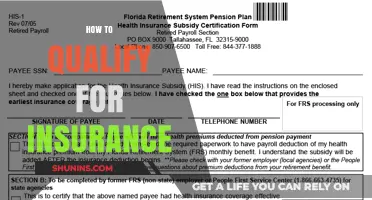

Qualifying for government insurance involves meeting specific eligibility criteria set by federal or state programs, such as Medicaid, Medicare, or the Children’s Health Insurance Program (CHIP). Eligibility is typically based on factors like income, age, disability status, family size, and citizenship or immigration status. For instance, Medicaid serves low-income individuals and families, while Medicare is primarily for those aged 65 and older or individuals with certain disabilities. Applicants must provide documentation to verify their financial situation and personal details, and enrollment often requires completing an application through state health insurance marketplaces or directly through government agencies. Understanding the specific requirements of each program is essential to determine eligibility and access affordable healthcare coverage.

Explore related products

$15.44 $19.75

$28.45 $59.95

What You'll Learn

- Income Eligibility Requirements: Understand income limits and guidelines to qualify for government insurance programs

- Age and Citizenship Criteria: Meet age, residency, and citizenship requirements for specific insurance plans

- Disability and Health Conditions: Qualify based on documented disabilities or chronic health conditions

- Family Size and Dependents: Adjust eligibility based on household size and dependent status

- Application and Documentation: Submit required forms, proof of income, and other necessary documents accurately

![]()

Income Eligibility Requirements: Understand income limits and guidelines to qualify for government insurance programs

To qualify for government insurance programs, understanding the Income Eligibility Requirements is crucial. These programs, such as Medicaid, the Children’s Health Insurance Program (CHIP), and subsidized health plans through the Affordable Care Act (ACA) Marketplace, have specific income limits that determine eligibility. Generally, eligibility is based on the Federal Poverty Level (FPL), which is adjusted annually and varies by household size. For example, Medicaid typically covers individuals and families with incomes up to 138% of the FPL in states that have expanded the program. However, non-expansion states may have stricter income limits, often below 100% of the FPL. It’s essential to check your state’s specific guidelines, as eligibility criteria can differ significantly.

When assessing income limits, all countable income sources are considered, including wages, self-employment income, Social Security benefits, unemployment benefits, and alimony. Some programs may also account for deductions, such as certain work-related expenses or medical costs for the elderly or disabled. For ACA Marketplace subsidies, eligibility is determined by income relative to the FPL, with premium tax credits available for households earning between 100% and 400% of the FPL. Understanding these thresholds is key to determining whether you qualify for free or low-cost coverage through government insurance programs.

Household size plays a pivotal role in income eligibility guidelines. Larger households have higher income limits compared to smaller ones, as the FPL increases with each additional family member. For instance, a single individual may qualify for Medicaid with an income up to $18,000 annually (138% of the FPL), while a family of four may qualify with an income up to $37,000. When applying, ensure you provide accurate information about your household size and income to avoid discrepancies that could affect your eligibility.

It’s also important to note that income eligibility requirements can vary by program and state. For example, CHIP often has higher income limits than Medicaid, allowing families with slightly higher incomes to access affordable coverage for their children. Additionally, some states have implemented their own eligibility rules or waivers, which may expand coverage to individuals who would not qualify under federal guidelines. Researching your state’s specific programs and consulting resources like Healthcare.gov or your state’s Medicaid office can provide clarity on these variations.

Finally, documentation and verification are critical steps in proving your income eligibility. Applicants are typically required to provide recent pay stubs, tax returns, or other proof of income. For self-employed individuals or those with fluctuating income, averaging income over a specific period may be necessary. Keeping detailed records and ensuring all documentation is up-to-date will streamline the application process and increase your chances of approval. By thoroughly understanding and meeting the income eligibility requirements, you can successfully navigate the path to qualifying for government insurance programs.

Does Citizens Insurance Cover Ranch Properties? A Comprehensive Guide

You may want to see also

Explore related products

$43.71 $49

![]()

Age and Citizenship Criteria: Meet age, residency, and citizenship requirements for specific insurance plans

To qualify for government insurance, understanding the age and citizenship criteria is crucial, as these requirements vary depending on the specific insurance plan. For instance, Medicare, a federal health insurance program, primarily serves individuals aged 65 and older. However, younger individuals with certain disabilities or those with End-Stage Renal Disease (ESRD) may also qualify. It’s essential to verify your age eligibility by checking the official Medicare guidelines or consulting a healthcare representative. Additionally, Medicare requires beneficiaries to be either U.S. citizens or permanent legal residents who have lived in the United States for at least five continuous years. Meeting these age and citizenship criteria is the first step in determining your eligibility for this program.

Another government insurance program, Medicaid, has different age and citizenship requirements that vary by state. While Medicaid primarily assists low-income individuals and families, eligibility often includes children, pregnant women, parents, seniors, and individuals with disabilities. Age criteria can range from newborns to seniors, depending on the state’s specific guidelines. Citizenship requirements mandate that applicants must be either U.S. citizens, qualified non-citizens, or legal permanent residents. Some states may also require proof of residency, such as a state-issued ID or utility bills. It’s important to review your state’s Medicaid program details to ensure you meet both the age and citizenship criteria.

For Children’s Health Insurance Program (CHIP), the focus is on providing coverage for children in families who earn too much to qualify for Medicaid but cannot afford private insurance. Age eligibility for CHIP typically covers children up to 19 years old, though this may vary by state. Citizenship requirements are similar to Medicaid, where children must be U.S. citizens or qualified immigrants. Parents or guardians applying for CHIP on behalf of their children must also meet residency requirements, proving they live in the state where they are applying. Understanding these age and citizenship criteria ensures that children receive the necessary healthcare coverage.

Veterans’ healthcare benefits through the Department of Veterans Affairs (VA) have unique age and citizenship criteria. While there is no specific age requirement, eligibility is primarily based on military service history. Applicants must be U.S. citizens or non-citizen veterans who served in the active military and were discharged under conditions other than dishonorable. Residency requirements may also apply, as some benefits are tied to living in specific areas or enrolling in certain programs. Veterans should review their service records and consult the VA to confirm eligibility based on these criteria.

Lastly, Affordable Care Act (ACA) marketplace plans do not have strict age limits, as they are available to individuals of all ages who meet income and citizenship requirements. However, applicants must be U.S. citizens, nationals, or lawfully present immigrants to qualify. Residency requirements include living in a state where the marketplace operates. While age is not a barrier, certain plans may offer specific benefits tailored to different age groups, such as pediatric care for children or preventive services for adults. Ensuring compliance with citizenship and residency criteria is essential when applying for ACA plans. Always verify these details through official government resources or healthcare navigators to avoid disqualification.

Understanding DC Single Life Insurance Plans

You may want to see also

Explore related products

![]()

Disability and Health Conditions: Qualify based on documented disabilities or chronic health conditions

To qualify for government insurance based on disability and health conditions, individuals must provide documented evidence of their disabilities or chronic health conditions. This typically involves submitting medical records, diagnoses, and statements from healthcare providers that confirm the nature and severity of the condition. Government programs like Medicaid and Supplemental Security Income (SSI) often require proof that the disability or health condition significantly impairs daily functioning or is expected to last at least 12 months or result in death. It is essential to ensure that all documentation is up-to-date and clearly outlines how the condition affects your ability to work or perform daily activities.

For Social Security Disability Insurance (SSDI), eligibility is based on having a documented disability that prevents you from engaging in substantial gainful activity (SGA). The Social Security Administration (SSA) maintains a Listing of Impairments, which outlines specific criteria for various physical and mental health conditions. If your condition meets or equals the criteria in the listings, you may qualify for benefits. Even if your condition is not listed, the SSA will assess your residual functional capacity (RFC) to determine if you can perform any work. Working with a healthcare provider to gather comprehensive medical evidence is crucial for a successful application.

Individuals with chronic health conditions such as diabetes, heart disease, or autoimmune disorders may also qualify for government insurance if their condition is severe enough to limit their ability to work. Programs like Medicaid often consider the financial impact of managing chronic conditions, such as ongoing medical expenses, when determining eligibility. Some states have expanded Medicaid to cover individuals with lower incomes who have chronic illnesses, even if they do not meet the traditional disability criteria. It is important to check your state’s specific guidelines for Medicaid eligibility related to chronic health conditions.

In addition to federal programs, some states offer Medicaid waivers or disability-specific programs that provide additional support for individuals with documented disabilities or chronic health conditions. These programs may cover services like home health care, medical equipment, or specialized therapies not typically included in standard insurance plans. To qualify, applicants must meet both medical and financial criteria, which vary by state. Contacting your state’s Medicaid office or Department of Health Services can provide clarity on available programs and application requirements.

Finally, it is important to apply for benefits promptly and follow all instructions carefully. The application process for government insurance based on disability or chronic health conditions can be lengthy and may require appeals if initially denied. Seeking assistance from a disability advocate, attorney, or social worker can help navigate the process and ensure all necessary documentation is submitted correctly. Regularly updating medical records and staying informed about changes to eligibility criteria will also strengthen your application and improve your chances of approval.

Calculating Life Insurance Reserves: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

Family Size and Dependents: Adjust eligibility based on household size and dependent status

When determining eligibility for government insurance, family size and dependent status play a crucial role in the assessment process. The government recognizes that larger households and those with dependents often face higher living expenses, which can impact their ability to afford private insurance. As such, eligibility criteria are adjusted to accommodate these variations. For instance, a family of four with two children will likely have different financial thresholds compared to a single individual. Understanding how family size influences eligibility is essential for applicants to accurately assess their qualification for government insurance programs.

The first step in adjusting eligibility based on family size is to define the household composition. This includes counting all individuals living under the same roof, including spouses, children, and other dependents. Dependents are typically defined as individuals who rely on the primary applicant for financial support, such as minor children, disabled family members, or elderly parents. Each dependent adds to the household size, which in turn affects the income limits and asset thresholds used to determine eligibility. For example, a program might allow a higher income for a family of five compared to a family of two, ensuring that larger families are not unfairly excluded from benefits.

Income limits are a key factor in eligibility, and these limits are often scaled based on family size. Government insurance programs use the Federal Poverty Level (FPL) as a benchmark, with eligibility often set at a certain percentage above this level. For instance, a program might cover families with incomes up to 200% of the FPL. Since the FPL varies depending on household size, a larger family will have a higher income threshold. This means a family of six might qualify with a higher total income than a family of three, even if their per-person income is similar. Applicants should carefully review the income guidelines for their specific family size to ensure accurate eligibility assessment.

In addition to income, some government insurance programs also consider the financial responsibilities associated with dependents. For example, childcare expenses, medical costs for disabled dependents, or educational expenses for children may be factored into the eligibility calculation. These adjustments acknowledge the additional financial burdens that come with supporting dependents. Applicants should be prepared to provide documentation of such expenses, as they can sometimes increase the allowable income limit or reduce the household’s countable income, thereby improving eligibility chances.

Lastly, it’s important to note that eligibility rules can vary significantly between different government insurance programs, such as Medicaid, CHIP (Children’s Health Insurance Program), or subsidized health plans through the Marketplace. Each program may have its own definitions of family size, dependent status, and income calculations. Applicants should research the specific requirements of the program they are interested in and, if necessary, consult with program representatives or enrollment assisters to ensure they accurately account for their family size and dependent status during the application process. This proactive approach will help maximize the chances of qualifying for the appropriate government insurance coverage.

How to Verify Someone's Liability Insurance Coverage: A Step-by-Step Guide

You may want to see also

Explore related products

![Medicare and Social Security: [5 in 1] Maximize Your Retirement Benefits, Secure Medical Coverage and Quality Healthcare | Proven Strategies to Protect Your Financial Future Avoiding Costly Mistakes](https://m.media-amazon.com/images/I/71sRJGiWeQL._AC_UL320_.jpg)

![]()

Application and Documentation: Submit required forms, proof of income, and other necessary documents accurately

To successfully apply for government insurance, it is crucial to gather and submit all required forms and documentation accurately. The application process typically begins with obtaining the necessary forms, which can often be found on the official government insurance website or at local government offices. These forms will require detailed personal information, including your full name, address, Social Security number, and contact details. Ensure that all sections of the forms are completed thoroughly, as incomplete applications may result in delays or denials. Double-check your entries for accuracy, as errors can lead to complications in the review process.

Proof of income is a critical component of the application, as government insurance programs often have income-based eligibility criteria. You will need to provide recent pay stubs, tax returns, or other official documents that verify your income. If you are self-employed, bank statements or profit and loss statements may be required. For those with fluctuating income, such as seasonal workers or freelancers, additional documentation like contracts or client invoices might be necessary. It’s essential to organize these documents chronologically and ensure they cover the required time period specified by the program guidelines.

In addition to income verification, other necessary documents may include proof of citizenship or legal residency, as government insurance programs typically require applicants to be U.S. citizens or qualified immigrants. Acceptable documents often include a birth certificate, passport, or permanent resident card. If you are applying on behalf of dependents, you will also need to provide their documentation, such as birth certificates or adoption papers. For individuals with disabilities or specific medical conditions, additional medical records or statements from healthcare providers may be required to support your application.

Accuracy and completeness are paramount when submitting your application and supporting documents. Any discrepancies or missing information can result in your application being returned or denied. Before submission, create a checklist of all required documents and review each item to ensure it is included and correctly filled out. If you are unsure about any part of the application, contact the relevant government office or a caseworker for guidance. Many programs also offer online tools or helplines to assist applicants in navigating the process.

Finally, keep copies of all submitted documents for your records. This not only helps in case of follow-up questions or audits but also ensures you have a reference for future applications or updates. Submit your application through the designated channels, whether online, by mail, or in person, and retain proof of submission, such as a confirmation number or receipt. By carefully preparing and submitting your application and documentation, you increase your chances of qualifying for government insurance and accessing the benefits you need.

Understanding PMI Insurance: Do You Have It and How It Works

You may want to see also

Frequently asked questions

Eligibility for government insurance, such as Medicaid or Medicare, varies by program. Generally, factors like income, age, disability status, family size, and citizenship or residency status are considered. For example, Medicaid is income-based, while Medicare is primarily for individuals aged 65 and older or those with certain disabilities.

You can apply for government insurance through your state’s health insurance marketplace, the Healthcare.gov website, or directly through your state’s Medicaid office. Required documents typically include proof of income (e.g., pay stubs or tax returns), identification (e.g., driver’s license or passport), and proof of citizenship or legal residency.

Yes, you may still qualify for government insurance, such as Medicaid, if your income meets the eligibility criteria, even if you have private insurance. However, Medicare typically serves as the primary insurer for those eligible, with private insurance acting as secondary coverage. Check specific program rules to understand how coverage works in your situation.

![The Medicare Bible for Beginners: [3 in 1] Unlock Medical Benefits and Quality Healthcare | Super Easy Insider Strategies to Navigate Medicare While Avoiding Costly Mistakes](https://m.media-amazon.com/images/I/71tm-tSiWnL._AC_UL320_.jpg)