Investing in Indexed Universal Life (IUL) insurance can be a strategic way to combine life insurance protection with the potential for cash value growth tied to market indices. IUL policies offer policyholders the opportunity to allocate a portion of their premiums to an indexed account, allowing the cash value to grow based on the performance of a specific stock index, such as the S&P 500, while also providing a floor to protect against market downturns. To invest in IUL insurance, start by assessing your financial goals, risk tolerance, and need for life insurance coverage. Work with a licensed insurance professional to compare policies, understand fees, and evaluate the crediting methods and caps associated with the indexed accounts. Additionally, consider the policy’s flexibility, including options for premium payments and withdrawals, to ensure it aligns with your long-term financial strategy. Properly structured, an IUL can serve as both a safety net for your loved ones and a tax-efficient vehicle for wealth accumulation.

Explore related products

What You'll Learn

- Understanding IUL Basics: Indexed Universal Life insurance combines death benefit with cash value growth tied to indexes

- Choosing the Right Policy: Compare carriers, fees, caps, participation rates, and surrender charges for optimal returns

- Funding Strategies: Determine premium amounts and frequency to maximize cash value accumulation and policy benefits

- Riders and Add-Ons: Evaluate optional riders like accelerated death benefit or long-term care for added protection

- Tax Advantages: Explore tax-deferred growth, tax-free loans, and tax-free death benefits for efficient wealth transfer

![]()

Understanding IUL Basics: Indexed Universal Life insurance combines death benefit with cash value growth tied to indexes

Indexed Universal Life (IUL) insurance is a hybrid financial product that merges the protection of a death benefit with the potential for cash value growth linked to market indexes. Unlike traditional whole life policies, which offer fixed interest rates, IUL policies allow policyholders to participate in market gains without directly investing in stocks or bonds. This dual functionality makes IUL an attractive option for those seeking both security and growth potential. However, understanding how index-linked growth works is crucial to maximizing its benefits.

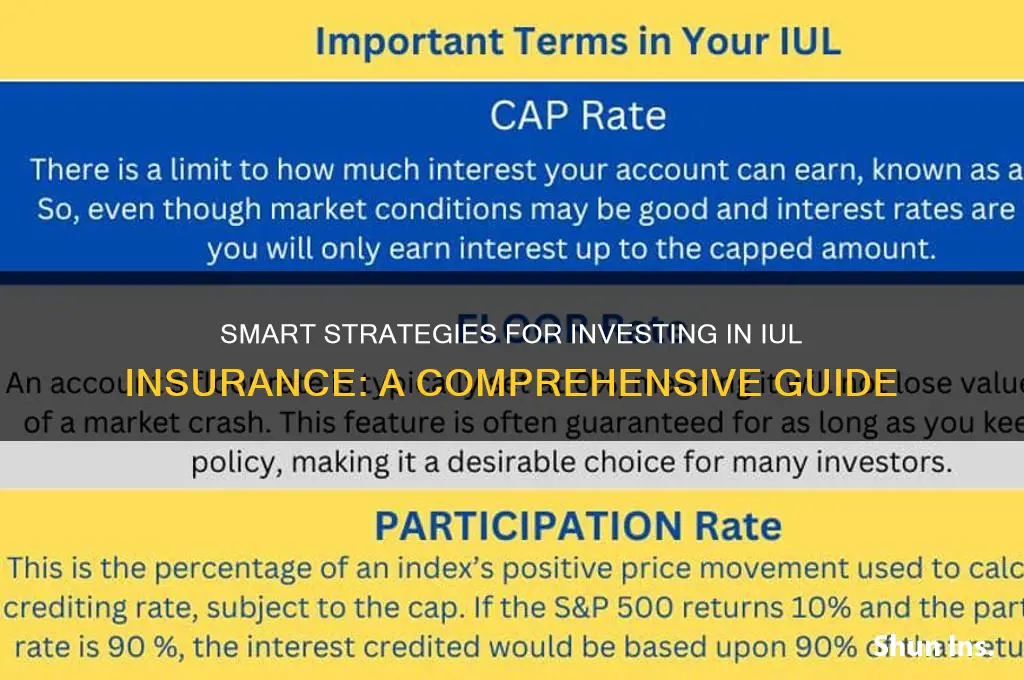

The cash value component of an IUL policy grows based on the performance of a chosen market index, such as the S&P 500. Policyholders can select from various indexing strategies, each with its own crediting method. For example, an annual point-to-point strategy measures the index’s performance from the beginning to the end of the year, while a monthly cap method applies a predetermined cap to monthly gains. Importantly, IUL policies offer a floor of 0%, meaning the cash value won’t decrease even if the index performs poorly. This feature provides a safety net absent in direct market investments.

One of the key advantages of IUL is its flexibility. Policyholders can adjust premium payments within certain limits, allowing for increased contributions during prosperous years or reduced payments when finances are tight. Additionally, the cash value can be accessed tax-free through policy loans, providing a source of liquidity for emergencies, education, or other financial needs. However, it’s essential to repay these loans to avoid reducing the death benefit or causing policy lapse.

While IUL offers growth potential, it’s not without limitations. The crediting methods often include caps, participation rates, or spreads, which can limit the upside compared to direct index investments. For instance, if the S&P 500 gains 10% but the policy has a 7% cap, the cash value will only grow by 7%. Prospective buyers should carefully review these features and consider consulting a financial advisor to ensure the policy aligns with their goals.

In practice, IUL can be a valuable tool for individuals aged 30–55 who seek long-term financial security and growth. For example, a 40-year-old with a growing family might use IUL to provide a death benefit while building cash value for future needs like retirement or college tuition. To optimize an IUL policy, policyholders should regularly review their indexing strategy, monitor fees, and ensure premiums are sufficient to keep the policy in force. By understanding these basics, individuals can leverage IUL as a strategic component of their financial plan.

Why Insurance Commissioners Conduct Examinations: Key Reasons and Insights

You may want to see also

Explore related products

![]()

Choosing the Right Policy: Compare carriers, fees, caps, participation rates, and surrender charges for optimal returns

Selecting the right Indexed Universal Life (IUL) insurance policy requires a meticulous comparison of carriers, as each offers unique features that can significantly impact your returns. For instance, Carrier A might boast a higher participation rate but impose stricter caps on index gains, while Carrier B may offer more flexibility in indexing options but charge higher fees. Start by evaluating the financial strength and reputation of the carrier, as measured by ratings from agencies like A.M. Best or Moody’s. A financially stable carrier ensures your policy’s long-term reliability, which is critical for an investment-oriented product like IUL.

Fees are the silent eroders of investment returns, and IUL policies are no exception. Administrative fees, cost of insurance charges, and rider fees can vary widely between carriers. For example, a policy with a $100 annual fee might seem negligible, but over 30 years, it compounds to $3,000—money that could have grown in your cash value account. Scrutinize the fee structure and consider how it scales with your policy’s growth. Some carriers offer fee waivers or reductions for larger premiums, making them more cost-effective for high-net-worth individuals.

Caps and participation rates are the twin engines driving your IUL’s potential returns. A cap limits the maximum return you can earn from the index’s performance, while the participation rate determines how much of the index’s gain is credited to your policy. For example, a policy with a 120% participation rate and a 6% cap could yield a 4.8% return if the index gains 8%. Compare these metrics across carriers, but beware of overly aggressive rates that may come with hidden trade-offs, such as higher fees or lower floor rates (the minimum guaranteed return).

Surrender charges are the exit fees you’ll face if you withdraw funds or cancel the policy within a specified period, often 10–15 years. These charges can be as high as 15% of the surrender value in the early years, effectively locking in your investment. If you anticipate needing liquidity in the near term, prioritize policies with shorter surrender periods or lower penalties. Alternatively, consider partial surrenders, which allow you to access a portion of your cash value without triggering the full charge, though this may reduce your death benefit.

To optimize returns, adopt a holistic approach by weighing these factors against your financial goals and risk tolerance. For instance, a 35-year-old with a long investment horizon might prioritize high participation rates and caps, while a 55-year-old nearing retirement may favor lower fees and surrender charge flexibility. Use online calculators or consult a fee-only advisor to model different scenarios and identify the policy that aligns best with your objectives. Remember, the goal isn’t just to invest in IUL insurance but to craft a policy that maximizes growth while safeguarding your financial stability.

Family Group Life Insurance: What You Need to Know

You may want to see also

Explore related products

![]()

Funding Strategies: Determine premium amounts and frequency to maximize cash value accumulation and policy benefits

Effective funding of an Indexed Universal Life (IUL) insurance policy hinges on strategic premium allocation to optimize cash value growth and policy benefits. Start by assessing your financial capacity and long-term goals. For instance, a 40-year-old professional with a stable income might aim to fund the policy with annual premiums of $10,000 to $20,000, leveraging the policy’s ability to accumulate tax-deferred cash value while providing death benefit protection. This approach balances affordability with growth potential, ensuring the policy remains sustainable over decades.

The frequency of premium payments plays a critical role in maximizing cash value accumulation. While annual or lump-sum payments often yield higher early cash value due to reduced fees and immediate investment exposure, monthly or quarterly payments can align better with cash flow needs. For example, a policyholder with irregular income might opt for flexible premium payments, ensuring they meet the minimum annual requirement to keep the policy active while contributing more during prosperous periods. This flexibility is a key advantage of IULs over traditional whole life policies.

To accelerate cash value growth, consider overfunding the policy within the insurer’s guidelines. Overfunding involves paying premiums above the minimum required to cover costs, directing excess funds into the policy’s indexed account. For instance, a policy with a $5,000 minimum annual premium might allow up to $20,000 in the first year. This strategy maximizes the amount exposed to market index gains while maintaining the policy’s tax advantages. However, be mindful of IRS guidelines to avoid classifying the policy as a Modified Endowment Contract (MEC), which imposes restrictions on tax-free withdrawals.

A comparative analysis of funding strategies reveals that consistent, higher premiums early in the policy’s life outperform staggered or lower contributions. For example, a policy funded with $15,000 annually for the first 10 years will typically accumulate more cash value than one funded with $10,000 annually for 15 years, even if the total contributions are equal. This is because early premiums benefit from compounded growth over a longer period, amplifying the impact of index-linked returns.

Finally, regularly review and adjust your funding strategy to align with life changes and policy performance. Major life events, such as a salary increase, inheritance, or reduced expenses, may warrant increasing premiums to boost cash value. Conversely, financial setbacks might necessitate reducing contributions temporarily. Most IULs allow for premium flexibility, but consult your policy’s terms and an advisor to ensure adjustments don’t compromise the policy’s integrity. By proactively managing premium amounts and frequency, you can harness the full potential of an IUL as both a protective and wealth-building tool.

Is Your Vanguard 401k Insured? Understanding FDIC and SIPC Protection

You may want to see also

Explore related products

![]()

Riders and Add-Ons: Evaluate optional riders like accelerated death benefit or long-term care for added protection

Indexed Universal Life (IUL) insurance is a versatile financial tool, but its true potential is unlocked through strategic customization. Riders and add-ons are the building blocks of this customization, allowing policyholders to tailor coverage to their unique needs. Think of them as optional upgrades that transform a basic IUL policy into a comprehensive financial safety net.

Among the most valuable riders are the accelerated death benefit and long-term care riders. These additions address specific vulnerabilities that a standard IUL policy might not cover, providing an extra layer of protection for both the policyholder and their beneficiaries.

Understanding the Accelerated Death Benefit Rider

This rider allows policyholders to access a portion of their death benefit while still alive, under specific circumstances. Typically, this is triggered by a terminal illness diagnosis with a life expectancy of 12 to 24 months. The payout can be used to cover medical expenses, home modifications, or simply to fulfill personal wishes. For example, a 55-year-old diagnosed with advanced cancer could receive up to 50% of their death benefit, providing financial relief during a challenging time. This rider is particularly valuable for those without substantial savings or comprehensive health insurance.

Long-Term Care Rider: Planning for the Future

As life expectancy increases, the likelihood of needing long-term care rises significantly. This rider provides a monthly benefit to cover expenses associated with nursing homes, assisted living facilities, or in-home care. The benefit amount is usually a percentage of the policy's face value, paid out over a defined period. For instance, a policy with a $500,000 face value might offer a 2% monthly benefit, providing $1,000 per month for long-term care needs. This rider is especially attractive for individuals concerned about outliving their savings or becoming a financial burden on their families.

Evaluating the Cost-Benefit Analysis

While riders enhance the functionality of an IUL policy, they come at an additional cost. Premiums will increase to accommodate these add-ons, so it's crucial to assess their value in relation to your personal circumstances. Consider factors such as family medical history, current health status, and existing insurance coverage. For a young, healthy individual with a robust health insurance plan, the accelerated death benefit rider might be less critical. Conversely, someone with a family history of chronic illnesses or a desire for comprehensive long-term care planning may find these riders indispensable.

Strategic Implementation: A Tailored Approach

The key to maximizing the benefits of riders is strategic implementation. Start by identifying potential gaps in your current financial plan. Are you concerned about the financial impact of a critical illness? Do you want to ensure your long-term care needs are met without depleting your assets? Once you've pinpointed these areas, consult with a financial advisor to determine the most suitable riders and coverage levels. Remember, the goal is not to add every available rider but to select those that align with your specific needs and financial goals. By doing so, you transform your IUL policy into a powerful instrument that provides peace of mind and financial security for both the present and the future.

AM Trust Insurance: Comprehensive Coverage, Reliable Protection, and Peace of Mind

You may want to see also

Explore related products

![]()

Tax Advantages: Explore tax-deferred growth, tax-free loans, and tax-free death benefits for efficient wealth transfer

Indexed Universal Life (IUL) insurance isn’t just a safety net—it’s a strategic tool for tax-efficient wealth accumulation and transfer. At its core, IUL offers tax-deferred growth, meaning the cash value inside your policy grows without annual tax liabilities. Unlike taxable investment accounts, where gains are taxed yearly, IUL allows compounding to occur uninterrupted. For instance, if your policy’s cash value grows by $10,000 in a year due to market index performance, you owe no taxes on that growth until you withdraw it. This deferral can significantly amplify long-term wealth, especially for high earners in higher tax brackets.

One of the most underutilized features of IUL is the ability to take tax-free loans against the policy’s cash value. This isn’t borrowing in the traditional sense—it’s accessing your own money without triggering taxable events. For example, if you have $50,000 in cash value, you can take a loan for $30,000 to fund a child’s education, start a business, or cover emergencies. The loan is repaid with interest, but that interest goes back into your policy, not to a bank. Properly structured, this strategy preserves the tax-free nature of the policy while providing liquidity for life’s needs.

The tax-free death benefit is where IUL truly shines as a wealth transfer vehicle. Upon your passing, beneficiaries receive the full death benefit income-tax-free. For instance, a $1 million policy payout passes directly to heirs without reducing their inheritance through taxes. This feature is particularly valuable for estate planning, as it allows for efficient transfer of wealth outside the probate process. Compare this to taxable investment accounts, where heirs may inherit a tax liability along with the assets, and the advantage becomes clear.

However, maximizing these tax advantages requires careful planning. First, ensure your policy is structured to prioritize cash value growth over excessive death benefits. Second, monitor policy performance annually to avoid lapses that could trigger taxable events. Finally, consult a financial advisor to align your IUL strategy with broader financial goals, such as retirement planning or legacy building. When used correctly, IUL’s tax advantages can transform it from a mere insurance product into a cornerstone of your financial strategy.

DCU's Term Life Insurance Offer: What You Need to Know

You may want to see also

Frequently asked questions

IUL (Indexed Universal Life) insurance is a type of permanent life insurance that combines death benefit protection with a cash value component tied to a stock market index. The cash value grows based on the performance of the chosen index (e.g., S&P 500) but offers protection against market losses, meaning you won’t lose money in down years. It’s considered an investment because the cash value can accumulate tax-deferred and be accessed during your lifetime.

To invest in IUL insurance, first consult a licensed insurance agent or financial advisor to assess your financial goals and needs. They will help you choose a policy that aligns with your objectives. You’ll then complete an application, undergo underwriting (which may include a medical exam), and pay the initial premium to activate the policy.

IUL insurance offers several advantages, including tax-deferred growth, protection against market downturns, and a death benefit for your beneficiaries. It also provides flexibility in premium payments and the ability to access cash value through loans or withdrawals. Unlike traditional investments, IUL combines growth potential with financial protection.

While IUL offers benefits, it also has downsides. Fees and charges can be high, potentially reducing overall returns. The growth of the cash value is capped, meaning you won’t earn the full market return. Additionally, accessing cash value through loans or withdrawals can reduce the death benefit and impact long-term growth. It’s important to carefully review the policy terms and consult a professional before investing.