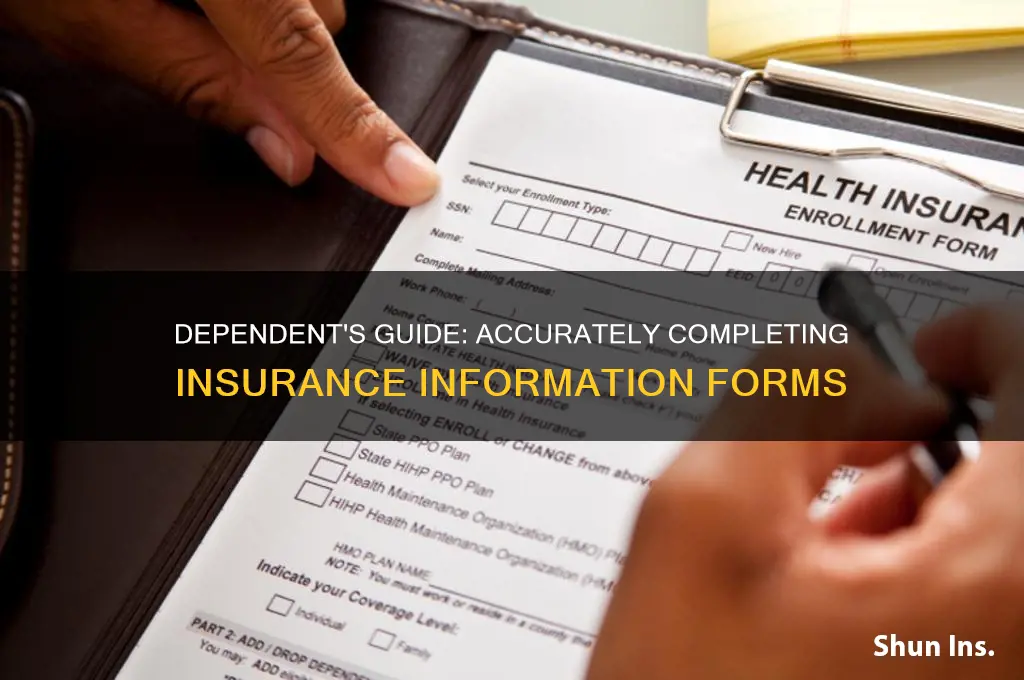

Filling out insurance information forms as a dependent can seem daunting, but with a clear understanding of the process, it becomes manageable. As a dependent, you’ll typically need to provide details about the primary policyholder, such as their name, policy number, and relationship to you, along with your own personal information, including your full name, date of birth, and contact details. It’s crucial to ensure accuracy in every field, as errors can lead to delays or complications in coverage. Additionally, familiarize yourself with the specific requirements of the insurance provider, as some forms may ask for additional documentation or details about your dependency status. Taking the time to carefully review and complete the form will help ensure seamless access to the benefits you’re entitled to.

| Characteristics | Values |

|---|---|

| Dependent Status | Clearly indicate your relationship to the policyholder (e.g., child, spouse, domestic partner). |

| Policyholder Information | Provide the policyholder's full name, date of birth, and contact details. |

| Dependent Personal Information | Include your full name, date of birth, Social Security Number (SSN), and contact information. |

| Coverage Type | Specify the type of coverage (e.g., health, dental, vision, life). |

| Effective Date | Note the date when your coverage begins. |

| **Primary Care Physician (if applicable) | List your preferred primary care physician or healthcare provider. |

| Emergency Contact | Provide an emergency contact's name, relationship, and contact details. |

| Employer Information (if applicable) | Include your employer's name and address if the insurance is work-related. |

| Previous Insurance Details | Provide details of any previous insurance coverage, if applicable. |

| Signature | Sign and date the form to confirm the accuracy of the information. |

| Supporting Documents | Attach required documents (e.g., birth certificate, marriage certificate, proof of dependency). |

| Form Submission | Submit the form to the insurance provider or employer as instructed. |

| Review and Updates | Periodically review and update your information as needed. |

Explore related products

What You'll Learn

- Gather Required Documents: Collect ID, SSN, policy details, and relationship proof for accurate form completion

- Verify Eligibility: Confirm dependency status and coverage limits with the policyholder or insurer

- Complete Personal Details: Fill in name, DOB, contact info, and address precisely as required

- Specify Relationship: Clearly state your relationship to the policyholder (e.g., child, spouse)

- Review and Submit: Double-check all entries for errors before submitting the form

![]()

Gather Required Documents: Collect ID, SSN, policy details, and relationship proof for accurate form completion

Before you dive into filling out an insurance form as a dependent, pause and gather your arsenal of documents. Think of this step as laying the foundation for a house—skimp on the materials, and the entire structure risks collapse. You’ll need four critical items: a valid ID (driver’s license, passport, or state ID), your Social Security Number (SSN), detailed policy information (policy number, group number, and insurer’s contact details), and proof of your relationship to the policyholder (birth certificate, marriage certificate, or legal guardianship papers). Without these, you’re not just risking delays—you’re inviting errors that could derail your coverage entirely.

Let’s break it down. Your ID and SSN are non-negotiable. Insurance companies use these to verify your identity and ensure you’re eligible for coverage under the policyholder. Pro tip: Double-check that your name matches exactly across all documents. Even a hyphen or middle initial discrepancy can trigger red flags. For minors, a parent’s ID won’t suffice—the dependent’s ID is required, even if it’s a school-issued card or passport.

Policy details are equally critical. Don’t assume the policyholder has this information handy. Ask for the policy number, group number (common in employer-sponsored plans), and the insurer’s name and contact details. If the policy is through an employer, you might also need the employer’s name and address. Keep these details organized—a single typo in the policy number can lead to rejection.

Relationship proof is where many dependents stumble. For children, a birth certificate is usually sufficient. Spouses need a marriage certificate, and legal dependents (like stepchildren or wards) require court documents. If you’re a domestic partner, check the insurer’s requirements—some accept affidavits or joint tax returns, while others demand specific forms. Pro tip: Scan or photograph these documents and keep them in a secure digital folder. You’ll likely need them again for future updates or claims.

Here’s the takeaway: Treat this step as your insurance form’s backbone. Spend the extra 10 minutes gathering and verifying these documents now, and you’ll save yourself hours of frustration later. Remember, accuracy isn’t just about filling out a form—it’s about ensuring you’re protected when you need it most.

Storage Unit Insurance: What's Covered in Case of Theft?

You may want to see also

Explore related products

![]()

Verify Eligibility: Confirm dependency status and coverage limits with the policyholder or insurer

Before filling out an insurance form as a dependent, it’s critical to verify your eligibility. Start by confirming your dependency status with the policyholder, typically a parent, guardian, or spouse. Insurers define dependency differently—some require full-time student status under age 26, while others mandate financial reliance. For example, a 24-year-old graduate student may qualify, but a 27-year-old working professional likely won’t. Cross-reference the insurer’s criteria with your situation to avoid submission errors.

Next, scrutinize coverage limits tied to your dependent status. Policies often cap benefits for dependents, such as lower annual maximums for dental or vision care. For instance, a family plan might cover 80% of a dependent’s orthodontic treatment up to $1,500, whereas the policyholder gets $3,000. Request a copy of the policy’s Summary of Benefits or call the insurer directly to clarify these limits. Misunderstanding these thresholds can lead to unexpected out-of-pocket costs later.

A practical tip: document all communications with the policyholder or insurer. Note dates, names, and key details discussed. For instance, if the policyholder confirms your eligibility over a call, follow up with an email summarizing the conversation. This creates a paper trail to reference if disputes arise during claims processing. Proactive documentation saves time and reduces confusion when navigating complex insurance systems.

Finally, consider edge cases that might affect eligibility. Marriage, employment changes, or aging out of dependent status can terminate coverage abruptly. For example, some insurers drop dependents immediately upon marriage, regardless of age. Others allow coverage until the end of the policy year. Review the policy’s termination clauses and plan accordingly, especially if you’re nearing a life transition that could impact your status.

By meticulously verifying dependency status and coverage limits, you ensure the form’s accuracy and avoid future complications. This step isn’t just bureaucratic—it’s a safeguard against denied claims or coverage gaps. Treat it as a non-negotiable part of the process, not an optional formality. Your diligence today prevents headaches tomorrow.

Police Dogs: Are They Covered by Insurance?

You may want to see also

Explore related products

![]()

Complete Personal Details: Fill in name, DOB, contact info, and address precisely as required

Accurate personal details are the cornerstone of any insurance form, especially when you’re listed as a dependent. Errors in your name, date of birth (DOB), contact information, or address can lead to claim denials, delays, or administrative headaches. For instance, a misspelled name or an outdated address might result in your insurer being unable to verify your identity or reach you for critical updates. Even a minor typo in your DOB could categorize you in the wrong age bracket, affecting coverage eligibility or premiums. Precision here isn’t just about neatness—it’s about ensuring the insurer has the exact data needed to process your claims efficiently.

When filling out these fields, start with your legal name as it appears on government-issued IDs (e.g., driver’s license, passport). Avoid nicknames or abbreviations unless explicitly instructed. For your DOB, use the MM/DD/YYYY format unless the form specifies otherwise. Double-check the year—a single-digit error (e.g., 1995 vs. 1996) can have significant implications. If you’re under 18, ensure your parent or guardian’s name is also listed as the policyholder, as this clarifies your dependent status. Pro tip: Keep your birth certificate or ID handy while filling out the form to avoid guesswork.

Contact information requires equal attention. Provide a phone number and email address that you check regularly, as insurers often use these to send policy updates, claim approvals, or requests for additional documentation. If you’re a student living temporarily away from home, include both your current and permanent addresses. However, designate one as the “primary” address for official correspondence. For example, if you’re at college but your parents manage the policy, use their address as primary and yours as secondary. This ensures no mail gets lost in transit.

Your address must match the one on file with the policyholder. If you’ve recently moved, confirm with them whether the insurer has been notified. Inconsistencies between your address and the policyholder’s can trigger verification delays. For international dependents, include the full address format (e.g., postal codes, province names) as used in your country. If the form has limited space, prioritize accuracy over completeness—abbreviate “Street” to “St.” or “Apartment” to “Apt” if necessary, but never omit critical details like unit numbers.

Finally, take a moment to review these details before submission. A quick cross-check with your ID and policyholder’s information can prevent weeks of back-and-forth corrections. Remember, insurers process thousands of forms daily, and clarity in your personal details streamlines their work—and yours. As a dependent, you’re relying on someone else’s policy, so ensuring your information is flawless is both a courtesy and a necessity. After all, insurance is about preparedness, and this starts with getting the basics right.

Does Lemonade Offer Renovation Insurance? A Comprehensive Coverage Guide

You may want to see also

Explore related products

![]()

Specify Relationship: Clearly state your relationship to the policyholder (e.g., child, spouse)

Accurately specifying your relationship to the policyholder is a critical step in filling out an insurance information form as a dependent. This field is not just a formality; it determines your eligibility for coverage and influences the type of benefits you receive. For instance, a "child" dependent may qualify for different health services than a "spouse," such as pediatric care or family planning resources. Insurance companies use this information to tailor policies, ensuring compliance with legal and regulatory requirements, like those outlined in the Affordable Care Act (ACA) for dependents under 26.

When completing this section, avoid vague or ambiguous terms. Instead of "family member," use precise labels like "child," "spouse," or "domestic partner." If your relationship falls into a less common category, such as "stepchild" or "fiancé(e)," confirm with the insurance provider whether these qualify under their dependent definition. Some companies may require additional documentation, like a marriage certificate or birth record, to verify the relationship. Double-check the policy’s fine print to avoid coverage gaps or claim denials later.

Consider the legal implications of your chosen relationship label. For example, listing someone as a "spouse" typically requires a valid marriage license, while "domestic partner" may necessitate proof of a long-term committed relationship, such as shared finances or residency. Misrepresenting your relationship can lead to fraud charges or policy termination. If you’re unsure, consult the insurer directly or seek guidance from a legal professional to ensure accuracy.

Practical tip: Keep a digital or physical copy of supporting documents, like birth certificates or marriage licenses, readily available when filling out the form. Some insurers allow uploading these directly during online submissions, streamlining the verification process. If completing a paper form, note the required attachments and submit them promptly to avoid processing delays. Remember, clarity in this section not only secures your coverage but also simplifies future interactions with the insurer, from claims to policy updates.

Life Insurance and Suicidal Death: What's Covered?

You may want to see also

Explore related products

![]()

Review and Submit: Double-check all entries for errors before submitting the form

Before submitting your insurance information form as a dependent, take a moment to scrutinize every detail. Even minor errors, like a misplaced digit in your policy number or an incorrect birthdate, can lead to delays or denials in coverage. Think of this step as your final defense against administrative mishaps that could complicate your healthcare access.

Start by verifying personal information: name, date of birth, and Social Security number. These fields are foundational, and discrepancies here can invalidate the entire form. Next, cross-reference the policyholder’s details against your insurance card or official documents. Ensure the policy number, group number, and effective dates match exactly—a single typo can render the form unusable. If you’re under 26 and covered under a parent’s plan, confirm the relationship field accurately reflects your status as a dependent.

For address and contact information, double-check zip codes and phone numbers. A wrong zip code might route correspondence to the incorrect location, while an outdated phone number could prevent you from receiving important updates. If you’ve recently moved or changed numbers, ensure the form reflects your current details. Additionally, review any optional fields, such as emergency contacts or preferred communication methods, to ensure they’re complete and accurate.

Finally, adopt a systematic approach to minimize oversight. Read the form aloud to catch awkward phrasing or missing words. Use a checklist to track each section as you review it, and consider having a trusted person proofread the form. If the form is digital, use tools like spell-check and date validators where available. Remember, submitting an error-free form not only ensures smooth processing but also demonstrates your attention to detail—a trait insurers value when managing claims and coverage.

Vanna White's Body Insurance: Fact or Fiction?

You may want to see also

Frequently asked questions

As a dependent, you'll typically need to provide your full name, date of birth, Social Security number (or equivalent), and relationship to the policyholder. Ensure the information matches your official records to avoid processing delays.

Qualification as a dependent varies by insurer and policy but generally includes unmarried children under 26, disabled dependents of any age, or other family members financially supported by the policyholder. Check the specific criteria in the policy guidelines.

Some insurers may require proof of dependency, such as a birth certificate, tax documents, or legal guardianship papers. Review the form instructions or contact the insurance provider to confirm if additional documentation is needed.

While the policyholder typically completes the form, some insurers allow dependents to provide their own information. Ensure the policyholder reviews and submits the form to maintain accuracy and compliance with the policy terms.

Notify the policyholder and the insurance provider immediately of any changes, such as a name change, address update, or change in dependency status. Updating the information promptly ensures continuous coverage and avoids potential issues with claims.