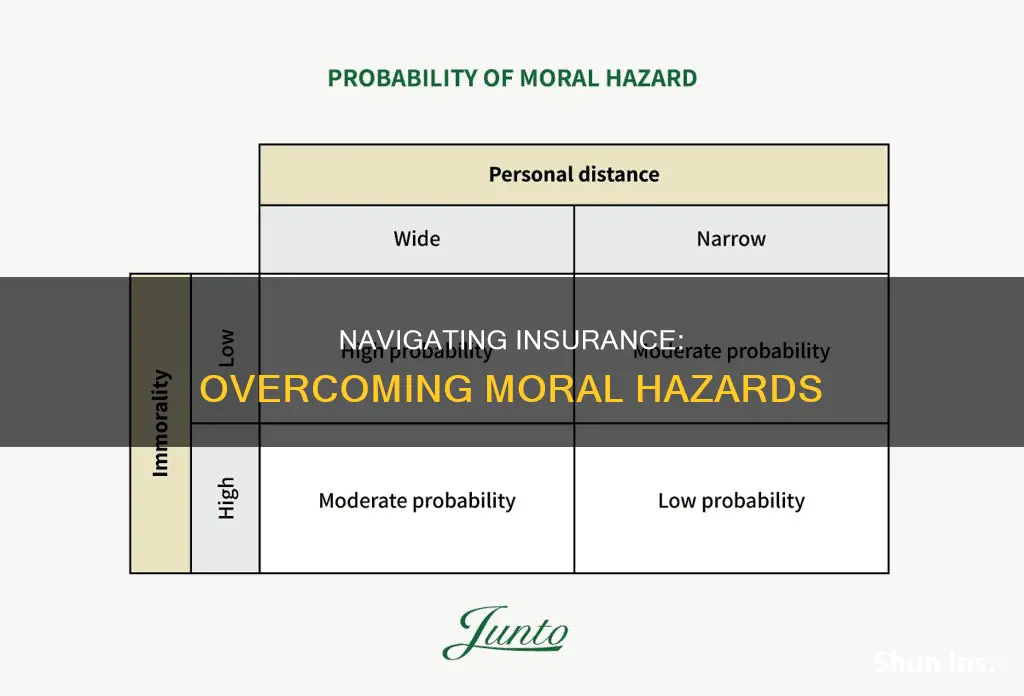

The concept of moral hazard is essential in the insurance industry. Moral hazard refers to a situation where an individual takes on unnecessary risks that affect the other party in a transaction because they know they will not bear the full cost of the risk. In the insurance sector, this means that insured individuals may be more inclined to take greater risks, knowing that the insurance company will cover any losses. This can lead to increased costs for insurance companies and, consequently, higher insurance premiums for all customers. Moral hazard can also occur in lending, finance, and employer-employee relationships. While it is challenging to eliminate moral hazard entirely, measures such as co-pays, deductibles, and regular monitoring can help mitigate its impact.

| Characteristics | Values |

|---|---|

| Definition | Moral hazard is the risk that a party has not entered into a contract in good faith or has provided misleading information about its assets, liabilities, or credit capacity. |

| Application | Common in the lending, finance, and insurance industries, but also can exist in employee-employer relationships. |

| Incentive | The incentive to take on additional risks that negatively affect the other party. |

| Information | Asymmetric information, where the risk-taking party knows more about its intentions than the party paying the consequences of the risk. |

| Example | A property owner may be less inclined to protect their property since insurance lessens the burden in case of a disaster. |

| Solution | Health insurance providers institute co-pay and deductibles, requiring individuals to pay partially for the services they receive. |

| Prevention | Incentives, policies to prevent immoral behavior, and regular monitoring. |

Explore related products

What You'll Learn

![]()

The root cause of moral hazard is asymmetric information

The concept of a moral hazard is essential in the insurance industry. It refers to a situation where an individual or entity takes on greater risks because they know they are insured and that any resulting costs will be covered by the insurer. This phenomenon is often driven by asymmetric information, where one party possesses more information than the other, leading to a power imbalance and potential exploitation.

The root cause of moral hazard is indeed asymmetric information. This occurs when there is an imbalance in information between two parties, such as the insured and the insurer. In such cases, the party with more information may alter their behaviour to benefit themselves at the expense of the less informed party. For example, a homeowner with flood insurance may be less vigilant about flood preparation, knowing that any damage will be covered by their insurance company. This behaviour increases the risk for the insurer, who now has a higher chance of having to pay out a claim.

In the health insurance industry, moral hazard occurs when individuals seek more expensive and riskier medical services than they would if they had to pay for them out of pocket. This behaviour increases the cost for the insurer. To mitigate this, health insurance providers may implement co-pays and deductibles, requiring individuals to partially pay for the services they receive. This discourages excessive use of medical services and reduces the occurrence of moral hazard.

Moral hazard can also occur in principal-agent relationships, where one party (the agent) acts on behalf of another party (the principal). If the agent has more information about their intentions or actions than the principal, they may be incentivised to act in a riskier manner, particularly if their interests are not aligned. This type of information asymmetry can lead to a conflict of interest and negative consequences for the principal.

Furthermore, adverse selection, a concept closely related to moral hazard, also arises from asymmetric information. Adverse selection occurs when one party has superior information about product quality or intentions and exploits this advantage to their benefit. This results in an inefficient allocation of resources and can lead to increased prices and reduced quality of goods and services.

To summarise, the root cause of moral hazard is asymmetric information, where one party possesses more information than the other, leading to behaviour changes that increase risk and costs for the less informed party. This phenomenon is prevalent in insurance and principal-agent relationships and can result in adverse selection and inefficient markets.

Savings Insurance: Are Apple Accounts Covered?

You may want to see also

Explore related products

![]()

Moral hazard in health insurance

Moral hazard is a situation in which one party in a transaction has the opportunity to take on additional risks that negatively impact the other party. This can occur when there is asymmetric information between the two parties, such as when one party has more accurate or hidden information than the other. In the context of health insurance, moral hazard refers to the responsiveness of healthcare spending to insurance coverage.

The concept of moral hazard in health insurance suggests that individuals with health insurance may be more likely to seek medical care, regardless of whether they truly need it. This is because insurance coverage lowers the marginal cost of care, making healthcare more affordable and accessible. As a result, individuals may increase their utilisation of healthcare services, leading to a potential overconsumption of healthcare resources. This can drive up costs for insurers and impact the overall healthcare system.

To address moral hazard in health insurance, various strategies can be implemented. One approach is to introduce co-pay and deductible systems, where individuals are required to partially pay for the healthcare services they receive. This can help reduce overconsumption and encourage individuals to consider the costs and necessity of their healthcare decisions. Additionally, insurance companies can emphasise the importance of healthy behaviours and provide incentives for policyholders to maintain their health, such as through discounted premiums for non-smokers or those who engage in regular exercise.

Another strategy to mitigate moral hazard is through integrated universal healthcare systems, as seen in countries like the Netherlands and Germany. By combining insurance and service protocols, these systems can help control healthcare utilisation and costs while ensuring that individuals have access to the necessary healthcare services. Additionally, it is important for insurance companies to have accurate and transparent information about their policyholders' health conditions and risks to make informed decisions and mitigate the impact of information asymmetry.

While moral hazard in health insurance is a complex issue, it is important to recognise that the availability of health insurance can also have positive impacts. It can provide individuals with financial protection, improve access to healthcare, and potentially lead to better health outcomes. Therefore, the key lies in finding a balance between providing adequate insurance coverage and preventing the overconsumption of healthcare services.

Cigna Commercial Insurance: PPO or HMO?

You may want to see also

Explore related products

![]()

Moral hazard and bailouts

Moral hazard is a situation in which a party has an incentive to increase its exposure to risk because it does not bear the full costs associated with that risk. In the context of insurance, this means that an individual or entity may be more inclined to take on additional risks or act recklessly because they know that any potential losses will be covered by their insurance policy.

Bailouts of financial institutions, such as those that occurred during the 2008 financial crisis, can create a moral hazard. If a firm knows that it will be bailed out by the government or another entity in the event of failure, it may be incentivized to take on excessive risks in pursuit of higher profits, without considering the potential negative consequences for the economy or taxpayers. This expectation of a bailout can lead to a situation where firms take on more risk than they otherwise would, knowing that they are protected from the full impact of their decisions.

For example, during the 2008 financial crisis, banks made risky loans to unqualified borrowers because they expected to be bailed out if things went wrong. Similarly, individuals who have insurance on their property may be less inclined to take precautions to protect it, knowing that any damage will be covered by their insurance company. This can lead to increased insurance claims and drive up the cost of insurance for everyone.

To mitigate the moral hazard associated with bailouts, some have suggested alternative regulations such as controlling short-term interest rates offered by banks or requiring managers to account for systemic externalities in their governance decisions. Additionally, creating a privatized fund to minimize the public cost of bailing out systemically important firms could help reduce the moral hazard associated with government bailouts.

In the health insurance industry, moral hazard can be mitigated by implementing co-pay and deductible policies, which require individuals to pay partially for the services they receive. This encourages individuals to consider the financial implications of their actions and can lead to reduced claims and lower costs for insurers.

Understanding Your Rights: Communicating with Insurance Adjusters After Water Damage

You may want to see also

Explore related products

![]()

Moral hazard in employee-employer relationships

Moral hazard is a situation where an individual has an incentive to take actions that lead to a negative outcome for another party. This occurs when one party in a transaction has the opportunity to assume additional risks that negatively affect the other party. The decision is based on what provides the highest level of benefit, hence the reference to morality.

Moral hazard is common in the lending, finance, and insurance industries, but it can also exist in employee-employer relationships. For example, an employee with a company car that they do not have to pay to repair may be less careful and more likely to take risks with the vehicle. Similarly, an employee enrolled in their company's dental insurance plan may be less concerned about their oral hygiene.

Firms can address moral hazard in employment relationships through performance pay and managerial control. For instance, an auto-repair firm implemented detailed checklists for mechanics and monitored their use, resulting in a 20% increase in revenue. This managerial control approach proved more effective than simply increasing mechanic commission rates.

To mitigate moral hazard, practices or incentives can be implemented to ensure the risk-taking party has some "skin in the game". For example, health insurance providers introduce co-pay and deductibles, requiring individuals to partially pay for the services they use, which encourages them to avoid making claims.

In the context of employee-employer relationships, offering incentives or performance-based pay can help align the interests of employees with those of the employer, reducing the potential for moral hazard.

Fidelis: Commercial Insurance and Its Benefits

You may want to see also

Explore related products

![The Drug Users Bible [Extended Edition]: Harm Reduction, Risk Mitigation, Personal Safety](https://m.media-amazon.com/images/I/71QnZ+8wqmL._AC_UY218_.jpg)

![]()

Moral hazard and adverse selection

Moral Hazard

Moral hazard occurs when there is asymmetric information between two parties, and the behaviour of one party changes after an agreement is made. This happens when one party has an incentive to take on additional risks that negatively affect the other party. The decision to take on these risks is based on what will bring the highest benefit, rather than what is considered morally right. For example, in the insurance industry, a property owner with insurance may be less inclined to protect their property, knowing that the insurance company will bear the cost of any damage. Similarly, in the health industry, individuals with health insurance may be more inclined to seek out riskier and more expensive medical treatments.

Adverse Selection

Adverse selection, on the other hand, occurs when one party in a deal has more accurate or private information about a product's quality than the other and exploits this discrepancy. This information asymmetry causes a lack of efficiency in the price and number of goods and services provided. For example, in the used car market, the seller may be aware of defects in the vehicle but may not disclose them, charging the buyer more than the car is worth. In the insurance industry, adverse selection can occur when there is an imbalance between high-risk and low-risk policyholders, with more high-risk individuals purchasing insurance, leading to higher premiums for all policyholders.

Overcoming Moral Hazard in Insurance

To overcome moral hazard in insurance, companies can reward good behaviour and penalize bad behaviour with higher rates or fees. Additionally, insurance companies can introduce co-pay and deductibles, requiring individuals to partially pay for the services they receive, encouraging them to avoid making unnecessary claims.

Filing Insurance Claims: Timely Filing for Recouping Money

You may want to see also

Frequently asked questions

A moral hazard is a situation where an individual has an incentive to take on more risk because they are protected from any potential consequences. In insurance, this means that the insured party may be more inclined to take risks because they know that the insurer will bear the costs if things go wrong.

Asymmetric information occurs when one party in a transaction has more information about their intentions or the situation than the other party. This can lead to moral hazard because the party with more information may have an incentive to act in a way that increases the risk for the other party.

Moral hazard is particularly relevant in the insurance industry because insurance companies offer protection against risks. When individuals are insured, they may be more inclined to take risks, knowing that the insurer will cover any losses. This can lead to increased claims and costs for insurance companies.

There are several strategies to reduce moral hazard, including:

- Incentives: Creating incentives for individuals to avoid taking excessive risks.

- Policies: Implementing policies to prevent immoral or illegal behaviour.

- Monitoring: Regularly monitoring the actions and behaviours of individuals to identify and mitigate potential risks.

- Deductibles and co-pays: In health insurance, instituting deductibles or co-pays can help reduce moral hazard by requiring individuals to pay for a portion of the services they receive, incentivizing them to avoid making unnecessary claims.