Life insurance is a crucial step in financial planning, offering peace of mind and security for you and your loved ones. When applying for life insurance, it's essential to carefully complete the application form, providing accurate and detailed information. The application process typically involves disclosing personal details, such as your name, date of birth, address, and Social Security number. You may also be asked about your health status, lifestyle choices, and occupation. It's imperative to be transparent and honest when filling out the form, as any inaccuracies or omissions could impact the validity of your policy.

| Characteristics | Values |

|---|---|

| Personal Information | Name, Sex, Date of Birth, Social Security/Tax ID, Driver's License, Marital Status, Birth Place, Citizenship, Address, Mailing Address, Years at Address, Email Address, Employer, Occupation |

| Policy Information | Product Name, Face Amount, Payment Period, Riders, Dividend Options, Additional Product Features |

| Owner Information | Name, Relationship to Proposed Insured, Address, Phone Number, Mailing Address, Birth/Trust Date, Social Security/Tax ID, Email Address |

| Contingent Owner Information | Name, Relationship to Proposed Insured, Address, Phone Number, Mailing Address, Birth/Trust Date, Social Security/Tax ID, Email Address |

| Payor Information | Name, Date of Birth, Address, Mailing Address, Social Security/Tax ID, Phone Number, Relationship to Proposed Insured, Amount of Life Insurance Carried, Reason for Paying Premiums |

| Beneficiary Information | Name, Date of Birth, Social Security/Tax ID, Phone Number, Address, Relationship, Percentage of Benefit |

| Additional Information | Tobacco and/or Nicotine Use, Personal Physician Information, Lifestyle Information, Financial Information, Medical History, Family History |

Explore related products

![]()

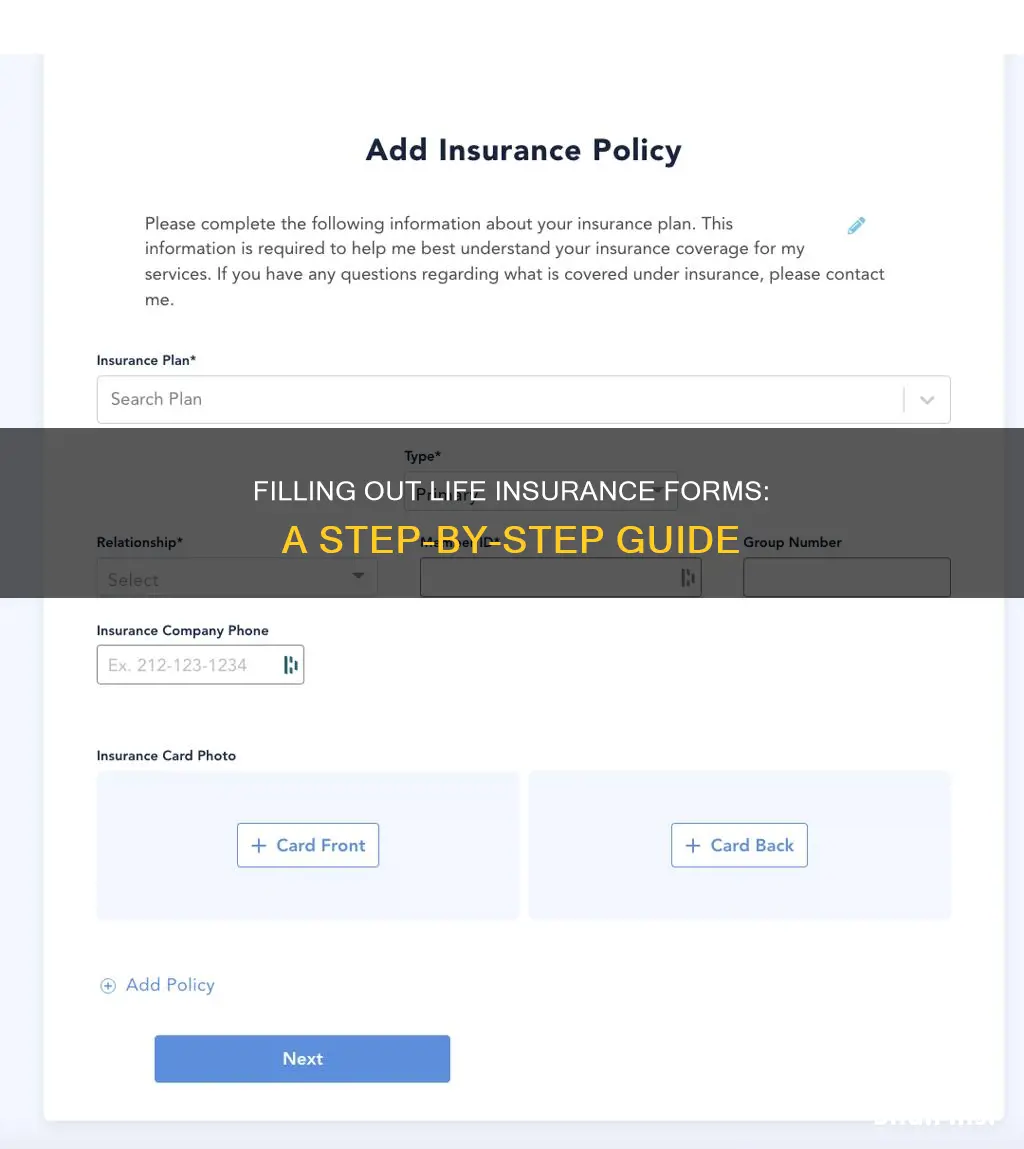

Personal information

- Full Name: The application should include the proposed insured's full name, including their first, middle, and last names.

- Sex and Date of Birth: The form should indicate the proposed insured's sex, along with their date of birth in the format mm/dd/yyyy.

- Social Security/Tax ID Number: Provide the individual's Social Security or Tax Identification Number.

- Driver's License Information: Include the state, license number, issue date, and expiration date of the proposed insured's driver's license.

- Marital Status: Specify whether the individual is single, married, widowed, or divorced.

- Birthplace: State or country of birth. If born outside the US, provide additional details such as a valid Green Card or Visa number and type.

- Citizenship: Indicate citizenship status. For non-US citizens, attach relevant documents, such as a copy of a Green Card or Visa.

- Address and Mailing Address: Provide the street address, city, state, and zip code for both residence and mailing addresses, if they differ.

- Years at Address: Mention how long the individual has resided at the current address.

- Contact Information: Include personal and business email addresses and phone numbers.

- Employment Details: Share information about the proposed insured's employer, occupation, and the duration of their current employment.

- Business Address: Provide the street address, city, state, and zip code of the workplace.

Some life insurance applications may also request additional personal information, such as details about the proposed insured's lifestyle, health history, family medical history, and any existing life insurance coverage. It's important to carefully review the specific requirements of the insurance company's application form and provide accurate and complete information.

Life Insurance: Millions of Americans Unprotected

You may want to see also

Explore related products

![]()

Policy type

The policy type is a crucial component of a life insurance form, as it dictates the nature of the insurance coverage and the benefits provided. Here is a detailed overview of the different types of life insurance policies:

Term Life Insurance

Term life insurance is designed for individuals who seek coverage for a specific number of years. It is a cost-effective option, often more affordable than permanent life insurance, as it only provides coverage for a set term, such as 10, 15, or 20 years. Term life insurance policies offer locked-in rates for the entire term, making budgeting and planning more predictable. At the end of the term, policyholders may be able to renew their coverage at adjusted rates, typically on a year-to-year basis. Additionally, some term life policies can be converted into whole life insurance policies.

Whole Life Insurance

Whole life insurance, a type of permanent life insurance, offers coverage for the insured's entire lifetime. As long as the policyholder continues to pay the premiums, the insurance remains active. Whole life insurance includes a savings component, where a portion of the premium contributes to a fixed-interest savings account. This savings component, known as the cash value, can be used by the policyholder during their lifetime for various purposes, such as taking out loans or paying policy premiums. The cash value does not affect the death benefit, and if it grows to equal the death benefit amount by a certain age, typically 100 or 120, the insurer will terminate the policy and pay out the coverage amount.

Universal Life Insurance

Universal life insurance is another form of permanent life insurance that provides coverage for the insured's entire life, as long as premiums are paid. It is sometimes referred to as adjustable life insurance due to its flexibility. Universal life policies allow policyholders to increase or decrease the death benefit and adjust or skip monthly premiums within certain limits. Similar to whole life insurance, universal life policies have a savings component that grows over time. However, unlike whole life, the interest rate for universal life policies is not fixed and can change based on market conditions. Additionally, the cash value can eventually grow to a point where it covers the cost of premiums, resulting in a zero-cost policy.

Variable Life Insurance

Variable life insurance is a riskier form of permanent life insurance. It consists of two main components: a fixed death benefit and a variable cash value. The cash value rises and falls based on the policyholder's payments and the performance of their selected investments. While variable life insurance offers a wider range of investment options and the potential for higher returns, it also exposes policyholders to higher risk, fees, and costs compared to whole life or universal life policies.

Final Expense Life Insurance

Also known as funeral or burial insurance, final expense life insurance is a type of whole life insurance with a smaller and more affordable death benefit. It is designed to cover end-of-life expenses such as funeral costs, medical bills, or outstanding debt. Final expense policies are often more accessible to older individuals or those with health issues, as they typically have fewer age and health requirements. The cash value component operates similarly to whole life insurance, accumulating value at a fixed rate over time.

Other Types of Life Insurance

In addition to the main types of life insurance, there are several other alternatives worth considering:

- Indexed Universal Life Insurance: This type of permanent life insurance has a cash value that grows based on a stock market index, such as the S&P 500 or NASDAQ. Policyholders can adjust their premiums as the cash value increases, potentially resulting in the cash value covering the cost of premiums.

- Simplified Issue Life Insurance: This type of policy does not require a medical exam, making the approval process faster and more convenient for healthy individuals. However, it generally comes with higher costs and may offer smaller coverage amounts due to the increased risk taken on by the insurer.

- Instant Life Insurance: A specific type of simplified issue policy that can be applied for online and typically provides a decision within minutes. It offers higher and more affordable coverage options compared to other simplified issue policies.

- Guaranteed Life Insurance: This policy does not involve any medical questions, and applications cannot be turned down.

- Supplemental Life Insurance: Provides additional coverage beyond what is offered by an employer's group life policy, and can be purchased from an employer or a private insurance company.

- Survivorship Life Insurance: Covers two people on a single policy and pays a death benefit once both policyholders have passed away. It is commonly used as part of estate planning to leave an inheritance for heirs.

- Decreasing Term Life Insurance: Provides coverage with a death benefit that decreases over time, making the policy more affordable than standard term life insurance.

- AD&D Insurance: This category of life insurance will only pay out if the insured person dies in an accident or suffers serious injuries such as the loss of limbs, sight, or paralysis.

Founders Federal Credit Union: Life Insurance Options?

You may want to see also

Explore related products

![]()

Beneficiaries

The beneficiary section of the life insurance form is where you name the person or people who will receive the death benefit from the policy. This is an important part of the form, as it ensures that the benefits of your policy are allocated according to your wishes.

You can name multiple beneficiaries on your policy and specify the percentage of the benefit that each person will receive. For example, you may name your spouse as the primary beneficiary and allocate them 75% of the benefit, and your child as the secondary beneficiary who will receive the remaining 25%.

If you need to make changes to your beneficiaries, you can do so by submitting a beneficiary change form. This allows you to add, change, or delete beneficiaries. Some insurance providers may have specific forms for requesting owner and beneficiary changes, so it is important to check with your provider.

In the case that no beneficiary survives the insured, the proceeds will typically revert to the estate of the insured.

Life Insurance: A Necessary Safety Net for Families

You may want to see also

Explore related products

![Property and Casualty Insurance License Exam Study Guide: Property Casualty Insurance Book and Practice Test Questions [3rd Edition]](https://m.media-amazon.com/images/I/71MhA+5nDML._AC_UY218_.jpg)

![]()

Payment options

The payment options available to you will depend on the insurance company and the type of policy you have. Here are some of the most common payment options:

- Regular Premium Payment: This is the most common and preferred mode of premium payment. With regular mode, the premium payments for your term life insurance are made on a periodic basis, at a regular frequency. The premiums for the policy could be paid yearly, monthly, quarterly, or half-yearly, based on the individual preference of the policyholder. Regular premium payments are popular as they are affordable, flexible, and avoid placing a heavy, one-time financial strain on the policyholder.

- Single Premium Payment: This is one of the less frequently chosen modes of premium payment for life insurance policies. With single premium payments, the policyholder is required to make a one-time, upfront payment of premiums, regardless of the duration of the policy. While this mode may be ideal for those who want to protect themselves against a policy lapse, it can be costly when factored for inflation.

- Limited Premium Payment: With this option, policyholders can pay the premium for their entire policy in a limited period, such as 5 or 10 years. The premium payments are taken care of within a short time, while the insurance benefits can continue for a long time. The downside is that the premium amounts are generally higher than regular payments. This option is ideal for those who wish to retire before the term of the life insurance policy ends, as it reduces the financial burden of premiums from their post-retirement lives.

- Annual Premium Payment: An annual life insurance premium payment means you cover the entire premium upfront once a year. This is typically the most cost-effective payment mode, as the insurer may offer discounts on administrative fees for a lump-sum yearly payment. However, you'll need to plan ahead to ensure you have the funds to cover the entire premium payment for the year.

- Semi-Annual Premium Payment: You'll pay a semi-annual premium payment twice a year. The premium cost for this payment mode will be higher compared to an annual payment but lower than monthly payment options. This option offers some flexibility for your budget, potentially saving you money while allowing for smaller upfront payments twice a year.

- Quarterly Premium Payment: With a quarterly premium payment plan, you'll send premium payments every three months (four times a year). This option can help balance manageability and cost, as you'll likely save on administrative and management fees, but still have affordable payments. However, you'll need to pay extra attention to the payment schedule and deadlines.

- Monthly Premium Payment: If you choose a monthly payment plan, you'll pay your premium in smaller, more manageable chunks, which can make it easier to budget. However, paying monthly may mean higher total premium payments over the policy's life. If you have a whole life policy with a cash value component, monthly payments could potentially slow the growth compared to larger lump-sum payments.

Payment Methods

In addition to the payment options outlined above, it's important to consider the payment methods accepted by your insurance company. Here are some common payment methods:

- Electronic Bank Transfer: Recurring payments using electronic bank transfer are the most common way to pay for life insurance. You can set up a recurring bank transfer so that premiums are automatically withdrawn on the same day each month or year.

- Check: Checks are allowed but may only be accepted for annual, bi-annual, or quarterly payments.

- Credit Card: Most life insurance companies only accept credit cards for the first premium payment, if at all. Companies that do accept credit cards may not accept them in every state and may add a processing fee to each payment.

- Cash: Cash is never accepted as a form of payment for life insurance.

Tricare for Life: Primary Insurance and You

You may want to see also

Explore related products

![]()

Contact details

The contact details section of the life insurance form is where you provide your personal information, such as your name, address, and date of birth. This section is crucial as it helps the insurance company identify you and contact you if needed. Here is a detailed breakdown of the information typically required in the contact details section:

- Name: Provide your full name, including your first, middle, and last name. Make sure to enter your name exactly as it appears on your legal identification documents.

- Sex: Indicate your sex, either male or female.

- Date of Birth: Enter your date of birth in the format specified (e.g., mm/dd/yyyy).

- Social Security/Tax ID: Provide your Social Security number or Tax Identification number, depending on your country of residence.

- Driver's License: Include your driver's license details, such as the state of issue, license number, issue date, and expiration date.

- Marital Status: Specify your marital status, such as single, married, divorced, or widowed.

- Birthplace: State the country or state and city of your birth.

- Citizenship: Indicate your citizenship status. If you are not a citizen of the country where you are applying for insurance, provide additional details such as your visa or Green Card information.

- Address: Provide your complete residential address, including the street, city, state, and zip code.

- Mailing Address: If your mailing address is different from your residential address, include it here. This is especially relevant if you receive mail at a P.O. box or another location.

- Years at Address: Specify how long you have resided at your current address.

- Email Address: Provide your personal email address to receive communications from the insurance company.

- Phone Number: Include your contact phone number so the insurance company can reach you if needed.

- Employer: State the name of your current employer, if applicable.

- Occupation: Describe your current occupation or profession.

- Business Address: Provide the address of your workplace, including the street, city, state, and zip code.

Remember to review the information carefully before submitting the form. If any details change over time, such as your address or phone number, be sure to update your contact details with the insurance company to ensure they have the most current information on file.

Selling Canadian Life Insurance: What You Need to Know

You may want to see also

Frequently asked questions

You will need to provide personal information, such as your name, date of birth, address, phone number, email address, and Social Security or Tax ID number. You will also need to disclose your occupation, employer, and marital status.

First, contact the life insurance company and inform them of the policyholder's passing. Then, obtain certified copies of the death certificate. After that, complete and submit the claim form, which will require information such as the policy number, the deceased's name and Social Security Number, a description of the cause of death, and your contact information as the beneficiary. Finally, choose how you would like to receive the death benefit payment.

There are several types of life insurance policies, including whole life, term life, universal life, and variable universal life. Each type offers different coverage options and benefits, so it's important to review the details of each policy before making a decision.

To change your beneficiary, you will need to contact your insurance provider and request a beneficiary change form. Complete and submit the form to update your beneficiary information. It's important to keep your beneficiary information current to ensure that your benefits are distributed according to your wishes.