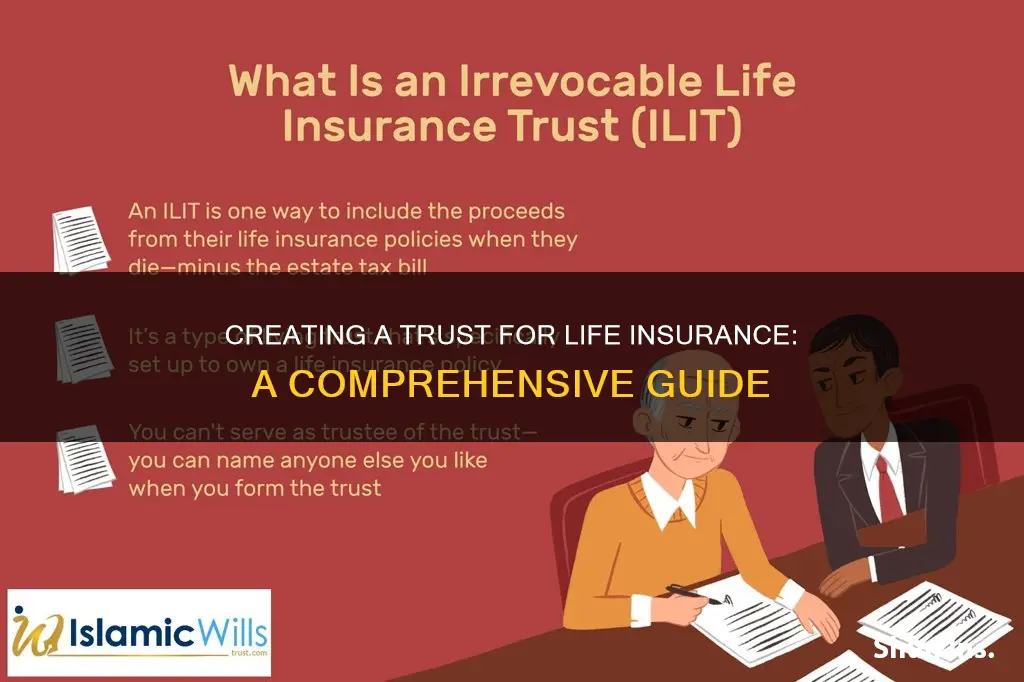

A life insurance trust is a legal arrangement that allows you to exert control over how your beneficiaries receive your life insurance payout after your death. It is particularly useful if you have young children, a child with a disability, or a large death benefit that you want to control the use of. There are two main types of life insurance trusts: irrevocable and revocable. An irrevocable life insurance trust (ILIT) is a permanent trust that cannot be altered or cancelled once it is finalised. It is beneficial for those wanting to reduce estate tax or shield assets from creditors. On the other hand, a revocable life insurance trust (RLIT) can be changed or cancelled by the grantor at any time and is ideal for growing families whose needs may change.

Explore related products

$8.99

$24.95 $24.95

What You'll Learn

![]()

Understand the types of life insurance trusts

Understanding the types of life insurance trusts is essential when creating a trust for your life insurance. Here is a detailed overview:

Irrevocable Life Insurance Trusts (ILIT)

The ILIT is an unchangeable trust that holds and manages life insurance policies. Once established, it cannot be altered or cancelled. This type of trust is ideal for those seeking to reduce estate taxes or protect assets from creditors. It offers the advantage of shielding the trust from creditors and avoiding estate taxes. However, it lacks flexibility as changes are not permitted.

Revocable Life Insurance Trusts (RLIT)

The RLIT, also known as a living trust, offers the grantor the ability to modify or cancel the trust at any time. This type of trust is suitable for individuals or families whose needs may evolve over time. While the grantor retains control, the trust becomes irrevocable upon their death or incapacitation. RLITs do not provide the same tax benefits as ILITs and may be subject to estate taxes.

When deciding between an ILIT and an RLIT, it is important to consider your financial situation, estate planning goals, and the level of control you wish to maintain over the trust.

Special Considerations

It is worth noting that a life insurance trust can be particularly beneficial if you have minor children or a child with disabilities. It allows you to specify how the life insurance funds will be distributed and used, ensuring that your wishes are respected. Additionally, a life insurance trust can help your beneficiaries maintain their eligibility for government benefits.

Life Insurance: Private Health Info's Post-Mortem Impact

You may want to see also

Explore related products

![]()

Choose the right type of life insurance

Choosing the right type of life insurance is an important decision and can be confusing. Here are some factors to consider when deciding which type of life insurance is best for you:

Term Life Insurance

Consider term life insurance if you:

- Need life insurance for a specific period. For example, if you have young children and want to ensure there will be funds to pay for their college education, you can buy a 20-year term life insurance policy.

- Need a large amount of life insurance but have a limited budget. Term life insurance generally has lower premiums than permanent life insurance. However, it only pays out if you die during the term, and you will not build equity.

- Think your financial needs may change. You can look into "convertible" term policies, which allow you to convert to permanent insurance without a medical examination, but at higher premiums.

- Are young and want to take advantage of lower premiums, which increase upon renewal as you age.

Permanent Life Insurance

Consider permanent life insurance if you:

- Need life insurance for as long as you live. A permanent policy pays a death benefit regardless of when you die.

- Want to accumulate savings that will grow tax-deferred and can be borrowed for various purposes, including paying premiums if needed.

- Are willing to pay higher premiums than for term insurance. While permanent policies have higher premiums, the premium remains the same regardless of your age, whereas term premiums can increase substantially with each renewal.

Types of Permanent Life Insurance Policies

There are several types of permanent life insurance policies to choose from, including:

- Whole life insurance: A permanent coverage type that lasts your entire life. This option may be more expensive upfront but can provide more secure benefits in the long run.

- Universal life insurance: A type of permanent policy that has an investment portion, known as the cash value, which grows in a tax-deferred account at a stable rate. Universal life insurance offers greater flexibility, as you may be able to adjust premium payments and benefit values.

- Variable life insurance: This type of permanent life insurance has cash value tied to investment accounts, so the cash value can rise and fall based on investment performance.

- Final expense insurance: A type of permanent life policy that offers a smaller death benefit payout to cover funeral, burial, and other end-of-life expenses.

- Group life insurance: This type of policy is offered by employers as a benefit to employees or members of an organization.

When choosing the right type of life insurance, it's important to consider your budget, the amount of coverage you need, and the access to cash benefits. For example, if you're starting a family and only need coverage until your children become adults, term life insurance may be the best choice. On the other hand, if you have many dependents, whole life insurance may be a better option. Additionally, if financial planning and cash value are your top priorities, universal life insurance could be a strong option.

Life Insurance and Social Security: Payout Impact

You may want to see also

Explore related products

![]()

Name the trust as the beneficiary

Naming a trust as the beneficiary of your life insurance policy is a crucial step in ensuring that the proceeds are managed and distributed according to your wishes. Here are some key considerations regarding naming the trust as the beneficiary:

Understanding the Role of a Beneficiary

The beneficiary of a life insurance policy is the person or entity designated to receive the insurance proceeds upon the insured person's death. By naming the trust as the beneficiary, you are essentially instructing the insurance company to pay the death benefit to the trust. This is a critical step in ensuring that the funds are protected and distributed according to your instructions outlined in the trust agreement.

Advantages of Naming the Trust as Beneficiary

One of the primary advantages of naming the trust as the beneficiary is that it allows you to maintain control over how the death benefit is used. You can specify the terms and conditions for distributing the funds, ensuring that your wishes are honoured. This is especially important if you have concerns about the financial maturity or capacity of your intended beneficiaries, such as minor children or individuals with special needs.

Additionally, naming the trust as the beneficiary can help streamline the distribution process and avoid probate, a lengthy legal proceeding where the court oversees the distribution of your assets. The trust enables the trustee to manage and distribute the funds according to your instructions, bypassing the need for court involvement.

Considerations for Naming the Trust as Beneficiary

When naming the trust as the beneficiary, it is essential to understand the different types of trusts and their implications. You can choose between a revocable and irrevocable trust, each offering varying levels of flexibility and control. A revocable trust provides more flexibility, allowing you to make changes or even cancel it if your circumstances change. On the other hand, an irrevocable trust is more permanent and cannot be easily altered once established.

Additionally, it is crucial to carefully select the trustee, as they will be responsible for managing and distributing the funds according to your instructions. Typically, a close friend or family member is chosen as the trustee, ensuring that they act in the best interests of the beneficiaries.

Steps to Name the Trust as Beneficiary

To name the trust as the beneficiary, you will need to work with an estate planning attorney to create the trust document. This document will outline the beneficiaries, trustees, and instructions for managing and distributing the insurance proceeds. Once the trust is established, you will need to obtain a change of ownership form from your insurance company and update the beneficiary information on your policy. It is important to ensure that the trust is both the owner and beneficiary of the policy to fully protect the proceeds from estate taxes.

Get Licensed to Sell Life Insurance in South Carolina

You may want to see also

Explore related products

![]()

Transfer ownership of the policy to the trust

Transferring ownership of a life insurance policy to a trust is the final step in setting up a trust with life insurance. Here is a detailed breakdown of the process.

The grantor (the life insurance policyholder) must sign a form from the insurance company and provide information about the trust to transfer ownership of the policy. This step is typically completed with the help of an experienced estate planning attorney, who ensures that all legal documents and paperwork are filed correctly. Once ownership is transferred, the trust becomes responsible for making premium payments, claiming the death benefit, and managing all aspects of the policy.

Important Considerations

- Tax benefits: Depending on whether you have an irrevocable or revocable trust, there can be different tax benefits. For example, with an irrevocable trust, the death benefit is usually not included in the grantor's estate and is not subject to estate tax unless the grantor dies within the first three years of the policy. On the other hand, revocable trusts do not offer the same tax advantages as irrevocable trusts and are subject to estate taxes.

- Estate planning benefits: Life insurance trusts offer asset protection, help beneficiaries avoid probate, and allow policyholders to specify how the death benefit payout should be used.

- Complexity and cost: Setting up a life insurance trust can be complex and may require the assistance of an estate planning attorney, resulting in high legal fees.

- Lack of control: Once funds are placed in an irrevocable life insurance trust, the grantor loses control over how they are used and distributed.

- Three-year lookback period: If the grantor dies within three years of setting up an irrevocable insurance trust, it may be included in their estate and subject to taxes.

When to Consider Transferring Ownership

There are several reasons why someone may want to transfer ownership of their life insurance policy to a trust, including estate tax planning and changes to financial or life circumstances, such as divorce or new financial obligations.

Term Life Insurance: Cancel Anytime, No Strings Attached

You may want to see also

Explore related products

![]()

Consult a financial professional

Consulting a financial professional is a crucial step in creating a trust for your life insurance policy. Here are some reasons why:

Expert Guidance

Financial advisors are well-versed in the complexities of estate planning and can offer personalised advice tailored to your unique circumstances. They will help you navigate the intricacies of trusts, ensuring your plan aligns with your financial goals and risk tolerance.

Trust Structure and Type

The first step in setting up a trust is determining its structure and type. A financial advisor can guide you through the pros and cons of different trust types, such as revocable vs. irrevocable trusts. They will help you understand the implications of each type, including tax consequences, flexibility, and control over assets.

Beneficiary Selection

Choosing the right beneficiary for your life insurance trust is essential. A financial advisor can assist you in selecting the most suitable beneficiary, taking into account factors such as age, financial literacy, and any special needs. They will ensure your beneficiary selection aligns with your overall estate plan and financial objectives.

Tax Implications

The tax implications of setting up a trust can be complex. A financial advisor can help you navigate the tax landscape, ensuring you structure your trust in a tax-efficient manner. They will advise on strategies to minimise estate taxes, gift taxes, and income taxes associated with your life insurance proceeds.

Trustee Selection

Selecting a trustee is a critical decision. A financial advisor can guide you in choosing an individual or institution that is well-suited to manage your trust effectively. They will help you assess factors such as the trustee's financial expertise, reliability, and ability to act in the best interests of your beneficiaries.

Ongoing Support

Financial advisors provide ongoing support and guidance. They will work closely with you to review and adjust your trust over time as your life circumstances change. This ensures that your trust remains aligned with your evolving financial goals and needs.

Life Insurance and Jeff Bezos: Does He Need It?

You may want to see also

Frequently asked questions

A life insurance trust is a legal arrangement that allows a trustee to manage assets for your beneficiaries after you pass away. It gives you control over how your beneficiaries receive your death benefit.

A life insurance trust can help you plan for your beneficiaries' future and ensure they are taken care of according to your wishes. It can also help reduce estate taxes and protect the death benefit from creditors.

To create a life insurance trust, you will need to determine the type of trust, choose the beneficiaries, calculate the insurance needed, select the type of insurance, purchase the insurance, and transfer ownership of the policy to the trust. You may also want to work with an estate attorney to ensure the process is done correctly.