Finding the best health insurance for you can be a daunting task, but it's essential to ensure you have the right coverage for your needs. With so many options available, it's important to consider factors such as your budget, health needs, and lifestyle. Start by researching different types of health insurance plans, such as HMO, PPO, and EPO, and compare their benefits and drawbacks. Consider your medical history and any ongoing conditions that may require specific coverage. Additionally, think about your dependents and whether you need a family plan. By taking the time to evaluate your options and understand the details of each plan, you can make an informed decision that will provide you with the best possible health insurance coverage.

Explore related products

$4.99 $14.99

What You'll Learn

- Assess Your Health Needs: Consider your medical history, current health status, and potential future health requirements

- Understand Insurance Types: Familiarize yourself with different health insurance plans such as HMO, PPO, EPO, and POS

- Compare Coverage and Costs: Evaluate the coverage provided by each plan and compare it with the associated premiums and out-of-pocket costs

- Check Provider Networks: Ensure that your preferred healthcare providers are included in the insurance plan's network

- Read Reviews and Ratings: Research customer reviews and ratings of insurance companies to gauge their reputation and customer satisfaction

![]()

Assess Your Health Needs: Consider your medical history, current health status, and potential future health requirements

To find the best health insurance for you, it's crucial to begin by assessing your health needs. This involves a thorough evaluation of your medical history, current health status, and potential future health requirements. Start by gathering all your medical records, including any chronic conditions, past surgeries, and ongoing treatments. This information will help you understand what coverage you need and what you might be able to forego.

Next, consider your current health status. Are you generally healthy, or do you have ongoing health issues that require regular medical attention? If you have a chronic condition, such as diabetes or hypertension, you'll want to ensure that your insurance plan covers the necessary medications, doctor visits, and diagnostic tests. Additionally, think about your lifestyle and any habits that might impact your health, such as smoking or lack of exercise.

When evaluating potential future health requirements, it's essential to consider your age and family history. As you age, your health needs may change, and you may become more susceptible to certain conditions. If you have a family history of specific health issues, such as heart disease or cancer, you may want to opt for a plan that provides comprehensive coverage for those conditions.

Once you've assessed your health needs, you can begin to compare different health insurance plans. Look for plans that offer the coverage you need at a price you can afford. Consider factors such as deductibles, copays, and out-of-pocket maximums. Additionally, think about the network of providers associated with each plan and whether your preferred doctors and hospitals are included.

In conclusion, assessing your health needs is a critical step in finding the best health insurance for you. By understanding your medical history, current health status, and potential future health requirements, you can make informed decisions about the coverage you need and avoid paying for unnecessary benefits. Remember to review your insurance plan annually and make adjustments as your health needs change.

Comparing Health Insurance Costs: New York vs. Washington

You may want to see also

Explore related products

![]()

Understand Insurance Types: Familiarize yourself with different health insurance plans such as HMO, PPO, EPO, and POS

Understanding the different types of health insurance plans is crucial in making an informed decision about which one is best for you. Health insurance plans can be broadly categorized into four main types: Health Maintenance Organizations (HMOs), Preferred Provider Organizations (PPOs), Exclusive Provider Organizations (EPOs), and Point of Service (POS) plans. Each type has its own unique features, benefits, and drawbacks that you should be aware of.

HMOs are a type of health insurance plan that typically requires you to choose a primary care physician (PCP) and use only the providers within the HMO's network. This can be beneficial if you have a specific doctor or hospital that you prefer, as it may result in lower out-of-pocket costs. However, HMOs often have more restrictive coverage and may require referrals from your PCP to see a specialist.

PPOs, on the other hand, offer more flexibility in terms of choosing providers. You can see any doctor or hospital within the PPO's network without needing a referral, and you may also have the option to see providers outside of the network, although this will likely result in higher out-of-pocket costs. PPOs often have higher premiums than HMOs, but they can be a good choice if you value flexibility and choice.

EPOs are similar to PPOs in that they offer a network of providers and do not require referrals to see specialists. However, EPOs typically do not cover out-of-network care, so it's important to ensure that your preferred providers are within the network. EPOs can be a good option if you are looking for a balance between flexibility and cost.

POS plans are a hybrid of HMOs and PPOs. They require you to choose a PCP and use providers within the network, but they also offer the option to see providers outside of the network, although this will result in higher out-of-pocket costs. POS plans can be a good choice if you want the flexibility to see providers outside of the network, but you also want the cost savings of an HMO.

When choosing a health insurance plan, it's important to consider your individual needs and preferences. Do you value flexibility and choice, or are you looking for a more cost-effective option? Do you have specific providers that you prefer, or are you open to seeing new doctors? By understanding the different types of health insurance plans and their unique features, you can make a more informed decision about which one is best for you.

Understanding Medical Insurance Tiers: A Comprehensive Guide

You may want to see also

Explore related products

![]()

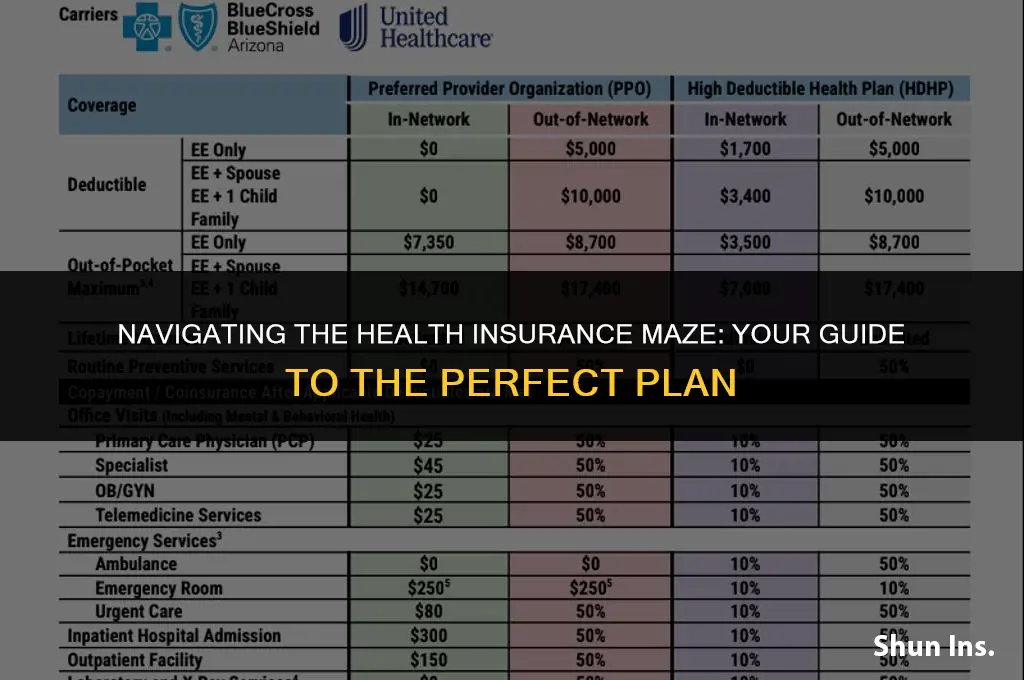

Compare Coverage and Costs: Evaluate the coverage provided by each plan and compare it with the associated premiums and out-of-pocket costs

To effectively compare health insurance plans, it's crucial to scrutinize both the coverage and costs associated with each option. Begin by evaluating the coverage provided by each plan, paying close attention to the specific services and treatments included. Look for plans that cover essential healthcare services such as doctor visits, hospital stays, prescription medications, and preventive care. Additionally, consider any extra benefits that may be important to you, such as dental and vision care, mental health services, or alternative therapies.

Once you have a clear understanding of the coverage, it's time to compare the costs. This includes not only the monthly premiums but also the out-of-pocket expenses such as deductibles, copayments, and coinsurance. Be sure to consider the overall cost of each plan, including any additional fees or charges. It's also important to think about your expected healthcare needs and how they might impact your out-of-pocket costs. For example, if you anticipate needing frequent doctor visits or prescription medications, a plan with lower copayments and coinsurance may be more cost-effective in the long run.

When comparing plans, it can be helpful to create a spreadsheet or chart to visualize the differences in coverage and costs. This will allow you to easily see how each plan stacks up against the others and make a more informed decision. Additionally, consider using online tools or resources that can help you compare plans side-by-side. Many health insurance websites offer comparison tools that allow you to input your specific needs and preferences to see which plans are the best fit for you.

It's also important to consider the provider network when comparing plans. Some plans may have a more limited network of providers, which could impact your ability to see the doctors or specialists you prefer. Be sure to check the provider network for each plan and verify that your preferred healthcare providers are included.

Finally, don't forget to read the fine print and understand any exclusions or limitations that may apply to each plan. This includes understanding what services are not covered, as well as any pre-existing condition exclusions or waiting periods. By taking the time to thoroughly compare coverage and costs, you can find the health insurance plan that best meets your needs and budget.

Does Health Insurance Cover Artificial Insemination? What You Need to Know

You may want to see also

Explore related products

![]()

Check Provider Networks: Ensure that your preferred healthcare providers are included in the insurance plan's network

When selecting a health insurance plan, it's crucial to verify that your preferred healthcare providers are part of the insurance network. This step ensures that you can access the care you need without incurring excessive out-of-pocket costs. To begin, make a list of your current healthcare providers, including primary care physicians, specialists, and any other medical professionals you see regularly. Then, visit the websites of the insurance plans you're considering and use their provider search tools to check if your preferred doctors and facilities are in-network.

If your providers are not listed, you may need to contact the insurance company directly to inquire about their network status. Additionally, consider reaching out to your providers' offices to ask if they accept the insurance plans you're evaluating. This proactive approach can help you avoid unexpected costs and ensure continuity of care.

It's also important to consider the breadth of the provider network. A larger network may offer more flexibility and convenience, especially if you travel frequently or have specific healthcare needs. Conversely, a smaller network might be more focused on quality of care or offer more personalized attention. Weigh these factors against your individual preferences and healthcare requirements.

Furthermore, don't overlook the importance of checking the network's coverage for prescription medications. If you take any regular medications, ensure that they are covered by the insurance plan's formulary. This can prevent significant out-of-pocket expenses and ensure that you have uninterrupted access to your necessary treatments.

In conclusion, thoroughly checking provider networks is a critical step in finding the best health insurance for you. By verifying the inclusion of your preferred providers and considering the network's size and scope, you can make an informed decision that aligns with your healthcare needs and financial situation.

Sacred Heart Pensacola: Medical Insurance Availability and Benefits

You may want to see also

Explore related products

![]()

Read Reviews and Ratings: Research customer reviews and ratings of insurance companies to gauge their reputation and customer satisfaction

Researching customer reviews and ratings is a crucial step in finding the best health insurance for you. This process allows you to gauge the reputation and customer satisfaction of various insurance companies, providing valuable insights into their performance and reliability. By delving into reviews, you can uncover patterns of positive or negative experiences, which can significantly influence your decision-making process.

To begin your research, you can utilize online platforms such as Yelp, Google Reviews, or specialized insurance review websites. These platforms offer a wealth of information from current and former policyholders, giving you a firsthand account of their experiences with different insurance providers. Pay close attention to the overall ratings, as well as the specific comments and feedback left by reviewers. Look for recurring themes, such as the quality of customer service, the ease of claims processing, or the comprehensiveness of coverage options.

As you analyze reviews, it's essential to consider the credibility and reliability of the sources. Some reviews may be biased or influenced by external factors, so it's crucial to take a critical approach and look for consistency across multiple platforms. Additionally, be mindful of the date of the reviews, as older feedback may not accurately reflect the current state of the insurance company.

Another valuable resource for researching insurance companies is the Better Business Bureau (BBB). The BBB provides ratings and reviews for businesses, including insurance providers, based on factors such as customer complaints, response times, and transparency. By checking the BBB ratings, you can gain a more comprehensive understanding of an insurance company's reputation and customer satisfaction levels.

In conclusion, reading reviews and ratings is an essential part of the process when searching for the best health insurance for you. By thoroughly researching customer feedback and ratings from various sources, you can make a more informed decision and choose an insurance provider that meets your needs and expectations.

Understanding Medicare Insurance Eligibility with Partial Disability

You may want to see also

Frequently asked questions

When selecting a health insurance plan, consider factors such as your budget, the level of coverage you need, the type of plan (e.g., HMO, PPO, EPO, POS), the network of providers, prescription drug coverage, and any additional benefits that may be important to you.

To compare health insurance plans, you can use online comparison tools or work with an insurance broker. Look at the premiums, deductibles, copays, coinsurance, and out-of-pocket maximums. Also, consider the plan's network, coverage for specific services, and customer reviews.

An HMO (Health Maintenance Organization) plan typically requires you to use a specific network of providers and may need a referral from your primary care physician to see a specialist. A PPO (Preferred Provider Organization) plan offers more flexibility, allowing you to see providers both in and out of the network, though you may pay more for out-of-network care.