Determining health insurance after marriage is a crucial step for newlyweds to ensure comprehensive coverage and financial stability. When tying the knot, couples often need to reassess their health insurance options, as marriage can significantly impact eligibility, costs, and benefits. Key considerations include evaluating whether to combine plans, stay on individual policies, or switch to an employer-sponsored family plan. Factors such as premiums, deductibles, provider networks, and prescription coverage should be carefully compared to find the most cost-effective and suitable option. Additionally, understanding open enrollment periods and special enrollment rights post-marriage is essential to avoid gaps in coverage. By thoroughly reviewing both spouses’ insurance options and consulting with HR or insurance providers, couples can make informed decisions that align with their health needs and financial goals.

| Characteristics | Values |

|---|---|

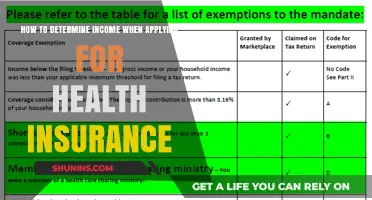

| Timing of Coverage Change | Typically, marriage qualifies as a Qualifying Life Event (QLE), allowing you to change or enroll in health insurance outside the annual Open Enrollment Period. You usually have 30-60 days after marriage to make changes. |

| Spouse’s Employer Coverage | If your spouse’s employer offers health insurance, you can join their plan during the special enrollment period triggered by marriage. Compare costs and benefits before deciding. |

| Your Employer Coverage | You can add your spouse to your employer’s health insurance plan if it allows dependent coverage. Check costs and coverage details. |

| Marketplace (ACA) Plans | If neither employer offers suitable coverage, you can explore plans on the Health Insurance Marketplace. Marriage may change your eligibility for subsidies based on combined income. |

| Medicaid Eligibility | Marriage may affect Medicaid eligibility based on combined household income and state rules. Check your state’s Medicaid guidelines. |

| Cost Considerations | Compare premiums, deductibles, copays, and out-of-pocket maximums for both individual and family plans. Family plans may be more cost-effective. |

| Network Coverage | Ensure that doctors, specialists, and hospitals you prefer are in-network for the plan you choose. |

| Prescription Drug Coverage | Review prescription drug coverage, especially if you or your spouse have ongoing medication needs. |

| Dependent Coverage Age Limits | Some plans have age limits for dependent coverage. Confirm if your spouse qualifies under these rules. |

| Coordination of Benefits | If both you and your spouse have coverage, understand how benefits coordinate to avoid over-insurance or gaps in coverage. |

| Legal Requirements | Ensure compliance with the Affordable Care Act (ACA) mandate to have health insurance or face penalties. |

| Documentation Needed | Prepare marriage certificate, proof of income, and other required documents for enrollment or changes. |

| Consultation with Experts | Consider speaking with a health insurance broker or using online tools to compare plans and costs. |

| State-Specific Rules | Some states have unique regulations regarding health insurance and marriage. Check local laws. |

| Long-Term Planning | Consider future needs, such as family planning, which may require more comprehensive coverage. |

Explore related products

What You'll Learn

- Combining Plans: Evaluate both employer-sponsored plans to decide which offers better coverage and cost

- Spousal Coverage: Check if adding your spouse to your plan is cost-effective versus their own plan

- Marketplace Options: Explore Affordable Care Act (ACA) plans for potentially better joint coverage

- Dependent Eligibility: Understand rules for adding dependents, including stepchildren or future children

- Cost Sharing: Compare deductibles, copays, and out-of-pocket maximums for joint financial planning

![]()

Combining Plans: Evaluate both employer-sponsored plans to decide which offers better coverage and cost

After marriage, one of the first practical steps couples face is navigating health insurance options, particularly when both partners have employer-sponsored plans. Combining plans isn’t just about merging coverage—it’s about maximizing benefits while minimizing costs. Start by requesting a detailed summary of benefits from each employer, including premiums, deductibles, copays, and out-of-pocket maximums. These documents will serve as your roadmap for comparison. For instance, if one plan offers lower premiums but higher deductibles, it might be ideal for a healthy couple with minimal medical needs. Conversely, a plan with higher premiums but comprehensive coverage could be better for those anticipating frequent doctor visits or chronic care.

Next, analyze the network of providers each plan covers. If one spouse has a preferred doctor or specialist, ensure they’re in-network for both plans. Out-of-network costs can skyrocket, negating any savings from lower premiums. For example, if one plan includes a top-rated hospital system while the other excludes it, this could be a deciding factor. Additionally, consider prescription drug coverage. If one spouse relies on specific medications, compare the formularies to see which plan covers them at a lower cost. Some plans may require prior authorization or step therapy, adding layers of complexity to access.

Another critical factor is coordination of benefits (COB) rules, which dictate how the two plans work together. Typically, the plan of the spouse whose birthday falls earlier in the year becomes the primary payer, with the other plan covering secondary costs. However, this doesn’t always result in full coverage. For instance, if one plan caps secondary payments at 20% of the remaining balance, out-of-pocket expenses could still be significant. Use hypothetical scenarios—like a $10,000 hospital stay—to estimate costs under both plans and determine which combination offers the best financial protection.

Finally, don’t overlook the impact of employer contributions and tax advantages. Some employers subsidize premiums more generously than others, effectively lowering the cost of one plan over another. If one spouse’s employer offers a Health Savings Account (HSA) with a high-deductible plan, this could provide long-term savings and tax benefits, especially for younger couples. However, HSAs require careful budgeting, as they pair with plans that often have deductibles exceeding $1,500 for individuals or $3,000 for families. Weigh these trade-offs against your financial stability and health needs.

In conclusion, combining employer-sponsored health plans after marriage requires a meticulous side-by-side analysis of costs, coverage, and practical considerations. By scrutinizing premiums, networks, prescription coverage, COB rules, and employer contributions, couples can make an informed decision that aligns with their health and financial goals. Remember, the “best” plan isn’t always the cheapest—it’s the one that provides the most value for your unique situation.

Medical Insurance and Viagra: What's Covered?

You may want to see also

Explore related products

![]()

Spousal Coverage: Check if adding your spouse to your plan is cost-effective versus their own plan

Marrying often means merging lives, including health insurance plans. One of the first questions newlyweds face is whether to combine coverage under one plan or maintain separate policies. Adding your spouse to your existing plan seems like the simplest solution, but it’s not always the most cost-effective. Premiums, deductibles, and out-of-pocket maximums can vary dramatically depending on the plan and provider. Before making a decision, gather both your current plan details and your spouse’s options, including employer-sponsored plans, marketplace plans, or COBRA coverage if applicable.

Consider a scenario where one spouse has a high-deductible plan with a health savings account (HSA), while the other has a low-deductible plan with higher premiums. Adding the spouse with the low-deductible plan to the high-deductible plan could result in significant premium savings but higher out-of-pocket costs if medical needs arise. Conversely, keeping separate plans might maintain lower deductibles and better coverage for both individuals. Use online calculators or consult with a benefits specialist to compare total annual costs, including premiums, deductibles, and expected medical expenses.

Another factor to weigh is the quality of coverage for each spouse’s specific health needs. For instance, if one spouse requires frequent specialist visits or prescription medications, their current plan might offer better in-network options or lower copays. Adding them to a spouse’s plan could mean losing access to preferred providers or facing higher costs for essential treatments. Review each plan’s summary of benefits and coverage (SBC) to ensure critical services are adequately covered for both individuals.

Finally, don’t overlook the flexibility of maintaining separate plans. If one spouse’s employer offers a particularly robust plan with low costs and comprehensive benefits, it might be wiser to keep that plan intact while exploring options for the other spouse. Alternatively, if both spouses are self-employed or have access to marketplace plans, compare subsidies and tax credits available for individual plans versus family plans. Sometimes, two separate plans can provide better overall value than a combined spousal plan.

In conclusion, determining the cost-effectiveness of adding your spouse to your health insurance plan requires a detailed analysis of premiums, deductibles, coverage quality, and individual health needs. Take the time to compare all available options, consider both short-term and long-term costs, and prioritize flexibility in your decision-making process. What works best for one couple may not work for another, so tailor your approach to your unique circumstances.

Insurance Policy Termination: Accidents and Their Impact

You may want to see also

Explore related products

![]()

Marketplace Options: Explore Affordable Care Act (ACA) plans for potentially better joint coverage

Marrying often triggers a special enrollment period, allowing you to change health insurance plans outside the typical open enrollment window. This is your chance to explore Affordable Care Act (ACA) plans on the Health Insurance Marketplace, which might offer better joint coverage than your current individual plans or employer-sponsored options.

The ACA's income-based subsidies can significantly reduce premiums for qualifying couples. For 2023, a couple earning up to $73,240 annually (or $98,460 in Alaska and Hawaii) may be eligible for premium tax credits. These subsidies are applied directly to your monthly premiums, making Marketplace plans more affordable than you might think.

Consider this scenario: Sarah, 28, and John, 30, are newly married. Sarah has a plan through her job, but it doesn't cover John. John's individual plan is expensive and has a high deductible. By exploring Marketplace plans, they discover a Silver-level plan with a combined premium of $350 per month after subsidies. This plan offers better coverage for both, including lower out-of-pocket costs and access to a wider network of providers.

Key factors to consider when comparing Marketplace plans include:

- Metal Tiers: Bronze, Silver, Gold, and Platinum plans offer varying levels of coverage and costs. Silver plans often provide the best balance of premiums and out-of-pocket expenses, especially when combined with cost-sharing reductions for lower-income couples.

- Provider Networks: Ensure your preferred doctors and hospitals are in-network to avoid unexpected costs.

- Prescription Drug Coverage: Carefully review formularies to ensure your medications are covered at a reasonable cost.

- Family Planning Services: If you're planning to start a family, look for plans that cover prenatal care, childbirth, and well-child visits.

Remember, the Marketplace is designed to provide accessible and affordable health insurance options. By taking advantage of the special enrollment period and exploring ACA plans, you and your spouse can find a plan that meets your needs and budget as you begin your life together.

Medical Practices: Opting Out of Billing Insurance

You may want to see also

Explore related products

![Marriage Insurance: 12 Rules to Live By [Paperback] Rev. Francis J. Hoffman, JCD [Paperback] Fr. Rocky Hoffman [Paperback] Fr. Rocky Hoffman [Paperback] Fr. Rocky Hoffman [Paperback] Fr. Rocky Hoffman [Paperback] Fr. Rocky Hoffman [Paperback] Fr. Rocky Hoffman [Paperback] Fr. Rocky Hoffman [Paperback] Fr. Rocky Hoffman](https://m.media-amazon.com/images/I/916muqX8X3L._AC_UL320_.jpg)

![]()

Dependent Eligibility: Understand rules for adding dependents, including stepchildren or future children

Marrying often means merging lives, including health insurance plans. One critical aspect to navigate is dependent eligibility, especially when it involves stepchildren or future children. Understanding the rules can save you from coverage gaps or unnecessary costs. Most employer-sponsored health plans allow you to add dependents, but the definition of "dependent" varies. Stepchildren, for instance, are typically eligible if you’re their legal guardian or if they’re financially dependent on you. Future children, including newborns and adopted children, usually qualify for immediate coverage, but you must notify your insurer within a specific timeframe, often 30 to 60 days, to avoid delays.

Adding dependents isn’t automatic—it requires action. After marriage, review your plan’s dependent eligibility criteria and submit the necessary documentation, such as a marriage certificate, birth certificate, or legal guardianship papers. Some plans may require proof of financial dependency for stepchildren, like tax returns or court documents. Be proactive: missing enrollment deadlines can leave your dependents uninsured until the next open enrollment period, unless you qualify for a special enrollment period (SEP) due to a qualifying life event, such as marriage or the birth of a child.

Comparing your spouse’s plan to yours can reveal better options for dependent coverage. For example, one plan might offer lower premiums for family coverage, while another might have a broader network of pediatricians. If both of you have access to employer-sponsored plans, use a cost calculator to estimate total expenses, including premiums, deductibles, and copays, for each option. Don’t forget to consider future needs, like prenatal care or pediatric specialists, if you’re planning to expand your family.

A common pitfall is assuming all dependents are treated equally. Some plans have age limits for dependent coverage, typically up to 26 years old, but this doesn’t apply to disabled dependents. Stepchildren may face additional scrutiny, especially if they’re covered under another parent’s plan. To avoid complications, coordinate with your spouse to determine which plan offers the best overall value for your combined family. If you’re unsure, consult your HR department or an insurance broker for personalized guidance.

Finally, keep an eye on life changes that may affect dependent eligibility. Divorce, loss of guardianship, or a child aging out of coverage are events that require prompt updates to your plan. Regularly review your policy during open enrollment to ensure it still meets your family’s needs. By staying informed and proactive, you can maximize your health insurance benefits and provide seamless coverage for all dependents, regardless of their relationship to you.

Essential Questions for Catastrophic Medical Insurance

You may want to see also

Explore related products

$16.99 $29.99

![]()

Cost Sharing: Compare deductibles, copays, and out-of-pocket maximums for joint financial planning

Married couples face a critical decision when merging health insurance plans: understanding how cost-sharing mechanisms like deductibles, copays, and out-of-pocket maximums will impact their joint finances. These elements directly affect how much you’ll pay for healthcare throughout the year, making them a cornerstone of post-marriage insurance planning. For instance, a high-deductible plan might save on monthly premiums but requires paying more out-of-pocket before coverage kicks in, while a low-deductible plan offers immediate coverage but at a higher monthly cost. Analyzing these trade-offs is essential to avoid unexpected expenses.

To begin, compare the deductibles of your individual plans versus joint plans. A deductible is the amount you pay before insurance coverage begins. For example, if one spouse’s plan has a $2,000 deductible and the other’s has a $1,500 deductible, consider whether a joint plan with a $3,000 family deductible makes sense. While family deductibles are often higher, they may still be cost-effective if both spouses anticipate significant medical expenses. However, if one spouse rarely visits the doctor, a lower individual deductible might be more practical.

Next, examine copays, which are fixed amounts paid for specific services like doctor visits or prescriptions. Copays vary widely between plans—some charge $20 per primary care visit, while others may charge $50 or more. If one spouse frequently sees specialists with higher copays, a plan with lower specialist copays could save money in the long run. Additionally, consider prescription drug copays, especially if one or both spouses take regular medications. A plan with lower drug copays might offset higher premiums.

Out-of-pocket maximums are equally crucial, as they cap the total amount you’ll spend annually on covered services. For example, if a plan has a $6,000 out-of-pocket maximum, once you’ve paid that amount, the insurance covers all additional costs. For couples, family out-of-pocket maximums typically range from $10,000 to $15,000. If one spouse has a chronic condition requiring expensive treatments, a plan with a lower out-of-pocket maximum provides better financial protection. Conversely, healthy couples might opt for a higher maximum to reduce monthly premiums.

Finally, consider your joint financial goals and risk tolerance. If you’re saving for a home or starting a family, a plan with lower out-of-pocket costs might align better with your budget. Conversely, if you have a robust emergency fund and prefer lower monthly expenses, a high-deductible plan paired with a health savings account (HSA) could offer tax advantages and long-term savings. Practical tip: Use online calculators to estimate annual healthcare costs under different plans, factoring in anticipated doctor visits, prescriptions, and potential emergencies. This approach ensures your health insurance decision supports both your health and financial well-being as a married couple.

Navigating Obamacare: A Step-by-Step Guide to Applying for Health Insurance

You may want to see also

Frequently asked questions

Getting married allows you to combine health insurance plans with your spouse, either by joining their employer-sponsored plan, keeping your own plan, or exploring new options through the marketplace or private insurers.

Yes, marriage is a qualifying life event that allows you to switch to your spouse’s health insurance plan outside of the typical open enrollment period. Contact their employer’s HR department to enroll.

Compare costs, coverage, and provider networks of both plans. Consider factors like premiums, deductibles, and whether your preferred doctors are in-network before deciding.

Notify your insurance provider or employer’s HR department of your marriage. Provide necessary documentation, such as a marriage certificate, and choose a new plan if needed.

Most employer-sponsored plans and marketplace plans allow spouses to be covered under the same policy. Review your options to find a plan that suits both of your needs.