Prepaid insurance refers to the practice of paying for insurance coverage in advance, typically for a specified period such as six months or a year. This approach offers several advantages, including potential cost savings through discounts for upfront payments, improved cash flow management by avoiding monthly premiums, and the convenience of not having to remember recurring payments. Understanding how to effectively manage prepaid insurance involves knowing the types of policies that allow prepayment, such as auto, home, or health insurance, and being aware of the terms and conditions, including refund policies if coverage is canceled early. Additionally, it’s important to assess your financial situation to ensure prepayment aligns with your budget and long-term goals. By mastering the process, individuals and businesses can optimize their insurance expenses while maintaining continuous coverage.

| Characteristics | Values |

|---|---|

| Definition | Prepaid insurance refers to insurance premiums paid in advance for a specific period, typically a year or more. |

| Purpose | To ensure continuous coverage and avoid lapses in insurance protection. |

| Payment Frequency | One-time payment for the entire coverage period. |

| Common Types | General liability, property, health, and life insurance. |

| Accounting Treatment | Recorded as an asset (prepaid expense) on the balance sheet and expensed over the coverage period. |

| Benefits | Cost savings (discounts for upfront payment), convenience, and guaranteed coverage. |

| Drawbacks | Reduced cash flow flexibility, potential for overpayment if circumstances change. |

| Renewal Process | Policyholder must renew or cancel before the prepaid period ends to avoid automatic renewal. |

| Refund Policy | Partial refunds may be available if the policy is canceled before the end of the prepaid period, subject to terms. |

| Tax Implications | Prepaid insurance premiums may be tax-deductible in the year paid, depending on jurisdiction and policy type. |

| Documentation | Receipts, invoices, and policy documents should be retained for accounting and tax purposes. |

| Latest Trend | Increasing adoption of digital platforms for prepaid insurance purchases and management. |

Explore related products

![Property and Casualty Insurance License Exam Study Guide: Property Casualty Insurance Book and Practice Test Questions [3rd Edition]](https://m.media-amazon.com/images/I/71MhA+5nDML._AC_UY218_.jpg)

What You'll Learn

![]()

Understanding Prepaid Insurance Basics

Prepaid insurance is essentially a financial strategy where you pay for coverage in advance, typically for a defined period like six months or a year. This upfront payment differs from traditional monthly premiums, offering both advantages and considerations. For instance, many auto insurance providers offer discounts for paying the full term premium at once, which can save you 5-10% annually. However, this requires careful budgeting to ensure the lump sum doesn’t strain your finances.

Analyzing the mechanics, prepaid insurance operates on the principle of prepayment for future protection. When you purchase a prepaid policy, the insurer records it as a current asset on your balance sheet, gradually expensing it over the coverage period. For example, if you prepay $1,200 for a year of health insurance, $100 is expensed monthly as the coverage is consumed. This method aligns with the accounting principle of matching expenses to the period they benefit, providing a clearer financial picture for businesses and individuals alike.

From a practical standpoint, prepaid insurance is particularly beneficial for long-term policies like life or property insurance. It eliminates the risk of missed payments, which could lead to policy lapses or penalties. For instance, a 30-year-old purchasing a 20-year term life insurance policy might opt to prepay annually to lock in rates and avoid potential premium increases. However, it’s crucial to review the insurer’s cancellation policy, as some may not refund the full prepaid amount if you terminate early.

Comparatively, prepaid insurance contrasts with pay-as-you-go models, where premiums are paid monthly or quarterly. While the latter offers flexibility, prepaid options often come with discounts and simplify financial planning. For example, a small business prepaying its general liability insurance can avoid monthly billing fluctuations and allocate resources more efficiently. Yet, it’s essential to assess cash flow stability before committing to a large upfront payment, as liquidity can be temporarily reduced.

In conclusion, understanding prepaid insurance basics involves recognizing its cost-saving potential, accounting implications, and practical benefits. Whether for personal or business use, it’s a strategic choice that requires balancing upfront savings against cash flow needs. By evaluating your financial situation and policy terms, you can determine if prepaying insurance aligns with your long-term goals. Always consult with an insurance advisor to tailor the approach to your specific needs.

Life Insurance and Suicide: What Coverage Entails

You may want to see also

Explore related products

![]()

Calculating Prepaid Insurance Premiums

Prepaid insurance premiums are a forward-thinking approach to managing financial obligations, but their calculation requires precision to avoid overpayment or undercoverage. The process begins with identifying the policy’s coverage period and aligning it with your accounting cycle. For instance, if you pay $1,200 annually for general liability insurance starting January 1, but your fiscal year ends March 31, only $300 (three months) should be recorded as a prepaid expense. The remaining $900 is classified as an asset on your balance sheet, gradually expensed over the subsequent months. This method ensures compliance with accrual accounting principles and provides a clear financial snapshot.

To calculate prepaid insurance premiums accurately, follow these steps: first, determine the total premium cost and the policy’s duration. Divide the total cost by the number of months covered to find the monthly premium. For example, a $2,400 annual policy divided by 12 months equals $200 per month. Next, assess how many months fall within the current accounting period. If four months of coverage overlap, record $800 as an expense and the remaining $1,600 as prepaid insurance. This systematic approach prevents errors and ensures consistency in financial reporting.

A common pitfall in calculating prepaid insurance premiums is neglecting prorated adjustments for partial periods. For instance, if a policy is purchased mid-month, the premium for that month should be prorated based on the number of days covered. A $300 monthly premium for a policy starting on the 15th of a 30-day month would be adjusted to $150 (15/30). Failing to prorate can distort expense recognition and misrepresent financial health. Always verify the exact start and end dates of the policy to maintain accuracy.

Finally, leverage accounting software or spreadsheets to streamline the calculation process. Tools like QuickBooks or Excel templates can automate prorated adjustments and track prepaid balances over time. For small businesses, this reduces manual errors and saves time. Additionally, regularly review prepaid insurance accounts during month-end closings to ensure proper allocation. By mastering these calculations, you not only optimize cash flow but also enhance the reliability of your financial statements, fostering trust among stakeholders.

Life Insurance: A Necessary Safety Net?

You may want to see also

Explore related products

![]()

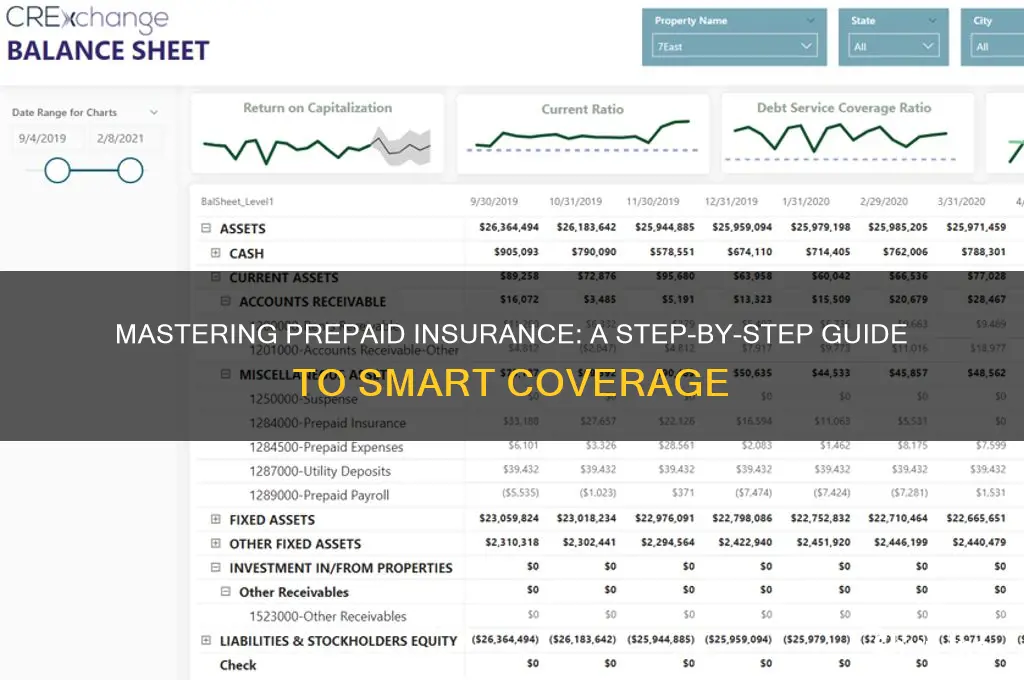

Recording Prepaid Insurance in Accounting

Prepaid insurance is an asset on a company’s balance sheet, representing coverage paid for in advance. Recording it correctly ensures financial statements reflect accurate expenses and asset values over time. When a business pays for insurance upfront, the full amount isn’t expensed immediately; instead, it’s allocated to the periods it covers. For example, a $12,000 annual policy paid in January would be recorded as a $1,000 monthly expense, with the remaining $11,000 held as a prepaid asset until it’s used.

The process begins with a journal entry to recognize the prepaid asset. Debit the prepaid insurance account (an asset) and credit cash or the payment method used. For instance, if a company pays $6,000 for a six-month policy, the entry would be: *Debit Prepaid Insurance $6,000, Credit Cash $6,000*. This records the expenditure without immediately affecting the income statement. As each month passes, adjust the accounts to reflect the expense. For the same policy, a monthly adjusting entry would be: *Debit Insurance Expense $1,000, Credit Prepaid Insurance $1,000*. This method aligns expenses with the period they benefit, adhering to the matching principle in accounting.

Mistakes in recording prepaid insurance can distort financial statements. Overstating expenses in the initial period misrepresents profitability, while failing to adjust monthly leads to underreporting expenses in subsequent periods. Small businesses, in particular, must be vigilant, as errors can affect tax liabilities and cash flow projections. For instance, a $10,000 policy expensed entirely in January instead of over 12 months would inflate January’s expenses by $8,500, skewing quarterly reports.

To streamline the process, leverage accounting software with recurring transaction features. Tools like QuickBooks or Xero allow automated adjusting entries, reducing manual errors. For businesses with multiple policies, create a prepaid insurance schedule to track expiration dates and monthly allocations. Regularly reconcile this schedule with the general ledger to ensure accuracy. For example, a company with three policies totaling $24,000 annually can use a spreadsheet to allocate $2,000 monthly, simplifying year-end adjustments.

In conclusion, recording prepaid insurance requires precision and consistency. By understanding the initial entry, monthly adjustments, and potential pitfalls, businesses can maintain accurate financial records. This not only ensures compliance with accounting standards but also provides a clear picture of financial health, aiding decision-making and stakeholder trust.

Does Insurance Double: Unraveling the Myth of Duplicate Coverage Benefits

You may want to see also

Explore related products

![]()

Amortizing Prepaid Insurance Costs

Prepaid insurance costs represent an asset on a company’s balance sheet, reflecting coverage paid for in advance. Amortization systematically reduces this asset over time, matching expenses to the periods benefiting from the insurance. For example, a $12,000 annual policy paid upfront in January would be expensed at $1,000 monthly, aligning with accrual accounting principles. This process ensures financial statements accurately reflect the economic reality of insurance consumption.

The mechanics of amortizing prepaid insurance are straightforward but require consistency. First, determine the total cost of the prepaid insurance policy. Next, divide this amount by the number of months (or periods) the policy covers. Record the resulting monthly expense as a debit to "Insurance Expense" and a credit to "Prepaid Insurance." For instance, a $6,000 six-month policy would be amortized at $1,000 per month. This method avoids distorting financial results by expensing the entire cost in a single period.

A common pitfall in amortizing prepaid insurance is neglecting to adjust for policy changes or cancellations. If a policy is canceled mid-term, the unamortized portion must be expensed immediately. For example, canceling a $12,000 annual policy after six months would require expensing the remaining $6,000 in that period. Similarly, policy modifications, such as coverage extensions or premium adjustments, necessitate recalculating the amortization schedule to maintain accuracy.

From a strategic perspective, amortizing prepaid insurance enhances financial transparency and decision-making. By spreading costs evenly, businesses avoid artificial spikes in expenses and gain a clearer view of monthly or quarterly financial performance. This approach also facilitates budgeting and forecasting, as insurance costs become predictable line items. For small businesses or startups, mastering this process can improve cash flow management and investor confidence.

In practice, leveraging accounting software can streamline prepaid insurance amortization. Tools like QuickBooks or Xero allow users to set up recurring journal entries, automating the process and reducing manual errors. For businesses with multiple policies, creating a centralized spreadsheet to track start dates, durations, and amortization schedules can provide additional oversight. Regularly reconciling prepaid insurance accounts ensures discrepancies are caught early, maintaining the integrity of financial records.

Is Americo Insurance Legit? A Comprehensive Review and Analysis

You may want to see also

Explore related products

![]()

Renewing and Managing Prepaid Policies

Prepaid insurance policies offer a unique advantage: predictable costs and peace of mind. However, their value hinges on proactive renewal and management. Unlike traditional policies, prepaid plans often require annual or periodic renewal, demanding attention to avoid coverage lapses.

Understanding Renewal Timelines:

Most prepaid policies have fixed terms, typically 6 to 12 months. Mark your calendar 30–60 days before expiration to allow time for review and payment. Insurers usually send reminders, but relying solely on these can be risky. For example, a missed email or postal delay could result in a gap in coverage. Use digital tools like calendar alerts or budgeting apps to track renewal dates.

Evaluating Policy Needs Annually:

Renewal is an opportunity to reassess your coverage. Life changes—a new car, home renovations, or a growing family—may necessitate adjustments. For instance, a prepaid auto insurance policy might need higher liability limits if you’ve purchased a more expensive vehicle. Conversely, if your risk profile has decreased, you could explore downgrading to save costs.

Managing Payments Strategically:

Prepaid policies often require full payment upfront, which can strain finances. Some insurers offer installment options, but these may incur fees. If paying in full, align the renewal date with a month when cash flow is typically higher. Alternatively, set aside a monthly amount in a dedicated savings account to cover the cost when due.

Avoiding Common Pitfalls:

One major mistake is assuming automatic renewal. While some insurers offer this, many require explicit consent. Another pitfall is neglecting to update personal details, such as address or vehicle information, which can invalidate coverage. Always review policy documents thoroughly before renewing.

Leveraging Technology for Efficiency:

Many insurers now provide online portals or mobile apps for policy management. These platforms allow you to view coverage details, update information, and renew policies seamlessly. For example, Progressive’s app lets users upload photos of vehicle damage for faster claims processing. Embracing these tools can streamline management and reduce administrative burdens.

By staying organized, reassessing needs annually, and leveraging available resources, you can maximize the benefits of prepaid insurance while minimizing risks. Proactive management ensures continuous coverage and financial stability, making prepaid policies a reliable choice for long-term protection.

The Cost of Mortgage Life Insurance: What You Need to Know

You may want to see also

Frequently asked questions

Prepaid insurance refers to insurance premiums paid in advance for coverage that extends into future accounting periods. It works by recording the prepaid amount as an asset on the balance sheet, and then gradually expensing it over the coverage period.

To record prepaid insurance, debit the prepaid insurance account (an asset) and credit the cash or bank account for the payment. As the coverage period progresses, periodically debit insurance expense and credit prepaid insurance to reflect the used portion.

Whether prepaid insurance can be refunded depends on the insurer’s policy. Some insurers may refund the unused portion of the premium, while others may deduct fees or penalties. Check your policy terms for specifics.

Prepaid insurance initially increases assets (prepaid insurance) and decreases cash (or bank balance). Over time, as the expense is recognized, it reduces the prepaid insurance asset and increases insurance expense on the income statement. This ensures accurate matching of expenses with revenues.

![TracFone Motorola Moto g 5G (2024) [Activation Promotion] Locked Prepaid Smartphone, 128GB, Gray - Includes $20 Unlimited Talk, Text, & 4GB Data 30-Day Plan](https://m.media-amazon.com/images/I/71y7mfjjN1L._AC_UY218_.jpg)