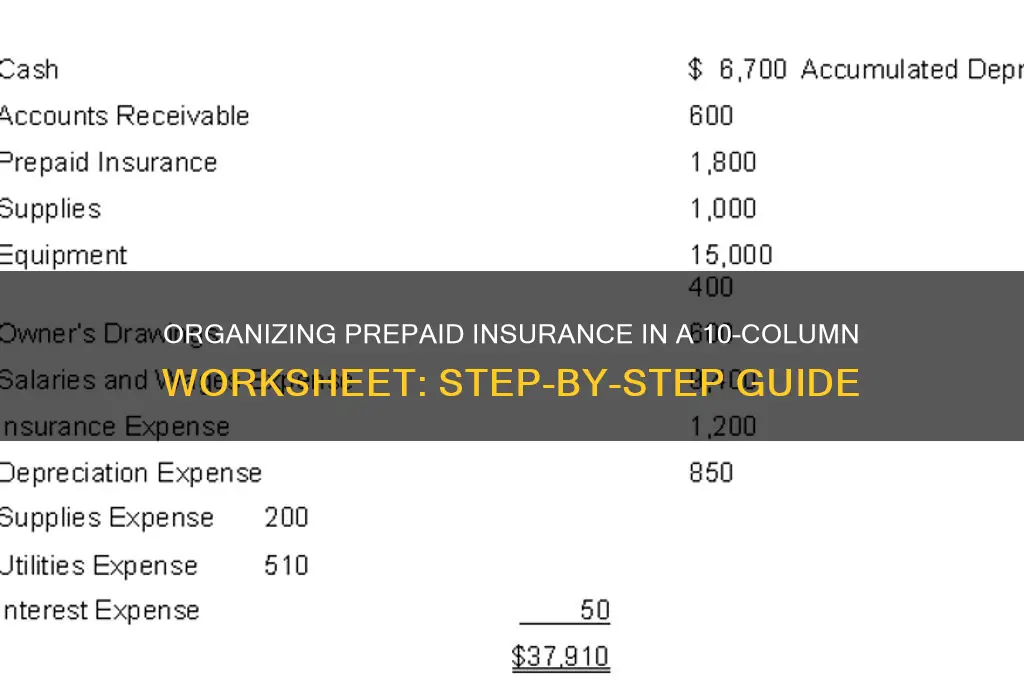

Putting prepaid insurance into a 10-column worksheet requires careful organization to accurately reflect the financial transaction. Prepaid insurance is an asset representing insurance coverage paid in advance, and it must be properly recorded to ensure compliance with accounting principles. In a 10-column worksheet, typically used for manual accounting, the entry involves debiting the prepaid insurance account (an asset) and crediting the cash account (a decrease in cash). The worksheet columns, such as date, account title, debit, credit, and description, must be filled out methodically to track the transaction. Additionally, as the insurance coverage is consumed over time, adjusting entries will be necessary to move the expense from the prepaid account to the insurance expense account, ensuring the financial statements accurately reflect the period’s usage. Understanding this process is crucial for maintaining precise financial records and adhering to accounting standards.

| Characteristics | Values |

|---|---|

| Account Type | Asset (Prepaid Insurance) |

| Column 1 | Date of Transaction |

| Column 2 | Description (e.g., "Prepaid Insurance - [Policy Name]") |

| Column 3 | Posting Reference (e.g., Invoice/Receipt Number) |

| Column 4 | Debit Amount (Full prepaid amount) |

| Column 5 | Credit Amount (Leave blank or 0) |

| Column 6 | Account Number (Prepaid Insurance account number) |

| Column 7 | Department/Division (if applicable) |

| Column 8 | Job/Project (if applicable) |

| Column 9 | Memo/Notes (e.g., Policy period, insurer details) |

| Column 10 | Total (Auto-calculated, matches debit amount) |

| Journal Entry | Debit: Prepaid Insurance Credit: Cash/Bank Account |

| Amortization | Monthly/Periodic adjustment to Insurance Expense and Prepaid Insurance |

| Example Entry | Date: 01/01/2023 Description: Prepaid Insurance - General Liability Debit: $1,200 Credit: $0 Account: 101-Prepaid Insurance |

| Frequency | Typically recorded annually or as per policy term |

| Supporting Docs | Insurance Policy, Invoice, Payment Receipt |

| Compliance | Follow GAAP/IFRS for prepaid expense recognition |

Explore related products

What You'll Learn

- Column Setup: Label columns for date, description, account, debit, credit, balance, policy, amount, expiration, notes

- Recording Premiums: Enter prepaid insurance payment in debit column, credit cash/bank account

- Monthly Adjustments: Allocate expense monthly, debit insurance expense, credit prepaid insurance account

- Tracking Expiration: Note policy end date in expiration column for renewal tracking

- Reconciliation: Verify balances monthly, ensure accuracy in prepaid insurance and expense accounts

![]()

Column Setup: Label columns for date, description, account, debit, credit, balance, policy, amount, expiration, notes

When setting up a 10-column worksheet to track prepaid insurance, the first step is to clearly label each column to ensure accurate and organized record-keeping. Begin by labeling the first column as Date, where you will record the transaction date for each entry related to the prepaid insurance. This column is crucial for chronological tracking and financial reporting. Next, label the second column as Description, which will provide a brief but clear explanation of the transaction, such as "Prepaid Insurance for Office Policy" or "Monthly Insurance Premium Payment." This helps in quickly identifying the purpose of each entry.

The third column should be labeled Account, where you specify the account affected by the transaction, typically "Prepaid Insurance" or "Insurance Expense." This ensures proper categorization in your accounting system. The fourth and fifth columns are Debit and Credit, respectively, which are essential for double-entry bookkeeping. When recording prepaid insurance, the debit entry will increase the prepaid insurance asset account, while the credit entry will decrease the cash or bank account. These columns are fundamental for maintaining balance in your financial records.

The sixth column, Balance, will track the remaining prepaid insurance amount after each transaction. This column is updated each time a portion of the prepaid insurance is expensed over time. The seventh column, Policy, should include the specific insurance policy number or identifier, ensuring that each entry is linked to the correct policy. This is particularly useful if you manage multiple insurance policies. The eighth column, Amount, records the total amount paid for the prepaid insurance or the portion expensed during the period.

The ninth column, Expiration, is critical for prepaid insurance tracking, as it indicates the date when the insurance coverage ends. This helps in monitoring when the prepaid insurance will need to be renewed or replaced. Finally, the tenth column, Notes, provides space for additional information or context, such as payment terms, insurer details, or any unusual circumstances related to the transaction. Properly labeling and utilizing these columns ensures that your prepaid insurance transactions are accurately recorded, easily traceable, and compliant with accounting standards.

FHA and VA Loan Insurance: What Borrowers Need to Know

You may want to see also

Explore related products

![]()

Recording Premiums: Enter prepaid insurance payment in debit column, credit cash/bank account

When recording prepaid insurance in a 10-column worksheet, the first step is to understand the nature of the transaction. Prepaid insurance represents the payment made in advance for insurance coverage that will benefit future accounting periods. To record this transaction, you must debit the prepaid insurance account and credit the cash or bank account from which the payment is made. This process ensures that the asset (prepaid insurance) is properly recognized on the balance sheet, while the reduction in cash is accurately reflected.

In the 10-column worksheet, locate the appropriate columns for the journal entry. The debit column for the prepaid insurance account and the credit column for the cash or bank account are where the amounts will be recorded. For example, if a company pays $1,200 for a one-year insurance policy in advance, the prepaid insurance account is debited by $1,200, and the cash account is credited by the same amount. This entry is made in the respective columns, ensuring that the total debits equal the total credits, maintaining the accounting equation’s balance.

The debit to the prepaid insurance account increases the asset account, reflecting the value of the insurance coverage that has been paid for but not yet used. Simultaneously, the credit to the cash or bank account reduces the balance in that account, accurately representing the outflow of funds. This dual entry ensures that the transaction is recorded in accordance with the accrual basis of accounting, where expenses are matched with the periods they benefit.

It’s important to ensure that the amounts entered in the debit and credit columns are accurate and consistent. Double-check the figures to avoid errors that could disrupt the balance of the worksheet. Additionally, include a brief description of the transaction in the description or particulars column to provide context for the entry. This practice enhances clarity and makes it easier to trace the transaction if needed in the future.

Finally, after recording the entry, verify that the totals of the debit and credit columns match. This step is crucial in a 10-column worksheet to maintain the integrity of the accounting records. Properly recording prepaid insurance payments in this manner not only ensures compliance with accounting principles but also provides a clear financial picture of the company’s assets and cash flow. By following these steps, you can accurately and efficiently record prepaid insurance transactions in a 10-column worksheet.

Health Insurance: A Key to Longevity?

You may want to see also

Explore related products

![]()

Monthly Adjustments: Allocate expense monthly, debit insurance expense, credit prepaid insurance account

When managing prepaid insurance in a 10-column worksheet, Monthly Adjustments are crucial to accurately reflect the expense over time. The primary goal is to allocate the prepaid insurance cost monthly, ensuring that the expense is recognized in the period it benefits. To achieve this, you must debit the Insurance Expense account and credit the Prepaid Insurance account each month. This process adjusts the books to match the accrual accounting principle, where expenses are recorded when incurred, not when paid.

Begin by determining the monthly portion of the prepaid insurance. For example, if you prepaid $1,200 for a year of insurance, the monthly allocation would be $100 ($1,200 ÷ 12). In your 10-column worksheet, locate the Insurance Expense column under the expense section and the Prepaid Insurance column under the asset section. In the first column (typically the date column), enter the date of the adjustment, usually the last day of the month. In the description or account title column, clearly note "Monthly Insurance Expense Adjustment."

Next, in the Insurance Expense column, debit the monthly amount (e.g., $100). This increases the expense account, reflecting the cost incurred during the month. Simultaneously, in the Prepaid Insurance column, credit the same amount (e.g., $100). This reduces the prepaid insurance asset, as a portion of it has been used up. Ensure the debit and credit amounts match to maintain the accounting equation balance.

Repeat this process each month until the prepaid insurance is fully expensed. For instance, after 12 months, the Prepaid Insurance account will have a zero balance, and the total Insurance Expense for the year will equal the original prepaid amount. This method ensures that the financial statements accurately represent the business's financial position and performance over time.

Finally, in the 10-column worksheet, ensure that the balancing columns (debit and credit totals) are updated accordingly. The debit to Insurance Expense and credit to Prepaid Insurance should appear in the respective columns, with the totals reflecting the monthly adjustments. This systematic approach not only keeps the books accurate but also simplifies year-end reporting and audits. By following these steps, you effectively allocate prepaid insurance expenses monthly, maintaining compliance with accounting standards.

Irrevocable Life Insurance Trusts: Can They Be Invaded?

You may want to see also

Explore related products

![]()

Tracking Expiration: Note policy end date in expiration column for renewal tracking

When managing prepaid insurance in a 10-column worksheet, Tracking Expiration is a critical step to ensure timely renewals and avoid coverage gaps. In the designated "Expiration" column, you must record the exact end date of each insurance policy. This column serves as a centralized reference point for monitoring when policies are set to expire. To implement this, locate the "Expiration" column in your worksheet, typically positioned after columns for policy details like "Policy Number," "Provider," and "Coverage Type." For each prepaid insurance entry, input the policy’s end date in a consistent format, such as MM/DD/YYYY, to maintain clarity and uniformity.

Accuracy is paramount when noting the policy end date in the "Expiration" column. Double-check the insurance documents or policy summaries to ensure the date entered is correct. Mistakes in this column can lead to missed renewals or unnecessary overlaps in coverage. If the policy includes a grace period, consider adding a note in an adjacent column or using conditional formatting to highlight policies expiring within the next 30, 60, or 90 days. This proactive approach helps prioritize renewals and keeps your insurance management organized.

To streamline renewal tracking, sort the worksheet by the "Expiration" column periodically. This allows you to quickly identify policies expiring soon and take action before they lapse. Additionally, consider adding a "Renewal Status" column adjacent to the "Expiration" column to indicate whether a policy is pending renewal, renewed, or canceled. This enhances visibility and ensures no policy slips through the cracks. Regularly updating this column as renewals are processed maintains the worksheet’s accuracy and reliability.

For long-term efficiency, integrate reminders or alerts based on the dates in the "Expiration" column. Many spreadsheet tools, like Excel or Google Sheets, allow you to set up automated notifications or use formulas to flag upcoming expirations. For example, a formula like `=IF(TODAY() > [Expiration Date], "Expired", "Active")` can help categorize policies. Pairing this with color coding or filters further simplifies tracking and ensures you stay ahead of renewals.

Finally, maintain consistency in updating the "Expiration" column whenever new policies are added or existing ones are renewed. If a policy is renewed, update the expiration date to reflect the new term and adjust the prepaid amount in the corresponding columns. Regularly reviewing and updating this column not only keeps your worksheet current but also reinforces a disciplined approach to insurance management. By prioritizing the "Expiration" column, you create a robust system for tracking prepaid insurance and ensuring continuous coverage.

Understanding Excess Group Life Insurance and PA Tax Laws

You may want to see also

Explore related products

![]()

Reconciliation: Verify balances monthly, ensure accuracy in prepaid insurance and expense accounts

Reconciliation is a critical process in accounting to ensure that the balances in prepaid insurance and expense accounts are accurate and up-to-date. When dealing with prepaid insurance in a 10-column worksheet, monthly verification is essential to maintain financial integrity. Begin by reviewing the general ledger for prepaid insurance and related expense accounts. Compare the ending balance of the prepaid insurance account from the previous month to the beginning balance of the current month to ensure continuity. Any discrepancies should be investigated promptly to identify errors or omissions in recording transactions.

To verify the accuracy of prepaid insurance, examine the supporting documentation, such as insurance policies and payment receipts. Ensure that the prepaid insurance amount reflects the unexpired portion of the policy, which is calculated by prorating the total cost over the coverage period. For example, if a $1,200 annual insurance policy was paid in January and it’s now June, the prepaid insurance balance should represent the remaining six months of coverage. Adjusting entries may be necessary if the balance does not align with the unexpired term. Record these adjustments in the appropriate columns of the worksheet, ensuring that the debit or credit entries are correctly allocated to prepaid insurance and insurance expense accounts.

Next, focus on the insurance expense account to ensure it accurately reflects the monthly cost of insurance consumed. The expense should be calculated based on the portion of prepaid insurance allocated to the current period. For instance, if the monthly insurance cost is $100, ensure this amount is consistently expensed each month. Cross-reference the insurance expense account with the income statement to verify that the recorded expenses match the expected monthly allocation. Any variances should be addressed by reviewing the adjusting entries and ensuring they are properly recorded in the worksheet.

In the 10-column worksheet, use the appropriate columns to track the prepaid insurance balance, monthly adjustments, and insurance expenses. The "Balance" column should reflect the beginning and ending balances, while the "Adjustments" column should capture any corrections or allocations made during the month. The "Insurance Expense" column should show the monthly expense recorded. Ensure that the total debits and credits balance across all columns to maintain accuracy. Regularly updating these columns monthly will facilitate a smoother reconciliation process and reduce the risk of errors.

Finally, perform a thorough review of the worksheet at the end of each month to confirm that the prepaid insurance and expense accounts are reconciled. Compare the ending balance of the prepaid insurance account to the total of unexpired insurance coverage, and ensure the insurance expense account aligns with the monthly allocation. If discrepancies arise, trace the transactions back to their source documents to identify and rectify errors. Consistent monthly reconciliation not only ensures accuracy but also provides a clear audit trail, which is vital for financial reporting and compliance. By following these steps, you can effectively manage prepaid insurance in a 10-column worksheet and maintain reliable financial records.

New York Life Insurance: Contact Number and Details

You may want to see also

Frequently asked questions

Prepaid insurance is an asset representing insurance coverage paid in advance. In a 10-column worksheet, it should be recorded in the Debit column under the Prepaid Insurance account to reflect the asset, and the corresponding Credit should be to the Cash account to show the payment.

The Prepaid Insurance account is debited in the Debit column, and the Cash account is credited in the Credit column. Both entries should be recorded in the Journal section of the worksheet.

To adjust prepaid insurance, debit the Insurance Expense account in the Debit column and credit the Prepaid Insurance account in the Credit column. This allocates the expired portion of the prepaid insurance to the current period.

After adjustments, the remaining balance of prepaid insurance should appear in the Balance Sheet section of the worksheet under the Assets column, as it represents the unexpired portion of the insurance coverage.