Health insurance is a necessity for many, but it can be expensive. There are ways to save money on health insurance costs, such as shopping around for a new plan, comparing prices, and checking if you qualify for financial aid or alternative health plans. You can also check if you might save on premiums or qualify for Medicaid or other programs based on your income. This paragraph will explore the different ways to get cheaper medical insurance and provide tips on how to shop for low-cost health insurance.

| Characteristics | Values |

|---|---|

| Financial assistance | Available for those who qualify |

| Enrollment | Open enrollment is over but opportunities are available for those who experience a qualifying life change event |

| Comparison | Shop from a variety of insurance companies, compare prices, and check estimated savings |

| Health Insurance Glossary | Learn industry terms to understand health insurance plan categories, types, and costs |

| Alternative health plans | May help save money but may also limit health coverage |

| Local community health centers | Provide high-quality, low-cost health care on a sliding fee scale |

| Health First Colorado | Colorado's Medicaid program with year-round enrollment |

| Other considerations | Plan duration, renewal rights, regulation, coverage of pre-existing conditions, drug coverage, doctor visits, copays, coinsurance |

Explore related products

$8.99 $14.99

What You'll Learn

![]()

Compare prices from a variety of insurance companies

Comparing prices from a variety of insurance companies is a great way to ensure you get the best deal. It is important to do your research and understand the different types of plans and costs available.

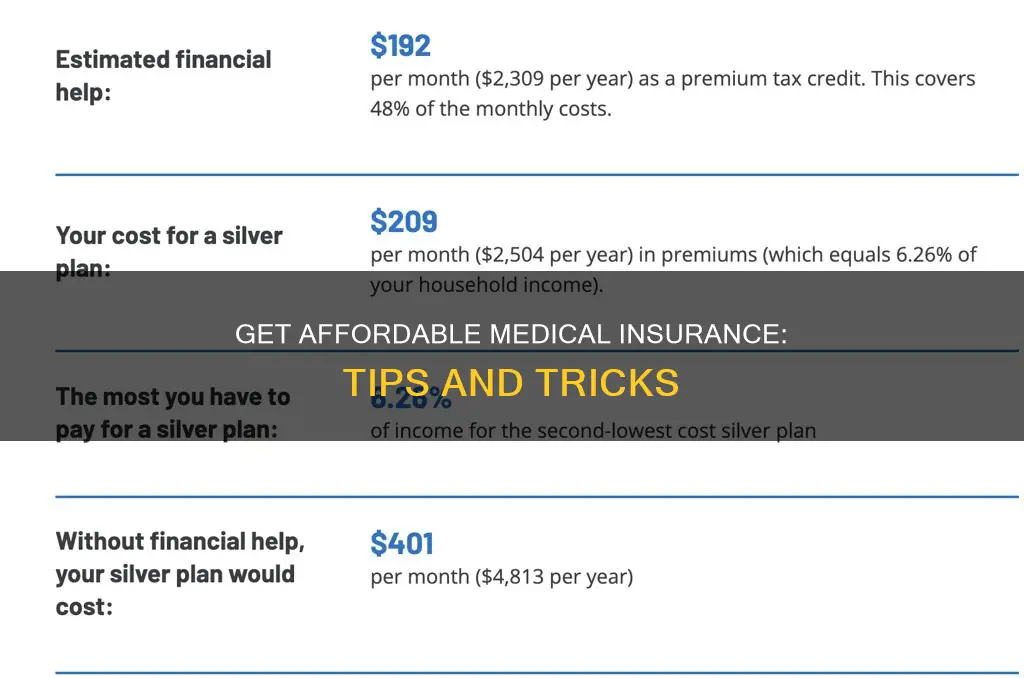

Firstly, it is worth checking if you can get financial help or special offers. Some states and companies provide financial assistance, so be sure to look into this. For example, Connect for Health Colorado is the only place to apply for financial help to lower the cost of health insurance in Colorado.

Next, you should consider your current and near-future healthcare needs. Are you planning to start a family? Do you have any pre-existing health conditions? Are you on any prescription medications? These are important factors to consider when comparing prices, as different plans will offer varying levels of coverage for different needs.

When comparing prices, be sure to review all of your health insurance options, including any plans offered through your spouse or parent. You can use online tools, such as the ACA marketplace at HealthCare.gov, to compare prices and plans from different insurance companies. This website can help you understand the different types of plans and costs available. It is also a good idea to use a cost calculator to estimate your potential savings.

Additionally, be sure to read the fine print and understand the details of each plan. Some things to consider include:

- Deductibles: How much will you have to pay out of pocket when you need care?

- Coverage: Does the plan cover pre-existing health conditions, prescription medications, brand-name drugs, doctor's visits, and hospital stays?

- Network: Are you limited to a specific network of doctors, hospitals, and urgent care centers, or can you choose your own?

- Renewability: Do you have the right to renew the plan, or can you be denied at renewal?

- Complaints: What is the complaint history of the insurance company, and who regulates them?

Travel Insurance: Medical Expense Claims and Their Validity

You may want to see also

Explore related products

$5.97 $10.99

![]()

Check if you qualify for Medicaid or CHIP

If you are looking for cheaper medical insurance, you may be eligible for Medicaid or the Children's Health Insurance Program (CHIP). These programs provide free or low-cost health coverage to millions of Americans, including low-income individuals, families, children, pregnant women, the elderly, and people with disabilities.

Medicaid eligibility depends on your income level and the requirements of your state. Each state has its own Medicaid agency that determines eligibility and provides coverage to those who qualify. To find out if you qualify for Medicaid, you can check with your state's Medicaid agency or visit Healthcare.gov to enter your household size and state to determine your potential eligibility. Even if your income is too high for Medicaid, you may still qualify for other programs, such as CHIP, which offers coverage for uninsured children and teens up to the age of 19.

When applying for Medicaid, you may need to provide certain information or documentation, such as your income details and proof of residency in the state where you are applying for benefits. Your state may also review your information annually to determine if you continue to be eligible for Medicaid coverage. It is important to note that not all medical providers accept Medicaid, so you may need to locate a Medicaid-participating provider in your area.

If you are interested in applying for Medicaid or CHIP, you can do so at any time during the year. You can create an account with the Health Insurance Marketplace and fill out an application to determine your eligibility. If you appear to qualify for either program, your information will be sent to your state agency, and they will contact you about enrollment. By exploring these options and checking your eligibility, you may be able to access more affordable medical insurance through Medicaid or CHIP.

Get Free Medical Insurance: Tips and Tricks

You may want to see also

Explore related products

![]()

Understand the different plan categories and types

When it comes to understanding the different plan categories and types, it's important to know that plan categories are about how you and your plan share costs and have nothing to do with the quality of care. The type of savings you qualify for may influence which plan category is the most suitable for you.

There are various types of health plans, and it's essential to choose one that suits your needs. One common type is a health plan that contracts with medical providers like hospitals and doctors to create a network of participating providers. Using the providers within this network will result in lower costs for you. Before choosing a plan, it's worth checking if your current doctor is part of it.

When considering a plan, it's important to ask questions and be informed. Some key questions to ask include: Does the plan cover pre-existing health conditions? Does it provide drug coverage, and if so, are brand-name drugs covered? Are there limits on how many times you can see a doctor? What are the copays for specific services, such as an emergency room visit? Will you pay coinsurance for certain services?

Additionally, it's worth noting that some plans may have hidden pitfalls. For example, be cautious of plans with prices significantly lower than their competitors, as they may have fewer benefits and more restrictions. Always ask questions and understand the terms and conditions of the plan before making a decision.

Billing Insurance Companies for Medical Records: Your Rights

You may want to see also

Explore related products

$9.45 $9.95

![]()

Shop for a new plan at a state-run marketplace

Shopping for a new health insurance plan can be confusing and overwhelming, but state-run marketplaces are there to help you navigate the process and find a plan that suits your needs and budget. These marketplaces are designed to be a one-stop shop where you can compare and enroll in a variety of low-cost, quality health insurance plans.

State-run marketplaces, such as New York State of Health, Get Covered Illinois, and Connect for Health Colorado, offer a range of tools and resources to help you make informed decisions about your health insurance. They provide a plan comparison tool that allows you to compare prices and estimated savings from different insurance companies, so you can find a plan that fits your budget. You can also review your application, renew your health insurance coverage, and seek assistance from experts, such as Certified Application Counselors and Brokers, who can help you understand your coverage options and make the best choice for your situation.

When shopping for a new plan, it is important to ask the right questions to ensure you get the coverage you need. Some key questions to consider include: Does the plan cover my pre-existing health conditions? Does it include drug coverage, and are brand-name drugs covered? Are there limits on how many times I can see a doctor? What are the copays for services like emergency room visits? Understanding the details of each plan will help you make an informed decision and avoid unexpected costs.

Additionally, be cautious of potential scams or high-pressure sales tactics. Remember that there are no limited-time offers in health insurance, and no one can promise you a special deal. Always verify the credibility of the company and check their complaint history. You can do this by contacting your state's Department of Insurance or the SHOP Call Center for assistance.

By utilizing the resources available on state-run marketplaces and being an informed shopper, you can successfully find a new health insurance plan that offers both comprehensive coverage and cost savings.

Medical Evacuation Insurance: Travel Safely, Know Your Coverage

You may want to see also

Explore related products

![Samsung Care+ Device Protection Monthly | Samsung Care+ Phone Tier 3 MRC [Subscription]](https://m.media-amazon.com/images/I/51HrsUt4s3L._AC_UY218_.jpg)

![]()

Look for warning signs when dealing with insurance salespeople

When shopping for cheaper health insurance, it is important to be cautious and vigilant. Here are some warning signs to look out for when dealing with insurance salespeople:

Lack of Listening and Understanding:

A good insurance advisor will actively listen to your needs, concerns, and financial situation. They will ask relevant questions to gather information and offer the most suitable policy for you. If your consultant is not paying attention or is more focused on delivering their sales pitch, it is a red flag. A reputable agent will take the time to understand your unique circumstances and recommend a policy that aligns with your financial goals and risk tolerance.

Inability to Provide Clear Information:

Insurance policies can be complex, but a competent agent should be able to explain the details clearly and ensure you understand what is covered and what is not. If you find yourself confused or unsure, don't hesitate to ask questions. Be cautious if the salesperson provides vague or misleading information, as this could be a sign of insurance mis-selling.

Pressure to Decide Quickly:

Be wary of high-pressure sales tactics. No one can promise you a special deal or limited-time offer in health insurance. If you feel rushed or pressured to make a decision immediately, it's a warning sign. Take your time to consider your options and seek advice from trusted sources, such as accountants or lawyers, before committing to any policy.

Unjustified Recommendations:

If an agent recommends a specific product without providing a valid reason, be cautious. Ask them to justify their recommendation and explain how it aligns with your needs. A good advisor will be able to articulate why a particular policy is suitable for you based on the information they have gathered.

Inability to Answer Basic Questions:

Before signing up for any insurance policy, make sure the agent can answer your basic questions about the plan. Inquire about coverage details, network providers, pre-existing condition coverage, drug coverage, copays, and any other concerns you may have. If they cannot provide clear and satisfactory answers, it may be a sign that they are not knowledgeable or trustworthy.

Remember, a good insurance advisor should have your best interests at heart and provide you with honest and transparent information. Don't hesitate to walk away from a salesperson if you encounter any of these warning signs.

Medical Insurance Group Numbers: Are They Confidential?

You may want to see also

Frequently asked questions

There are a few options to explore when looking for cheaper medical insurance. Firstly, you can check if you qualify for Medicaid or the Children's Health Insurance Program (CHIP) based on your income. Secondly, you can explore alternative health plans, although these may provide more limited coverage. Finally, you can contact your local community health centre for assistance, as they often provide low-cost healthcare on a sliding fee scale.

It is important to understand the details of your medical insurance plan before purchasing. Some factors to consider include the duration of the plan, whether it covers pre-existing health conditions, whether it includes drug coverage, and whether there are any limits on the number of times you can see a doctor. It is also worth comparing prices and estimated savings across different insurance companies.

Be cautious if the agent or salesperson cannot answer basic questions about the plan or if you feel pressured to make a decision immediately. Remember that there are no limited-time offers in health insurance, and be wary of unexpected calls or emails from companies you did not contact. Always check if the company is licensed and review their complaint history.