Understanding how to read health insurance documents is crucial for making informed decisions about your healthcare coverage. Health insurance policies can be complex, filled with specific terminology and details that impact your benefits and financial responsibilities. This guide aims to demystify the process by breaking down the key components of health insurance documents, such as the summary of benefits, provider networks, and coverage limitations. By learning how to navigate these documents effectively, you can ensure that you are getting the most out of your health insurance plan and avoiding unexpected costs.

| Characteristics | Values |

|---|---|

| Document Type | Informational guide |

| Purpose | To educate readers on understanding and navigating health insurance |

| Target Audience | Individuals seeking to understand health insurance, possibly including new enrollees, students, or employees |

| Language | English |

| Format | Digital or printable document, possibly a PDF |

| Length | Approximately 10-20 pages |

| Content Sections | Introduction to health insurance, Glossary of terms, Explanation of benefits, How to read an Explanation of Benefits (EOB), Common health insurance forms, Tips for managing health insurance, Frequently Asked Questions (FAQs) |

| Visual Elements | Diagrams illustrating insurance concepts, Infographics summarizing key points, Example forms with annotations |

| Tone | Clear, concise, and informative |

| Style | Professional and user-friendly |

| Authoritative Source | Health insurance company, Government health agency, or Healthcare advocacy group |

| Date of Publication | Recent, ideally within the last year |

| Accessibility Features | Readable font size, High contrast colors, Alt text for images |

| Call to Action | Contact information for further assistance, Links to additional resources |

| Reviews/Ratings | Positive feedback from readers, High ratings on educational value |

| Updates | Regularly updated to reflect changes in health insurance policies and regulations |

Explore related products

$97.95

$80.99 $257.95

What You'll Learn

- Understanding Policy Documents: Learn to navigate and comprehend the various sections of your health insurance policy

- Key Terms and Definitions: Familiarize yourself with essential health insurance terminology to better grasp your coverage details

- Coverage and Exclusions: Discover what medical services are covered and which ones are excluded under your specific plan

- Claims and Appeals: Understand the process of filing claims and how to appeal decisions if your claim is denied

- Comparing Plans and Costs: Evaluate different health insurance plans and their costs to make an informed decision

![]()

Understanding Policy Documents: Learn to navigate and comprehend the various sections of your health insurance policy

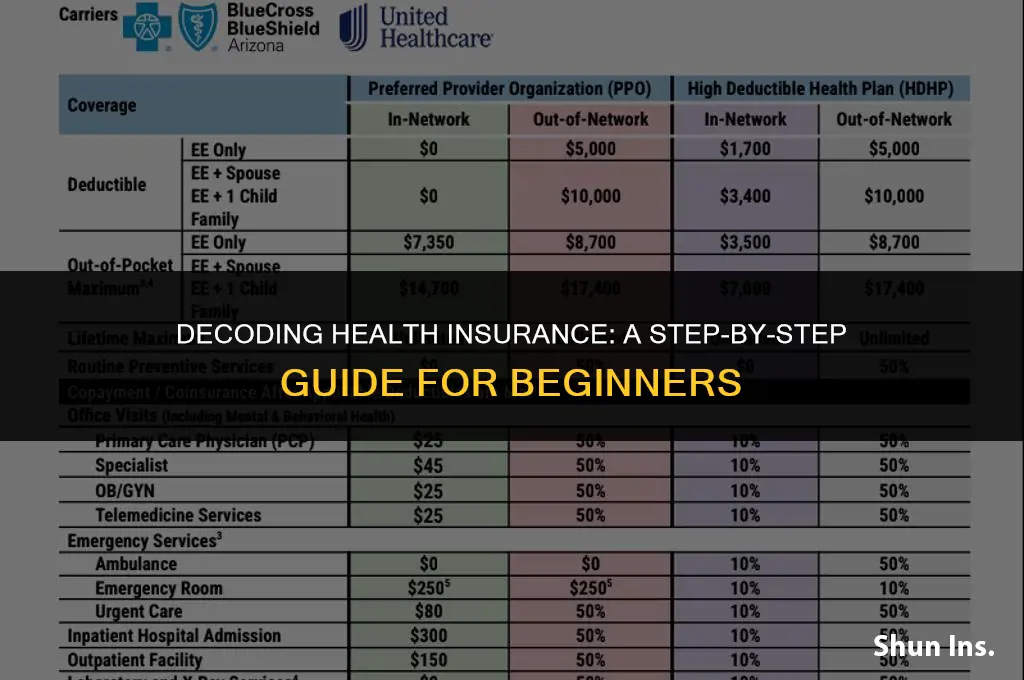

Policy documents are often dense and filled with jargon, making them challenging to decipher. However, understanding these documents is crucial to ensure you're fully aware of your health insurance coverage. Start by familiarizing yourself with the layout and sections typically found in such documents.

The first section to review is the 'Summary of Benefits and Coverage' (SBC). This section provides a concise overview of what your plan covers and what you're responsible for paying. It's an excellent starting point to grasp the essentials of your policy.

Next, delve into the 'Exclusions and Limitations' section. Here, you'll find details about what services and treatments are not covered under your plan. This is vital information to avoid unexpected out-of-pocket expenses.

The 'Glossary' is another critical component. It defines the terms and conditions used throughout the document, helping you understand the language and context of your policy.

Finally, pay close attention to the 'Claims and Appeals' section. This outlines the process for submitting claims and how to appeal decisions if you're denied coverage for a service you believe should be covered.

By methodically reviewing these sections, you can gain a comprehensive understanding of your health insurance policy and make informed decisions about your healthcare.

Securing Universal Coverage: Strategies to Prevent Health Insurance Denials

You may want to see also

Explore related products

$53.03 $257.95

![]()

Key Terms and Definitions: Familiarize yourself with essential health insurance terminology to better grasp your coverage details

Understanding health insurance can feel like navigating a maze of jargon and complex terms. To help you decipher your coverage details, it's essential to familiarize yourself with some key terminology. This knowledge will empower you to make informed decisions about your healthcare and ensure you're getting the most out of your insurance plan.

One crucial term to understand is "deductible." This is the amount you must pay out of pocket for healthcare services before your insurance coverage kicks in. For example, if your deductible is $1,000, you'll need to pay the first $1,000 of your medical bills each year before your insurance starts to cover the costs. Knowing your deductible can help you plan for healthcare expenses and avoid unexpected financial burdens.

Another important term is "co-pay" or "copayment." This is a fixed amount you pay for each healthcare service or prescription medication, even after you've met your deductible. Co-pays can vary depending on the type of service or medication, so it's important to review your plan's details to understand your out-of-pocket costs.

"Premium" is the monthly or annual fee you pay for your health insurance coverage. This cost can vary widely depending on factors such as your age, health status, and the level of coverage you choose. Understanding your premium and how it fits into your overall budget is crucial for maintaining your insurance coverage.

Finally, "out-of-pocket maximum" is a term that can provide significant financial protection. This is the most you'll have to pay for healthcare services in a given year, after which your insurance will cover 100% of the costs. Knowing your out-of-pocket maximum can give you peace of mind and help you plan for potential healthcare expenses.

By familiarizing yourself with these key terms and definitions, you'll be better equipped to understand your health insurance coverage and make informed decisions about your healthcare. Remember to review your plan's details regularly and reach out to your insurance provider with any questions or concerns you may have.

Health Insurance Elections: Do They Automatically Carry Over if Unspecified?

You may want to see also

Explore related products

$227.64 $257.95

![]()

Coverage and Exclusions: Discover what medical services are covered and which ones are excluded under your specific plan

Understanding the intricacies of health insurance coverage is crucial for making informed decisions about your healthcare. One key aspect to consider is the balance between coverage and exclusions. This section will delve into the specifics of what medical services are typically covered and which ones may be excluded under a standard health insurance plan.

Coverage under a health insurance plan generally includes a wide range of medical services such as doctor visits, hospital stays, emergency room care, prescription medications, and preventive care services like vaccinations and screenings. However, it's important to note that not all services are covered equally. For instance, while preventive care is often fully covered, other services may require a copay or coinsurance.

Exclusions, on the other hand, refer to medical services that are not covered by your insurance plan. These can vary widely depending on the specific policy but may include cosmetic procedures, alternative therapies, experimental treatments, and certain prescription medications. It's also common for insurance plans to exclude coverage for pre-existing conditions, at least for a certain period after you enroll in the plan.

To navigate these complexities, it's essential to carefully review your plan's Summary of Benefits and Coverage (SBC). This document provides a detailed breakdown of what is and isn't covered under your plan, including any limitations or exclusions. Additionally, you can reach out to your insurance provider's customer service for clarification on specific services or treatments.

In conclusion, understanding the coverage and exclusions of your health insurance plan is a critical step in managing your healthcare effectively. By familiarizing yourself with the specifics of your plan, you can avoid unexpected costs and ensure that you're getting the most out of your insurance coverage.

Insurance Companies Using Colossus: A Comprehensive List and Overview

You may want to see also

Explore related products

![]()

Claims and Appeals: Understand the process of filing claims and how to appeal decisions if your claim is denied

Navigating the claims and appeals process in health insurance can be complex, but understanding the steps involved can significantly increase your chances of a successful outcome. When a claim is denied, it's essential to know how to appeal the decision effectively. The first step is to carefully review the Explanation of Benefits (EOB) provided by your insurer to understand the reason for the denial. Common reasons include lack of medical necessity, pre-existing conditions, or errors in billing.

Once you've identified the reason for denial, gather all relevant documentation to support your appeal. This may include medical records, letters from your healthcare provider, and any other evidence that substantiates your claim. It's crucial to act quickly, as most insurers have strict deadlines for filing appeals, typically within 30 to 60 days of the initial denial.

The appeals process usually involves submitting a written request to your insurer, outlining the reasons why you believe the claim should be approved. Be sure to include all supporting documentation and a clear, concise explanation of why the initial decision was incorrect. Some insurers may also allow you to submit additional information or attend a hearing to present your case in person.

If your appeal is unsuccessful, you may have the option to escalate the matter to an independent review organization (IRO) or file a complaint with your state's insurance department. An IRO is a third-party entity that reviews denied claims and provides a binding decision. This process can be lengthy and may require additional documentation and fees, but it can be a valuable option if you believe your claim has been unfairly denied.

Throughout the claims and appeals process, it's important to keep detailed records of all communications with your insurer, including dates, times, and the names of representatives you speak with. This information can be crucial if you need to escalate your case or file a complaint. Additionally, consider seeking assistance from a patient advocate or a healthcare attorney who specializes in insurance claims to help guide you through the process and ensure your rights are protected.

In conclusion, while the claims and appeals process can be challenging, being prepared and knowledgeable about your rights and the steps involved can help you navigate the system more effectively. Remember to stay organized, act promptly, and seek professional assistance when needed to increase your chances of a successful appeal.

Musicians' Health: Getting Medical Insurance as a Band

You may want to see also

Explore related products

![]()

Comparing Plans and Costs: Evaluate different health insurance plans and their costs to make an informed decision

Evaluating different health insurance plans and their costs is crucial to making an informed decision that suits your needs and budget. Start by gathering information on various plans available in your area, which can be done through online research, contacting insurance providers directly, or using a health insurance marketplace.

Once you have a list of potential plans, compare their premiums, deductibles, copayments, and coinsurance rates. Consider your expected healthcare needs and budget when assessing these costs. For example, if you anticipate frequent doctor visits, a plan with a lower copayment may be more cost-effective, whereas if you are generally healthy, a plan with a lower premium might be preferable.

In addition to cost, evaluate the coverage provided by each plan. Look at the types of services covered, such as preventive care, prescription drugs, and mental health services. Check for any exclusions or limitations, and consider how these might impact your healthcare needs. For instance, if you have a chronic condition, ensure that the plan covers the necessary treatments and medications.

Another important factor to consider is the provider network. Check which doctors and hospitals are in-network for each plan, and verify that your preferred healthcare providers are included. If you have specific healthcare needs, such as ongoing treatment for a medical condition, it is essential to ensure that your current providers are part of the plan's network.

Finally, consider the plan's customer service and reputation. Look for reviews and ratings from current and past policyholders to get an idea of the plan's performance and customer satisfaction. Evaluate the plan's claims process, appeals process, and overall customer support to ensure that you will have a positive experience if you need to use your insurance.

By carefully comparing plans and costs, and considering factors such as coverage, provider network, and customer service, you can make an informed decision that will provide you with the best possible health insurance coverage for your needs and budget.

Disney Kitchen Staff Health Insurance: Benefits and Coverage Explained

You may want to see also

Frequently asked questions

When reading your health insurance policy, it's essential to look for key details such as coverage limits, deductibles, copayments, coinsurance, excluded services, and the list of in-network providers. Understanding these terms will help you know what is covered and what you are responsible for financially.

To determine if a medical service is covered by your health insurance, you should review the policy's coverage section, which outlines the types of services and treatments that are included. Additionally, you can contact your insurance provider directly to ask about specific services and verify if they are covered under your plan.

If you disagree with a decision made by your health insurance provider, you should first review your policy to ensure you understand the coverage and any limitations. Then, you can contact your provider to discuss the issue and ask for an explanation of their decision. If you are still not satisfied, you may be able to file an appeal or grievance with your state's insurance department or an independent review organization.