Joining a health insurance plan can seem daunting, but it's an essential step in ensuring you have access to quality healthcare. Whether you're looking for coverage through your employer, a government program, or a private insurer, understanding the process is key. In this guide, we'll walk you through the steps to join a health insurance plan, from researching your options to completing the enrollment process. We'll cover the different types of plans available, how to compare them, and what to consider when making your decision. By the end of this guide, you'll have the confidence and knowledge to choose the right health insurance plan for your needs.

| Characteristics | Values |

|---|---|

| Process | Joining health insurance typically involves researching available plans, comparing coverage and costs, selecting a suitable plan, and enrolling through the insurance provider or a marketplace. |

| Eligibility | Eligibility criteria may include age, residency status, employment status, and income level. Some plans have specific requirements or restrictions. |

| Coverage | Health insurance plans may cover a range of services including doctor visits, hospital stays, prescription medications, and preventive care. Coverage varies by plan. |

| Cost | Costs associated with health insurance include premiums, deductibles, copayments, and coinsurance. These costs can vary widely depending on the plan and the individual's circumstances. |

| Enrollment Period | Many health insurance plans have specific enrollment periods, such as during an employer's open enrollment period or through a government-run marketplace during designated times. |

| Documentation | Required documentation may include proof of identity, residency, income, and employment status. Specific documents needed can vary by plan and provider. |

| Waiting Period | Some health insurance plans have waiting periods before coverage begins, during which time the insured may not be able to use their benefits. |

| Pre-existing Conditions | Some plans may exclude coverage for pre-existing conditions, or may have specific rules or limitations regarding such conditions. |

| Network | Health insurance plans often have networks of preferred providers. Using in-network providers can result in lower out-of-pocket costs. |

| Appeals Process | If an application for health insurance is denied, there is usually an appeals process through which the applicant can challenge the decision. |

| Customer Service | Insurance providers typically offer customer service support to assist with questions, concerns, and issues related to coverage and claims. |

| Online Resources | Many health insurance providers and marketplaces offer online resources and tools to help individuals research and compare plans, estimate costs, and enroll. |

Explore related products

What You'll Learn

- Eligibility Criteria: Understand the requirements to qualify for health insurance coverage

- Types of Plans: Explore different health insurance options available (e.g., HMO, PPO)

- Enrollment Process: Learn the steps to enroll in a health insurance plan

- Premium Costs: Discover how to calculate and pay for your health insurance premiums

- Benefits Overview: Get an overview of the benefits and coverage provided by the insurance plan

![]()

Eligibility Criteria: Understand the requirements to qualify for health insurance coverage

To qualify for health insurance coverage, it's essential to understand the eligibility criteria set by insurance providers and regulatory bodies. These criteria can vary widely depending on the type of insurance plan, the insurer, and the region. Generally, eligibility is determined by factors such as age, income, employment status, and health condition. For instance, some plans may have age limits, excluding individuals who are too young or too old. Income-based eligibility criteria are common in government-sponsored programs, where only those below a certain income threshold qualify for subsidies or free coverage.

Employment status is another critical factor, with many insurance plans requiring applicants to be employed full-time to qualify for group coverage. Individuals who are self-employed or work part-time may need to seek alternative plans. Health condition can also play a role, particularly in private insurance markets where pre-existing conditions might affect eligibility or premiums. It's important to note that under the Affordable Care Act (ACA) in the United States, insurers cannot deny coverage based on pre-existing conditions, but this protection may not apply to all types of plans or in all regions.

Navigating these eligibility criteria can be complex, and it's crucial to carefully review the requirements of each plan you're considering. Start by gathering necessary documentation, such as proof of income, employment, and health status. Then, compare the eligibility criteria of different plans to find the best fit for your situation. If you're unsure about any aspect of the eligibility process, don't hesitate to reach out to the insurer or a healthcare navigator for assistance. Understanding and meeting the eligibility criteria is the first step towards securing the health insurance coverage you need.

Striking Workers: What Happens to Your Health Insurance Coverage?

You may want to see also

Explore related products

$9.85 $19.99

![]()

Types of Plans: Explore different health insurance options available (e.g., HMO, PPO)

Health insurance plans can be broadly categorized into several types, each with its own set of benefits and limitations. Understanding these differences is crucial when selecting a plan that best fits your needs. Here, we'll explore some of the most common types of health insurance plans available.

Health Maintenance Organizations (HMOs) are one of the most popular types of health insurance plans. HMOs typically require you to choose a primary care physician (PCP) who will coordinate your care and refer you to specialists when necessary. HMOs often have lower premiums and out-of-pocket costs compared to other types of plans, but they may also have more restrictions on the providers you can see and the services you can receive.

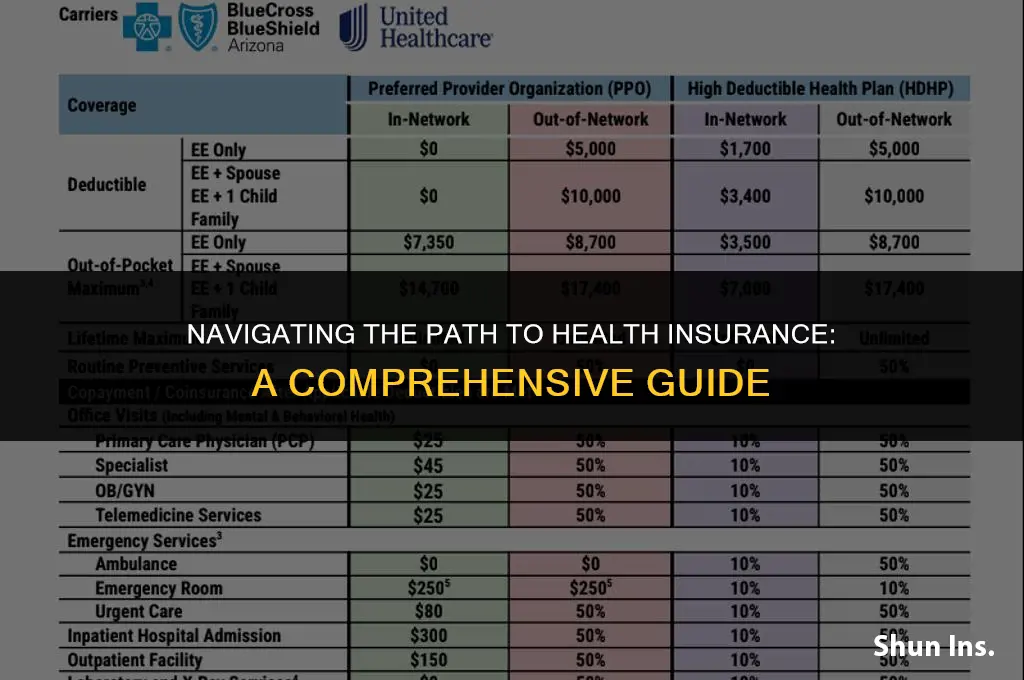

Preferred Provider Organizations (PPOs) offer more flexibility than HMOs. With a PPO, you can see any provider within the network without needing a referral from your PCP. PPOs also allow you to see out-of-network providers, although you may have to pay more for these services. Premiums and out-of-pocket costs for PPOs are generally higher than those for HMOs, but the increased flexibility can be worth the extra cost for some individuals.

Exclusive Provider Organizations (EPOs) are similar to HMOs in that they require you to use a specific network of providers. However, EPOs do not require you to choose a PCP or obtain referrals for specialist care. EPOs often have lower premiums than PPOs but may have higher out-of-pocket costs.

Point of Service (POS) plans are a hybrid of HMOs and PPOs. With a POS plan, you can choose a PCP and receive lower out-of-pocket costs for in-network care. However, you also have the option to see out-of-network providers at a higher cost. POS plans offer a balance between the lower costs of HMOs and the flexibility of PPOs.

When choosing a health insurance plan, it's important to consider your individual needs and preferences. Factors such as your budget, the providers you want to see, and the level of flexibility you need will all play a role in determining which type of plan is right for you. By understanding the different types of plans available, you can make an informed decision and select a plan that meets your healthcare needs.

Does Health Insurance Cover Chemo? Understanding Your Coverage Options

You may want to see also

Explore related products

$9.99

![]()

Enrollment Process: Learn the steps to enroll in a health insurance plan

The enrollment process for a health insurance plan can seem daunting, but it's essential to understand the steps involved to ensure you have the coverage you need. Here's a breakdown of the process:

- Research and Compare Plans: Start by researching different health insurance providers and comparing their plans. Look for plans that fit your budget and provide the coverage you need. You can use online comparison tools or consult with an insurance agent to help you make an informed decision.

- Check Eligibility: Once you've chosen a plan, check your eligibility. Most plans have specific requirements, such as age, income, and residency status. Make sure you meet these requirements before proceeding with the enrollment process.

- Gather Necessary Documents: You'll need to provide certain documents to enroll in a health insurance plan. These may include proof of identity, income, and residency. Have these documents ready to streamline the enrollment process.

- Fill Out the Application: Complete the application form provided by the insurance company. Be sure to answer all questions accurately and truthfully. If you're unsure about any information, contact the insurance company for clarification.

- Pay the Premium: Once your application is approved, you'll need to pay the premium. This can be done online, by phone, or by mail. Make sure to pay the premium on time to avoid any delays in coverage.

- Review and Confirm Coverage: After you've paid the premium, review your coverage details carefully. Make sure you understand what is covered and what is not. If you have any questions, contact the insurance company for clarification.

By following these steps, you can ensure a smooth enrollment process and have the peace of mind that comes with having health insurance coverage. Remember, it's important to act quickly, as open enrollment periods are limited. Don't wait until it's too late to get the coverage you need.

What Health Insurance Doesn’t Cover: Key Exclusions Explained

You may want to see also

Explore related products

![]()

Premium Costs: Discover how to calculate and pay for your health insurance premiums

Understanding premium costs is crucial when joining health insurance. Premiums are the monthly or annual payments you make to maintain your health coverage. Calculating these costs involves several factors, including your age, health status, location, and the type of plan you choose. Insurance companies use actuarial tables to determine the risk of insuring individuals based on these factors and set premiums accordingly.

To calculate your premium costs, start by researching different health insurance providers and comparing their plans. Each plan will have a different premium based on the coverage it offers. For example, a plan with a lower deductible and more comprehensive coverage will likely have a higher premium. Use online tools or consult with an insurance agent to get personalized quotes based on your specific information.

Once you have chosen a plan, you will need to pay your premiums regularly to maintain your coverage. Premiums can typically be paid monthly, quarterly, semi-annually, or annually. Some insurance companies offer discounts for paying premiums in full or for setting up automatic payments. Make sure to review your policy documents carefully to understand your payment options and any potential penalties for late payments.

It's also important to consider any additional costs associated with your health insurance, such as copayments, coinsurance, and out-of-pocket maximums. These costs can add up quickly, so it's essential to factor them into your overall budget when choosing a plan. By understanding and managing your premium costs, you can ensure that you have the health coverage you need without breaking the bank.

Exploring the Myths and Realities of Government-Funded Health Insurance

You may want to see also

Explore related products

![]()

Benefits Overview: Get an overview of the benefits and coverage provided by the insurance plan

Understanding the benefits and coverage provided by a health insurance plan is crucial before making a decision to enroll. This overview will delve into the specifics of what a typical health insurance plan covers, the different types of benefits available, and how to evaluate which plan is right for you.

Health insurance plans generally cover a range of medical services, including doctor visits, hospital stays, prescription medications, and preventive care. Some plans may also offer additional benefits such as dental and vision care, mental health services, and wellness programs. It's important to note that not all plans cover all services, and some may have limitations or exclusions.

When evaluating a health insurance plan, it's essential to consider the cost-sharing aspects, such as deductibles, copayments, and coinsurance. These are the amounts you'll be responsible for paying out-of-pocket before your insurance coverage kicks in. Additionally, you should be aware of the plan's network of providers, as using in-network doctors and hospitals can significantly reduce your costs.

Another key factor to consider is the plan's prescription drug coverage. If you take regular medications, you'll want to ensure that your plan covers them and that the copays are affordable. Some plans may also offer mail-order pharmacy services, which can be a convenient and cost-effective option.

Preventive care is an often-overlooked aspect of health insurance, but it's an important one. Many plans cover preventive services such as annual check-ups, vaccinations, and screenings at no cost to you. Taking advantage of these services can help you stay healthy and potentially avoid costly medical issues down the line.

In conclusion, getting an overview of the benefits and coverage provided by a health insurance plan is a critical step in the decision-making process. By understanding what's covered, what's not, and the cost-sharing aspects, you can make an informed choice that meets your healthcare needs and fits within your budget.

Understanding AARP's Medical Insurance Options and Benefits

You may want to see also

Frequently asked questions

There are several types of health insurance plans, including HMO (Health Maintenance Organization), PPO (Preferred Provider Organization), EPO (Exclusive Provider Organization), and POS (Point of Service). Each plan has its own network of providers and coverage options.

To choose the right health insurance plan, consider your healthcare needs, budget, and provider preferences. Research different plans, compare their benefits and costs, and consult with a healthcare professional or insurance agent if needed.

A deductible is the amount you pay out-of-pocket for healthcare services before your insurance coverage kicks in. A copay is a fixed amount you pay for each healthcare service, such as a doctor's visit or prescription, after your deductible has been met.

Yes, under the Affordable Care Act (ACA), health insurance companies cannot deny coverage based on pre-existing conditions. However, the cost of your premiums may be higher if you have a pre-existing condition.

To enroll in health insurance, you can visit the health insurance marketplace website, contact an insurance agent, or enroll through your employer if they offer health insurance benefits. Be prepared to provide personal information and answer questions about your healthcare needs and budget.