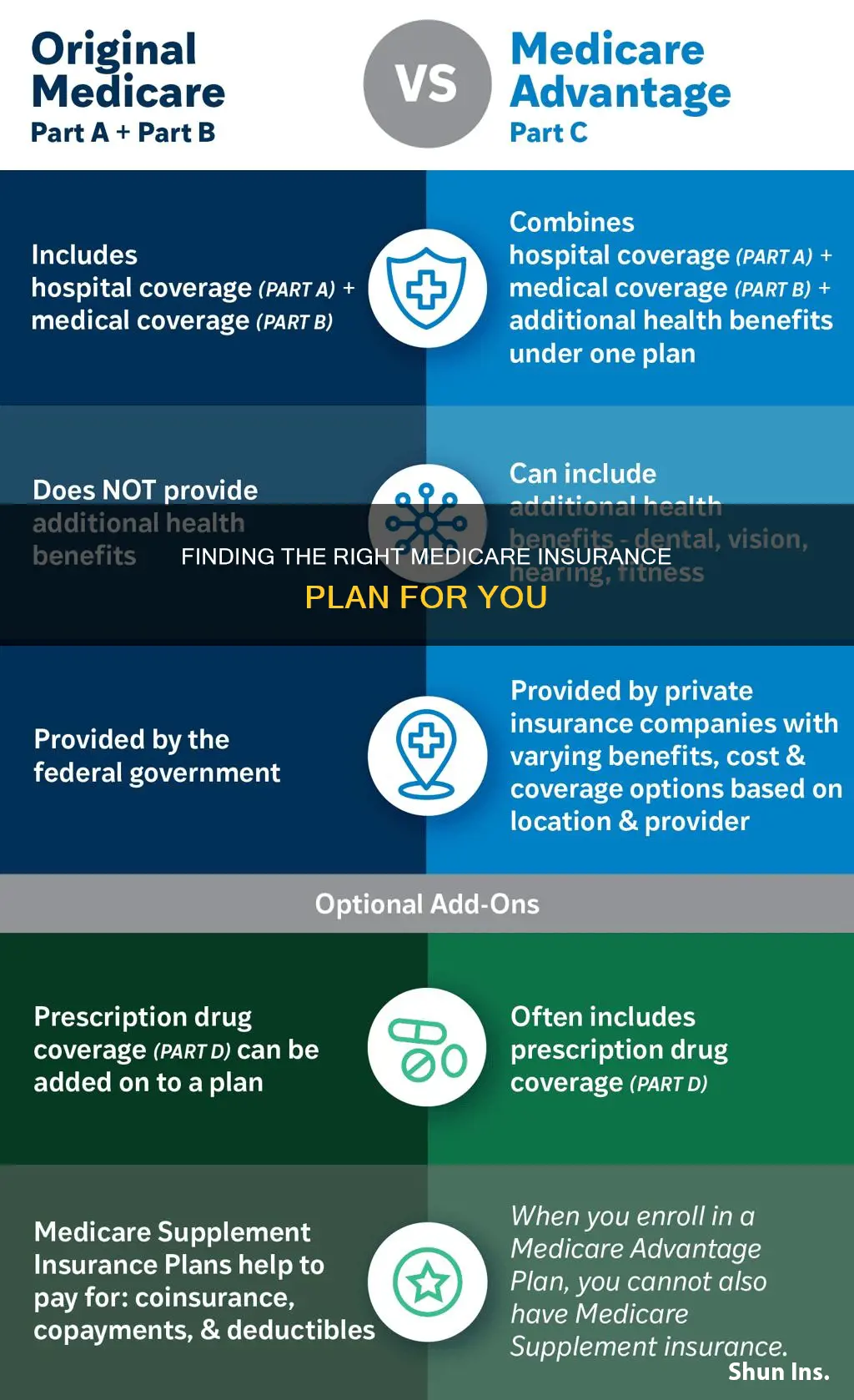

Medicare offers a variety of health insurance options, including Original Medicare (Parts A and B) and Medicare Advantage Plans (Part C). Depending on your specific needs, you may also require supplemental coverage to help pay for additional costs. This could include Medicare Supplement Insurance (Medigap), coverage from a former employer, union, or Medicaid. It's important to note that Medicare is not part of the Health Insurance Marketplace, so you don't need to make any changes if you already have Medicare coverage. However, if you are considering switching to Medicare from a Marketplace plan, there are specific situations and important considerations to keep in mind. Understanding the range of options available, as well as the benefits and limitations of each, can help individuals make informed decisions about their healthcare coverage.

| Characteristics | Values |

|---|---|

| Medicare coverage options | Original Medicare, Medicare Advantage (Part C), Medicare Supplement Insurance (Medigap) |

| Medicare Advantage Plans | Health Maintenance Organizations (HMOs), Preferred Provider Organizations (PPOs), Special Needs Plans (SNPs), Medicare Medical Savings Accounts (MSAs), Private Fee-for-Service Plans (PFFS) |

| Medicare drug plans | Medicare Part D, with a $2,000 cap on out-of-pocket costs for covered drugs |

| Medicare and other insurance | Medicare may make conditional payments if the insurance company doesn't pay within 120 days; contact the Benefits Coordination & Recovery Center for more information |

| Medicare and the Health Insurance Marketplace | Medicare isn't part of the Marketplace and isn't affected by it; in some cases, you can choose a Marketplace plan instead of Medicare |

| Medicare and dental plans | Availability of stand-alone dental plans depends on whether the Marketplace in your state is run by the federal government or the state |

| Medicare and prescription drug coverage | Prescription drug coverage in a Marketplace plan doesn't have to provide the same value as Medicare Part D, but must disclose if it's creditable coverage |

Explore related products

What You'll Learn

![]()

Medicare Advantage Plans

Most Medicare Advantage Plans include drug coverage (Part D). In most cases, you cannot join a separate Medicare drug plan if you are already enrolled in a Medicare Advantage Plan. Plans cover a variety of brand-name and generic prescription drugs. Each plan has a list of covered drugs, called a "formulary", that can vary in cost and specific drugs covered.

Debt Collectors: Insurance First?

You may want to see also

Explore related products

![Medicare and Social Security: [5 in 1] Maximize Your Retirement Benefits, Secure Medical Coverage and Quality Healthcare | Proven Strategies to Protect Your Financial Future Avoiding Costly Mistakes](https://m.media-amazon.com/images/I/71sRJGiWeQL._AC_UY218_.jpg)

$16.89 $28.99

![]()

Supplemental coverage

If you have Original Medicare, you can purchase Medicare Supplement Insurance, also known as Medigap, from a private health insurance company. Medigap policies help pay for your share of out-of-pocket costs in Original Medicare, which includes Part A (Hospital Insurance) and Part B (Medical Insurance). These policies are standardized, and in most states, they are named by letters, like Plan G or Plan K. The benefits offered by each lettered plan are the same, regardless of the insurance company, with the price being the only differentiating factor.

It is important to note that you should buy a Medigap policy within six months of getting Part A and Part B to avoid potential issues with eligibility and increased costs. You may also have other supplemental coverage options, such as coverage from a former employer or union, military benefits, or Medicaid.

Medicare Advantage Plans are another option to consider. These plans are offered by private companies and provide an alternative to Original Medicare for your health and drug coverage. Most Medicare Advantage Plans include Part D prescription drug coverage, and you cannot join a separate Medicare drug plan in addition to these plans.

If you are considering a Marketplace private health plan instead of Medicare, there are specific situations where this is possible. For example, if you are paying a premium for Part A, you can choose to drop Part A and Part B and enrol in a Marketplace plan. It is important to carefully consider your options before making any decisions, as there may be consequences if you decide to switch back to Medicare at a later date.

Ear Infection Help: No Insurance, Now What?

You may want to see also

Explore related products

![]()

Medigap policies

To purchase a Medigap policy, you typically need to have both Medicare Part A and Part B. Additionally, you will need to pay the monthly Medicare Part B premium and a separate premium to the Medigap insurance company. Medigap policies are generally guaranteed renewable, meaning they will automatically renew each year as long as you pay your premium. However, in some states, insurance companies may refuse to renew a Medigap policy purchased before 1992.

When considering a Medigap policy, it is essential to act promptly. If you do not purchase a Medigap policy within six months of enrolling in Medicare Part A and Part B, you may face difficulties in purchasing a policy or may have to pay higher prices. Additionally, certain plans, such as Plan C and Plan F, are not available to individuals who turned 65 on or after January 1, 2020, or to some people under the age of 65.

Car Insurance Rates: 24 and Still Paying High Premiums?

You may want to see also

Explore related products

![]()

Medicare Part D

Under Medicare Part D, drug benefits are provided by private insurance plans that receive premiums from both enrollees and the government. Part D plans typically pay most of the cost for prescriptions filled by their enrollees. However, the plans are reimbursed for much of this cost through rebates paid by manufacturers and pharmacies. Enrollees cover a portion of their drug expenses by paying cost-sharing. The amount of cost-sharing an enrollee pays depends on the retail cost of the filled drug, the rules of their plan, and whether they are eligible for additional Federal income-based subsidies.

To enroll in Part D, Medicare beneficiaries must also be enrolled in either Part A or Part B. Beneficiaries can participate in Part D through a stand-alone prescription drug plan or through a Medicare Advantage plan that includes prescription drug benefits. As of 2021, if you take insulin, your insulin could cost $35 or less for a 30-day supply. Stand-alone Part D plans generally don’t cover over-the-counter (OTC) medications.

Costs depend on the plan chosen, coverage, and what the enrollee will have to pay out of pocket. The cost of medications will depend on which level the medications fall under on a plan's drug list. Previously, when a person with Medicare Part D coverage reached a certain amount of out-of-pocket costs, they would enter a coverage gap known as the "donut hole". While in the "donut hole", the person was responsible for 100% of the costs of their prescription drugs until they reached the set limit and entered catastrophic coverage. As of 2025, the "donut hole" has been replaced with an out-of-pocket spending cap. When someone with Part D reaches $2,000 of out-of-pocket expenses, they automatically enter catastrophic coverage and pay nothing for their prescriptions for the rest of the year. In 2020, the average monthly Part D premium across all plans was $27.

Gap Insurance: Dealership Visits and Claims

You may want to see also

Explore related products

![]()

Medicare with other insurance

Medicare is a public health insurance program. It is not part of the Health Insurance Marketplace, so if you have Medicare coverage, you don't need to do anything else. However, you can have both Medicare and private insurance at the same time. This can occur if you have coverage through an employer or are covered under your spouse's private health insurance.

If you have both, a process called "coordination of benefits" determines which insurance provider pays first. This provider is called the "primary payer". The primary payer pays for any covered services until the coverage limit has been reached. The "secondary payer" then pays for costs that the primary payer doesn't cover. If the secondary payer doesn't cover the remaining balance, you may be responsible for the remaining costs.

There are a few situations where you can choose a Marketplace private health plan instead of Medicare. For example, if you're paying a premium for Part A (Hospital Insurance), you can drop Part A and Part B and get a Marketplace plan instead. You can also choose a Marketplace plan if you're eligible for Medicare but haven't signed up.

If you have questions about who pays first, or if your coverage changes, you can call the Benefits Coordination & Recovery Center at 1-855-798-2627.

Insurance or Hospital: Which Career Path to Choose?

You may want to see also

Frequently asked questions

You can choose between Original Medicare and Medicare Advantage (Part C). Medicare Advantage Plans are offered by Medicare-approved private companies and must follow rules set by Medicare. Most Medicare Advantage Plans include drug coverage (Part D).

Medigap is supplemental coverage that helps pay your share of costs. Medigap policies are standardized, and in most states, they are named by letters, like Plan G or Plan K. The benefits in each lettered plan are the same, no matter which insurance company sells it.

You can buy a Medigap policy from a private insurance company. Generally, you need Part A and Part B to buy a Medigap policy. You should get it within 6 months of getting Part A and Part B to avoid paying more or being denied coverage.

Medicare does not include dental coverage. If your state runs its own Marketplace, you may be able to buy a stand-alone dental plan.

Talk to your doctor or healthcare provider and ask if Medicare will cover the specific test, item, or service you need. Coverage for many tests, items, and services depends on where you live.