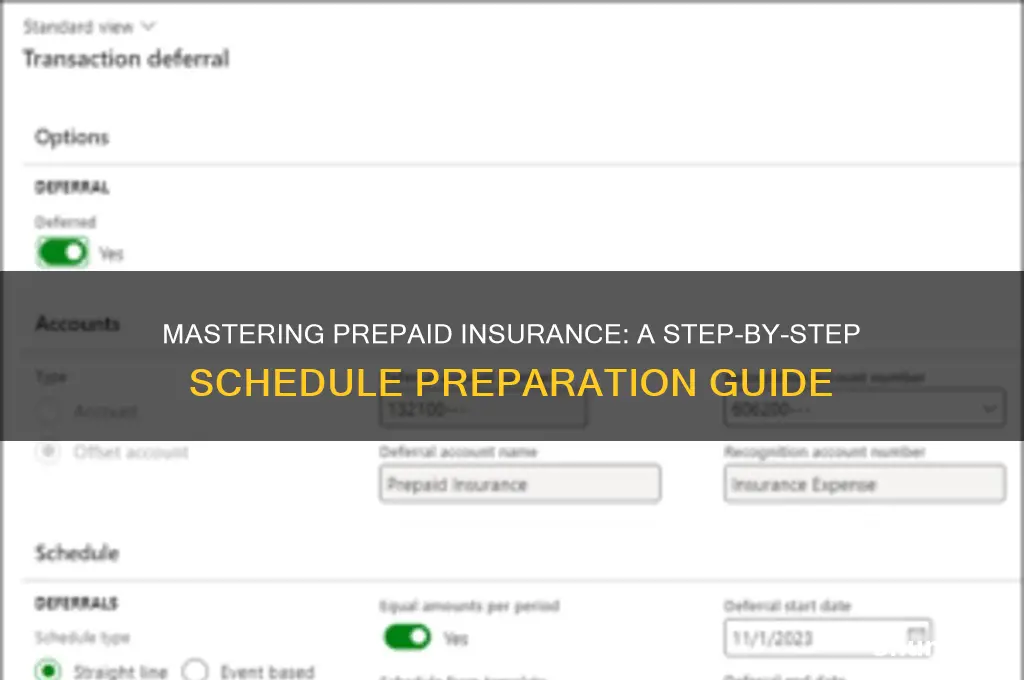

Preparing a prepaid insurance schedule is a critical task for businesses to accurately track and allocate insurance expenses over the appropriate accounting periods. This schedule ensures that prepaid insurance, which represents coverage paid in advance, is systematically recognized as an expense rather than an asset over time. To create the schedule, start by identifying all prepaid insurance policies, noting their coverage periods, total cost, and payment dates. Next, determine the portion of the insurance that applies to the current accounting period and the amount that will be expensed in future periods. Organize this information in a structured format, typically a spreadsheet or table, with columns for policy details, total cost, expiration date, and monthly or periodic expense allocations. Regularly update the schedule to reflect any changes in policies or coverage periods, ensuring compliance with accounting principles like GAAP or IFRS. Properly maintaining a prepaid insurance schedule not only enhances financial accuracy but also aids in budgeting, forecasting, and audit preparedness.

| Characteristics | Values |

|---|---|

| Purpose | To track prepaid insurance expenses and allocate them over the coverage period. |

| Key Components | Policy details, payment date, coverage period, total premium, monthly allocation. |

| Data Required | Insurance policy documents, payment receipts, coverage start and end dates. |

| Calculation Method | Divide the total premium by the number of months in the coverage period. |

| Frequency of Preparation | Annually or at the start of each insurance policy period. |

| Accounting Treatment | Prepaid insurance is recorded as an asset and amortized over time. |

| Journal Entry | Debit Prepaid Insurance, Credit Cash (at payment); Debit Insurance Expense, Credit Prepaid Insurance (monthly). |

| Software Tools | Excel, accounting software (QuickBooks, Xero), or ERP systems. |

| Compliance | Follow GAAP or IFRS guidelines for prepaid expense recognition. |

| Review and Adjustment | Periodically review for accuracy and adjust for policy changes or cancellations. |

| Documentation | Maintain policy documents, receipts, and amortization schedules for audit purposes. |

Explore related products

What You'll Learn

- Identify Policies: List all active insurance policies with prepaid premiums

- Determine Coverage Periods: Note start and end dates for each policy

- Calculate Prepaid Amounts: Allocate premiums across coverage periods accurately

- Organize by Month: Distribute prepaid expenses monthly for financial tracking

- Review and Update: Regularly verify and adjust the schedule for accuracy

![]()

Identify Policies: List all active insurance policies with prepaid premiums

The first step in preparing a prepaid insurance schedule is to identify all active insurance policies with prepaid premiums. This involves a comprehensive review of your organization's insurance portfolio, ensuring no policy is overlooked. Begin by gathering all insurance documents, including policy summaries, invoices, and payment records. For larger organizations, this might require coordination across departments or subsidiaries to centralize information. A systematic approach, such as categorizing policies by type (e.g., property, liability, health) or insurer, can streamline the process. For instance, a mid-sized company might use a spreadsheet to log policies, noting details like policy number, insurer, coverage period, and premium amount. This initial step is critical, as missing policies can lead to inaccurate financial reporting and compliance issues.

Analyzing the gathered data reveals patterns and potential discrepancies. For example, a policy with a prepaid premium might cover a multi-year period, requiring prorated allocation across fiscal years. Consider a life insurance policy with a $12,000 premium paid upfront for a 3-year term. In a prepaid insurance schedule, $4,000 would be allocated annually as an asset, with the remaining balance expensed over time. This analysis ensures compliance with accounting standards like GAAP or IFRS, which mandate the matching of expenses to the periods they benefit. Tools like accounting software or ERP systems can automate this process, reducing manual errors. However, smaller organizations might rely on manual calculations, emphasizing the need for meticulous record-keeping.

A persuasive argument for thorough policy identification lies in its impact on financial health and decision-making. Accurate prepaid insurance schedules provide a clear picture of future liabilities and assets, aiding in budgeting and forecasting. For instance, a manufacturing company with prepaid workers’ compensation insurance can anticipate reduced cash outflows in subsequent periods. Conversely, overlooking a prepaid policy might lead to overestimating expenses, distorting financial statements. Stakeholders, from investors to auditors, rely on this accuracy to assess organizational stability. Thus, investing time in this step is not just a compliance requirement but a strategic imperative for informed financial management.

Comparing manual and digital methods for policy identification highlights efficiency gains. Manual methods, while cost-effective, are prone to human error and time-consuming. For example, a sole proprietor might spend hours sifting through paper documents to identify prepaid policies. In contrast, digital solutions like cloud-based insurance management platforms offer real-time updates, automated reminders, and integration with accounting systems. A case study of a small business transitioning to digital tools showed a 40% reduction in time spent on insurance administration. However, digital adoption requires upfront investment and staff training, making it a long-term strategy. Organizations must weigh these trade-offs based on their size, complexity, and technological readiness.

In conclusion, identifying active insurance policies with prepaid premiums is a foundational yet nuanced task in preparing a prepaid insurance schedule. It demands attention to detail, analytical rigor, and strategic foresight. Whether through manual diligence or digital innovation, the goal remains the same: to create a transparent, compliant, and actionable financial record. By mastering this step, organizations not only meet accounting standards but also unlock insights that drive smarter financial decisions. Practical tips, such as maintaining a centralized policy repository and regularly reconciling records, can further enhance efficiency. Ultimately, this process transforms raw data into a powerful tool for financial stewardship.

Leaving a Universal Life Insurance Legacy for Your Children

You may want to see also

Explore related products

![]()

Determine Coverage Periods: Note start and end dates for each policy

Accurate coverage periods are the backbone of a prepaid insurance schedule. Omitting or misstating policy start and end dates can lead to overpayment, coverage gaps, or compliance issues. Each policy document explicitly states these dates, typically on the declarations page. Extract this information meticulously, ensuring alignment with the insurer's records. Double-check for amendments or endorsements that might alter the original terms.

Consider a scenario where a company purchases a general liability policy effective January 1, 2023, with a 12-month term. However, a mid-year endorsement extends coverage to include cyber liability, implicitly extending the policy period for this specific provision. Failing to note this adjustment could result in underreporting prepaid expenses or misclassifying liabilities. Always cross-reference the original policy with any subsequent changes to capture the full coverage timeline.

When dealing with multi-year policies, such as a three-year director and officer (D&O) insurance contract, allocate the prepaid expense proportionally across the coverage period. For instance, a $90,000 premium for a policy spanning 2023–2025 should be recognized as $30,000 annually. This approach adheres to the matching principle, aligning expenses with the periods they cover. Use spreadsheet tools to automate calculations, reducing the risk of manual errors.

Beware of policies with staggered coverage periods or overlapping terms. For example, a company might renew a property insurance policy mid-year while maintaining an active workers’ compensation policy with a different cycle. Clearly delineate these timelines to avoid double-counting or omitting prepaid amounts. Color-coding or using distinct identifiers in your schedule can enhance clarity and prevent confusion during audits.

Finally, reconcile coverage periods with accounting cycles to ensure compliance with GAAP or IFRS. Prepaid insurance should be recorded as an asset and amortized over the coverage period. For instance, a six-month auto insurance policy paid in full in Q1 should be expensed at $1/6 of the total premium each month. Regularly update the schedule to reflect renewals, cancellations, or policy modifications, maintaining a dynamic and accurate financial record.

Nuclear Reactors: Insured Against the Unthinkable?

You may want to see also

Explore related products

![]()

Calculate Prepaid Amounts: Allocate premiums across coverage periods accurately

Accurate allocation of prepaid insurance premiums across coverage periods is critical for financial reporting and compliance. Missteps here can lead to overstated expenses, understated assets, or audit adjustments. The core challenge lies in matching the timing of premium payments with the actual periods they cover, especially when policies span multiple accounting cycles. For instance, a $12,000 annual premium paid in January for a policy effective January 1 to December 31 must be systematically allocated to each month, recognizing $1,000 as an expense and $11,000 as a prepaid asset initially.

To achieve this, begin by identifying the policy’s effective dates and total premium cost. Divide the premium by the total coverage months to determine the monthly allocation. For example, a $6,000 six-month policy paid upfront would allocate $1,000 per month. Record the current month’s portion as an expense and the remaining balance as a prepaid asset. Use a prepaid insurance schedule to track these amounts, ensuring each month’s entry reduces the prepaid balance while increasing the expense account. This method aligns with the matching principle, ensuring expenses are recognized in the periods they benefit.

A common pitfall is neglecting to adjust for partial periods or policy changes mid-year. If a policy is canceled or modified, recalculate the allocation based on the revised coverage period. For example, if a $3,000 quarterly policy is canceled after two months, recognize $1,000 as expense for the first month, $1,000 for the second, and reclassify the remaining $1,000 as a refundable asset or expense, depending on the insurer’s policy. Failure to adjust can distort financial statements and misrepresent financial health.

Leverage accounting software or spreadsheets to automate these calculations and maintain accuracy. Tools like Excel or QuickBooks allow for dynamic adjustments and reduce manual errors. For instance, create a spreadsheet with columns for policy details, premium amounts, coverage periods, monthly allocations, and running prepaid balances. Update this schedule monthly to reflect actuals and ensure consistency. Regularly reconcile the prepaid account to the general ledger to catch discrepancies early.

In conclusion, precise allocation of prepaid insurance premiums requires a structured approach, attention to detail, and adaptability to changes. By systematically dividing premiums across coverage periods, maintaining a detailed schedule, and leveraging technology, businesses can ensure compliance, accurate financial reporting, and informed decision-making. This process not only enhances transparency but also builds trust with stakeholders by demonstrating fiscal responsibility.

Cashing in Life Insurance: What's the Tax Impact?

You may want to see also

Explore related products

![]()

Organize by Month: Distribute prepaid expenses monthly for financial tracking

Prepaid insurance expenses often represent a significant financial commitment, yet their impact on monthly cash flow can be obscured without proper organization. By distributing these expenses across the months they cover, businesses gain a clearer picture of their financial obligations and can make more informed decisions. This method, known as monthly allocation, transforms a lump-sum payment into a series of manageable entries, aligning with the period in which the insurance coverage is actually utilized.

Consider a $12,000 annual insurance premium paid upfront in January. Instead of recording the entire amount as a January expense, allocate $1,000 to each month. This approach reflects the true cost of insurance for that period, providing a more accurate representation of monthly expenses. For instance, a small business with tight cash flow can better anticipate and plan for these recurring costs, avoiding unexpected financial strain.

To implement this strategy, start by identifying the coverage period of the prepaid insurance. Divide the total cost by the number of months covered. For example, a six-month policy costing $6,000 would be allocated at $1,000 per month. Record these entries in your accounting system as monthly expenses, ensuring consistency and accuracy. Tools like accounting software can automate this process, reducing the risk of errors and saving time.

However, this method requires discipline and attention to detail. Ensure that the allocation aligns precisely with the coverage period to avoid misrepresenting financial data. For instance, a policy that starts mid-month should be prorated accordingly. Additionally, regularly review the schedule to account for any policy changes or renewals, maintaining the integrity of your financial records.

By organizing prepaid insurance expenses monthly, businesses not only improve financial transparency but also enhance budgeting and forecasting capabilities. This approach transforms a static expense into a dynamic tool for financial management, enabling better decision-making and long-term planning. It’s a simple yet powerful strategy that bridges the gap between upfront payments and their ongoing value.

Primerica Life Insurance: Application Process Simplified

You may want to see also

Explore related products

![]()

Review and Update: Regularly verify and adjust the schedule for accuracy

Maintaining an accurate prepaid insurance schedule is not a set-it-and-forget-it task. Regular reviews are essential to ensure the schedule reflects current realities and remains a reliable tool for financial planning. Think of it as a living document, constantly evolving alongside your business and the insurance landscape.

Neglecting updates can lead to costly errors. Overlooking policy renewals, premium changes, or coverage adjustments can result in underpayment, overpayment, or even coverage gaps. Imagine discovering a critical policy has lapsed due to an outdated schedule – a scenario easily avoided with consistent reviews.

The frequency of reviews depends on your business's complexity and the volatility of your insurance needs. A quarterly review is a good starting point for most businesses, allowing for adjustments based on seasonal fluctuations or recent policy changes. However, businesses with frequent policy modifications or high-risk operations might benefit from monthly reviews.

Set a recurring calendar reminder to ensure reviews don't slip through the cracks.

During each review, meticulously compare the schedule against actual insurance documents. Verify policy numbers, coverage limits, premiums, payment due dates, and expiration dates. Look for discrepancies, such as policies no longer in force, changes in premium amounts, or newly acquired policies not yet reflected.

Don't just identify discrepancies – act on them. Update the schedule immediately, ensuring all changes are clearly documented and dated. Consider using color-coding or highlighting to visually distinguish recent updates for easy reference.

By making regular reviews a priority, you transform your prepaid insurance schedule from a static record into a dynamic tool. This proactive approach minimizes financial risks, ensures compliance, and provides a clear picture of your insurance obligations, ultimately contributing to the financial health and stability of your business.

Life Insurance: Pitching for Protection

You may want to see also

Frequently asked questions

A prepaid insurance schedule is a detailed record of prepaid insurance premiums, showing the portion of coverage that applies to future accounting periods. It is important for accurate financial reporting, as it ensures that expenses are recognized in the correct period, aligning with the matching principle in accounting.

To prepare a prepaid insurance schedule, gather the insurance policy details, including the start date, end date, and total premium paid. Allocate the premium over the coverage period, typically on a monthly basis. Create a table listing the months, the portion of the premium applicable to each month, and the cumulative amount expensed or remaining as prepaid.

You will need the insurance policy start and end dates, the total premium paid, and the accounting period for which you are preparing the schedule. Additionally, ensure you have the company’s fiscal year-end date to accurately allocate expenses across periods.