disruptions. Additionally, inquire about payment methods—some insurers charge extra for credit card payments, while others waive fees for bank transfers.

Long-term affordability requires a deeper analysis than just current premiums. A policy with a $250 monthly premium might seem cheaper than one at $300, but if the latter includes a guaranteed rate lock for three years, it could save you money in the long run. Inflation and age-based rate increases can cause premiums to spike unexpectedly. For instance, a 40-year-old might see premiums rise by 5-10% annually after age 50. Look for policies with transparent rate adjustment policies or those that cap annual increases to protect your budget.

To evaluate affordability holistically, factor in your expected healthcare usage. If you’re healthy and rarely visit the doctor, a high-deductible plan with lower premiums might make sense. However, if you have chronic conditions requiring frequent care, a higher premium with lower out-of-pocket costs could be more cost-effective. Use online calculators to estimate annual expenses under different scenarios. For example, a family with two children might save $1,200 annually by choosing a plan with a $500 higher premium but lower copays and deductibles.

Finally, don’t overlook hidden costs that impact long-term affordability. Some policies bundle vision or dental coverage into premiums, while others require separate payments. A policy with a $350 monthly premium that includes dental care might be more affordable than a $300 premium plus $75 monthly dental insurance. Similarly, policies with wellness programs or telemedicine access can reduce future healthcare costs. For instance, a plan offering free annual check-ups and discounted gym memberships could save you $500 yearly in preventive care expenses. By scrutinizing these details, you can choose a policy that balances immediate costs with future financial stability.

Why Insurance Companies Often Deny Coverage for Preexisting Conditions

You may want to see also

Explore related products

![]()

Network Providers: Check in-network hospitals, clinics, and specialists included in each insurance plan

One of the most critical yet overlooked aspects of comparing health insurance policies is the network of providers each plan includes. In-network hospitals, clinics, and specialists are healthcare providers that have agreed to provide services at pre-negotiated rates, which can significantly reduce out-of-pocket costs. For instance, a visit to an in-network primary care physician might cost you a $20 copay, while the same visit to an out-of-network doctor could result in a $150 bill. To avoid such surprises, start by listing the healthcare providers you currently use or prefer, then cross-reference this list with each insurance plan’s network directory. Most insurers offer searchable online databases, making this step relatively straightforward.

Analyzing the breadth and depth of a plan’s network is equally important. A plan with a large network may seem appealing, but if it lacks specialists in your area or excludes the hospital closest to your home, its value diminishes. For example, if you have a chronic condition requiring frequent visits to a rheumatologist, ensure the plan includes multiple specialists within a reasonable distance. Similarly, families with children should verify that pediatric clinics and hospitals are part of the network. A narrow network might save you money on premiums, but it could limit your access to care when you need it most.

Another practical tip is to consider your lifestyle and mobility. If you travel frequently or split time between locations, opt for a plan with a national network or one that includes providers in multiple states. For instance, Blue Cross Blue Shield’s BlueCard program offers access to providers across the country, while HMOs often restrict coverage to a specific geographic area. Understanding these nuances can prevent unexpected denials or high costs when seeking care away from home.

Finally, don’t overlook the importance of provider quality. A large network is meaningless if it consists of low-rated hospitals or clinics. Use tools like Medicare’s Hospital Compare or U.S. News Best Hospitals rankings to assess the quality of in-network facilities. For specialists, check credentials, patient reviews, and board certifications. While insurance plans won’t always include your dream team of providers, prioritizing quality within the network ensures you receive competent care without compromising your health.

In conclusion, scrutinizing network providers is a non-negotiable step in comparing health insurance policies. By evaluating the size, location, and quality of in-network hospitals, clinics, and specialists, you can choose a plan that balances cost and accessibility. Remember, the goal isn’t just to find the cheapest option but to secure a policy that aligns with your healthcare needs and preferences.

Will Rental Insurance Cover Replacement Windows? What Landlords Need to Know

You may want to see also

Explore related products

![]()

Claim Process: Assess ease of filing claims, settlement time, and cashless facility availability

The claim process is the moment of truth for any health insurance policy. When you’re hospitalized or need medical treatment, the last thing you want is a complicated, time-consuming claims procedure. Start by scrutinizing how each insurer handles claim filing. Look for digital options like mobile apps or online portals, which streamline the process and reduce paperwork. Some insurers even offer pre-authorization for planned treatments, ensuring you’re not left scrambling at the last minute. For instance, Policy A might allow claims via a user-friendly app, while Policy B still relies on physical forms and email submissions. The ease of filing directly impacts your stress levels during an already challenging time.

Settlement time is another critical factor. A policy with a quick settlement process ensures you’re not left waiting indefinitely for reimbursement. Compare the average turnaround times advertised by insurers—some promise settlements within 7–14 days, while others may take up to a month. For example, if you’re comparing two policies with similar premiums, the one with a faster settlement time could be the better choice, especially if you’re on a tight budget. However, be wary of overly aggressive claims like "instant settlements," as these may come with hidden caveats or exclusions.

Cashless facility availability is a game-changer, particularly during emergencies. Policies with a wide network of cashless hospitals allow you to receive treatment without paying upfront, reducing financial strain. When comparing, check the number of hospitals in the insurer’s network and their locations. For instance, Policy X might have 5,000+ cashless hospitals across urban and rural areas, while Policy Y offers only 2,000, primarily in cities. If you travel frequently or live in a remote area, a policy with a broader network is invaluable.

Here’s a practical tip: Before finalizing a policy, call the insurer’s customer service and ask about their claim rejection rate. A high rejection rate could indicate stringent approval criteria or poor customer support. Additionally, read reviews from policyholders to gauge real-world experiences with the claim process. For example, if multiple users report delays in cashless approvals, it’s a red flag.

In conclusion, the claim process isn’t just about filing paperwork—it’s about how well the insurer supports you during a medical crisis. Prioritize policies with seamless digital filing, quick settlements, and extensive cashless networks. Remember, the goal is to minimize hassle and maximize support when you need it most.

IUD Insertion: Using Your Parents' Insurance

You may want to see also

Explore related products

![]()

Add-On Benefits: Compare additional features like maternity cover, critical illness, or wellness programs

Health insurance policies often come with a base level of coverage, but it’s the add-on benefits that can truly tailor a plan to your specific needs. These additional features—like maternity cover, critical illness riders, or wellness programs—can significantly impact both your financial security and overall well-being. When comparing policies, scrutinize these add-ons to ensure they align with your lifestyle, age, and health priorities. For instance, a young couple planning a family might prioritize maternity cover, while someone with a family history of cancer may value critical illness coverage.

Consider maternity cover as a prime example. Policies vary widely in terms of waiting periods (typically 9 to 48 months), coverage limits (often ₹25,000 to ₹50,000 per delivery), and inclusions (pre-natal, delivery, and post-natal expenses). Some plans even cover complications like preterm labor or cesarean deliveries. If you’re in your 20s or 30s and planning to start a family, this add-on could save you from out-of-pocket expenses that can run into lakhs. However, if you’re past childbearing age, this benefit may be unnecessary, making it a costly addition to your premium.

Critical illness riders are another add-on worth examining, especially if you have a genetic predisposition to conditions like heart disease, stroke, or cancer. These riders provide a lump-sum payout upon diagnosis, which can be used for treatment, lifestyle adjustments, or even debt repayment. Compare the list of covered illnesses (typically 10–30 conditions) and the payout amount (often 2–3 times the base sum insured). For example, a 35-year-old with a family history of heart disease might opt for a rider covering major cardiac procedures, while someone with no such history could skip this add-on to reduce premiums.

Wellness programs are a newer, increasingly popular add-on that focuses on preventive care rather than reactive treatment. These programs often include gym memberships, nutrition consultations, mental health support, or discounts on diagnostic tests. Some insurers even offer cashback or premium reductions for meeting fitness milestones, like walking 10,000 steps daily. If you’re health-conscious and proactive about wellness, these programs can provide long-term value. However, if you’re unlikely to use these perks, they may not justify the additional cost.

When comparing add-ons, ask yourself three questions: *What are my immediate and future health risks?*, *How likely am I to use this benefit?*, and *Does the cost of the add-on outweigh its potential value?* For instance, a 40-year-old with no plans for children might skip maternity cover but opt for a critical illness rider and wellness program to manage age-related health risks. Conversely, a 25-year-old athlete might prioritize wellness perks over critical illness coverage. By aligning add-ons with your unique needs, you can avoid overpaying for unnecessary features while ensuring you’re protected where it matters most.

Liberty Mutual vs. State Farm: Which Insurance Provider is Better?

You may want to see also

Frequently asked questions

When comparing health insurance policies, focus on coverage limits, premiums, deductibles, copayments, out-of-pocket maximums, network restrictions, and included benefits like prescription drugs, mental health services, or maternity care. Additionally, check for exclusions, waiting periods, and customer reviews to ensure the policy meets your specific needs.

Evaluate the policy’s network by checking if your preferred doctors, hospitals, and specialists are in-network, as out-of-network care often costs more. Also, consider the network’s size and geographic coverage, especially if you travel frequently or live in a rural area.

HMO (Health Maintenance Organization) plans typically have lower premiums and require you to choose a primary care physician and get referrals for specialists, with limited out-of-network coverage. PPO (Preferred Provider Organization) plans offer more flexibility to see any doctor without referrals and provide some out-of-network coverage, but at higher premiums. Choose based on your budget, preference for flexibility, and healthcare needs.