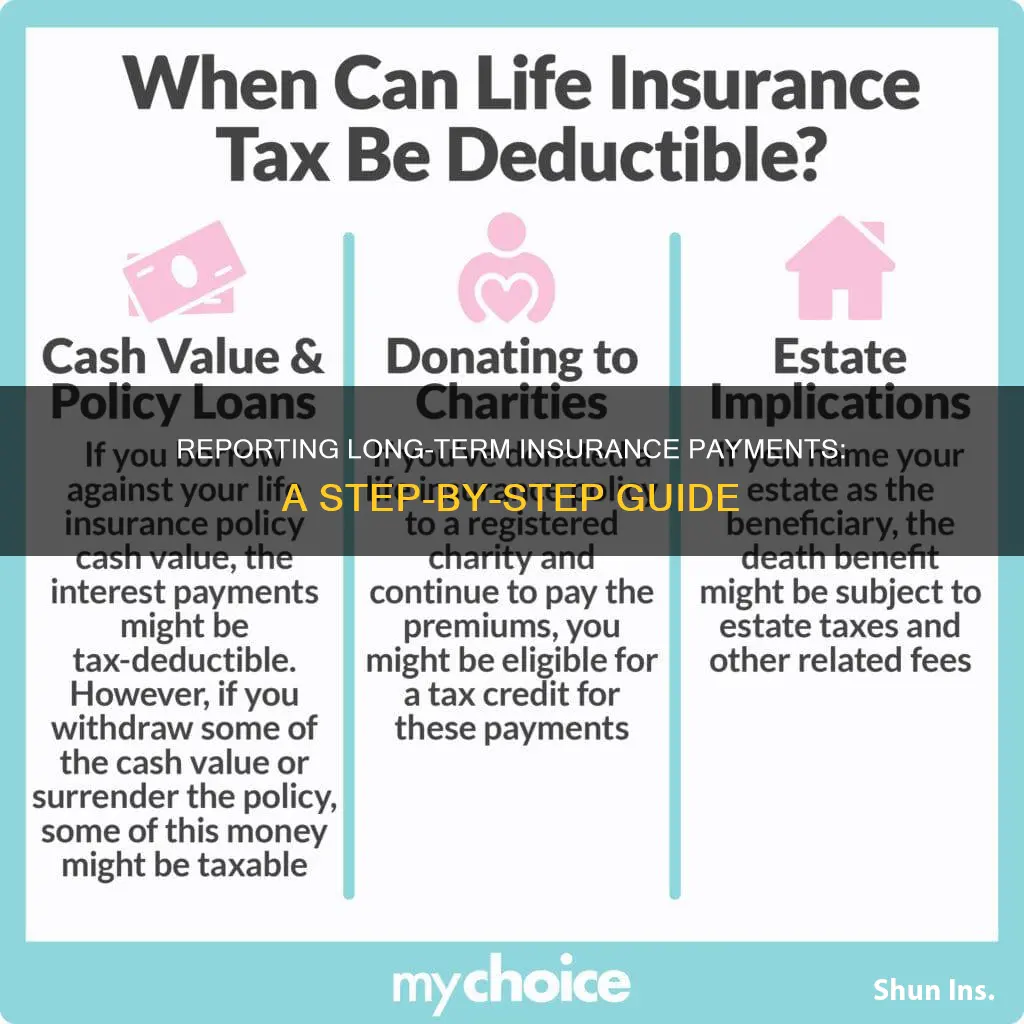

Long-term care insurance provides financial support for individuals who require assistance with daily activities due to physical or cognitive impairments. When filing a claim, it is essential to understand the policy's terms and conditions, including any waiting periods, to ensure timely and accurate reimbursement. To initiate the process, locate the policy or payment records, and contact the insurance company to verify coverage details and specific requirements, such as a nursing assessment or Plan of Care. Additionally, tax implications related to long-term care insurance benefits should be considered. While tax-qualified benefits are typically tax-free, non-tax-qualified policies may result in tax liabilities. The IRS requires insurance companies to provide claimants with a 1099-LTC form to report payments, which may raise questions about tax obligations. Consulting a tax advisor is advisable to navigate these complexities and ensure compliance with reporting requirements.

| Characteristics | Values |

|---|---|

| Reporting long-term insurance payments | Insurance companies that pay long-term care insurance benefits are required by the IRS to provide claimants with a 1099 LTC form |

| The 1099 LTC form is used to report payments made under a long-term care insurance contract | |

| Insurance companies usually issue these 1099 LTC forms in January for the prior tax year | |

| The 1099 LTC form reflects payments made directly to the claimant as well as those made to third parties on their behalf | |

| Tax-qualified long-term care insurance benefits are tax-free | |

| If the amounts are taxable, you can submit a Form W-4S, Request for Federal Income Tax Withholding From Sick Pay, to the insurance company | |

| You can make estimated tax payments by filing Form 1040-ES, Estimated Tax for Individuals | |

| You can generally exclude from income payments received from qualified long-term care insurance contracts as reimbursement of medical expenses received for personal injury or sickness under an accident and health insurance contract | |

| To file a claim, locate the policy or any records of premium payments | |

| Call the agent or insurance company listed on the documents to see if the policy is still in force | |

| If the policy is in force, find out all the specifics of the coverage, including how to trigger the policy and start receiving benefits | |

| Typically, to start receiving benefits, the policyholder must need help with at least two activities of daily living or help due to a cognitive impairment | |

| Once you have a physical or cognitive trigger, your need for care must be expected to last more than 90 days and a Plan of Care must be established | |

| After you've fulfilled your Elimination Period (waiting period), you'll start to receive benefits | |

| The policyholder (or their legal representative/agent under power of attorney) must sign the claimant's statement form | |

| This form is completed by the policyholder's primary care physician (or the doctor at their long-term care facility) and verifies that the care they require is medically necessary | |

| Grace period | The premium payment grace period is usually 3 months |

Explore related products

What You'll Learn

![]()

Understanding tax-qualified long-term insurance benefits

Long-term care insurance offers a range of tax benefits that can help individuals and businesses manage future care costs. These benefits can be understood by looking at the tax treatment of qualified long-term care insurance contracts, the tax-deductible nature of certain premiums, and the tax-free status of insurance benefits in certain cases.

Tax Treatment of Qualified Long-Term Care Insurance Contracts

The Health Insurance Portability and Accountability Act of 1996 (HIPAA) included provisions for favourable tax treatment of qualified Long-Term Care Insurance (LTCi) contracts. These tax-qualified LTCi premiums are considered medical expenses, which can be tax-deductible for individuals who itemize their deductions. The deductible amount is limited to eligible LTCi premiums, as defined by Internal Revenue Code 213(d), and is based on the age of the insured. For individuals over 70, up to $5,880 in long-term care premiums can be deducted for the 2024 tax year.

Tax-Deductible Premiums

Long-term care insurance premiums paid for qualified policies are often tax-deductible. The deductible amount depends on the taxpayer's age and adjusted gross income (AGI). To be considered a qualified expense, total medical expenses, including long-term care premiums, must exceed 7.5% of the taxpayer's AGI. For businesses, employer-paid premiums may also be tax-deductible as a business expense.

Tax-Free Insurance Benefits

Benefits received from a long-term care policy are generally not subject to federal income tax, provided they don't exceed certain limits. If the policy is a tax-qualified contract and only pays benefits that reimburse for qualified long-term care expenses, the benefits are typically tax-free. However, for non-tax-qualified contracts, some or all of the benefits may be taxable.

Overall, understanding the tax-qualified nature of long-term care insurance benefits is essential for individuals and businesses looking to maximize their tax advantages and effectively plan for future care costs.

Stolen Reports: Insurance Claims and Acceptance

You may want to see also

Explore related products

![]()

Locating your long-term insurance policy

Locating a long-term insurance policy can be challenging, especially when dealing with the loss of a loved one. Here are some steps to help you locate a missing long-term insurance policy:

First, determine if the policy belongs to you or a loved one. If it is your own policy, start by checking your bank account and credit card statements for evidence of payments to an insurer. Old policy documents and bank statements may also provide information about your insurance provider. Most providers include their contact details on their communications and websites, so you can reach out to them directly.

If you cannot contact the insurer, it could be that the company has changed its name. In this case, online tools and resources can be useful. The UK's Association of British Insurers (ABI) provides a "Keeping Track of your Pension" page to help locate missing life insurance policies.

If you are trying to locate a deceased loved one's policy, you must be an authorized legal representative or a named beneficiary to access the information. Start by looking through the deceased's personal belongings, papers, files, and safe deposit boxes. Check their bank statements for premium payments or indications of a whole life policy, such as funds transferred from an insurance company.

People close to the deceased may have information about the policy, including its storage location, beneficiaries, or the name of the insurance company. Accountants, attorneys, or financial professionals may also be able to provide the necessary information.

To locate a life insurance policy, you can utilize the National Association of Insurance Commissioners' (NAIC) Life Insurance Policy Locator, a free online tool. This tool helps consumers find their loved ones' lost life insurance policies and annuity contracts. To use this tool, go to naic.org, hover over "Consumer," and click on the "Life Insurance Policy Locator" under "Tools." You will need to create an account and provide the necessary details, including the deceased's information from the death certificate.

Additionally, the MIB Group and the National Association of Unclaimed Property Administrators also provide life insurance policy location services. Remember, privacy laws strictly regulate life insurance, and only specific individuals, such as next of kin, estate executors, and policy beneficiaries, are typically granted access to policy information.

If you are searching for a workplace pension with a previous employer, you can contact them directly or use the government's free Pension Tracing Service to obtain the scheme or provider's details.

Insurance Brokerage House: What's the Deal?

You may want to see also

Explore related products

![]()

Filling out the 1099 LTC form

If you have received a 1099-LTC tax form, it is likely because you received long-term care benefits or accelerated death benefits. This form is used by individual taxpayers to report long-term care benefits to the Internal Revenue Service (IRS). It is important to note that not all the amounts reported on Form 1099-LTC are automatically taxable. Whether or not you need to report it on your tax return depends on the following factors:

- Was the payment for long-term care? If yes, you might not owe taxes on it, especially if the payments were for qualified LTC services and didn't exceed the actual costs of care. For per diem benefits, you can exclude a certain amount from your income each day. However, if you exceed this daily limit, you may have to pay taxes on the excess amount.

- Was the payment for accelerated death benefits?

The 1099-LTC form will include the following information:

- Box 1: Gross long-term care benefits or gross benefits paid by the insurance company. This is the total amount you received from your LTC insurance contract.

- Box 2: Accelerated death benefits. If you received an early payout of life insurance due to a terminal illness, the gross amount will be listed here. This box does not apply to long-term care insurance.

- Box 3: Per diem vs. Reimbursed amount. These checked boxes indicate whether the benefit payout was based on actual costs incurred or made on a per diem basis. This box may also contain the Total Number of Days paid if the policy is an Indemnity (per diem paid) policy.

- Box 4: This is an optional field that indicates if benefits were paid from a Tax Qualified long-term care insurance contract.

- Box 5: The Chronically Ill box will always be checked for LTC. The Terminally Ill box is not applicable to long-term care.

- Payer's name and address: The name and address of the insurance company or other institution that provided the benefits.

- OMB No.: The tax year for which amounts are reported.

- Payer's Federal Identification Number: The federal tax identification number for the insurance company or institution that paid the benefit amounts.

- Insured's taxpayer identification number (TIN), Social Security Number (SSN), adoption taxpayer identification number, or employer identification number (EIN).

- Account number, gross benefits paid under an LTC contract, and gross accelerated death benefits during the year, if these amounts were paid per diem or as reimbursement of actual long-term care expenses.

- Date Certified: If the policy uses a Reimbursement formula, this box will show the date certified as Chronically Ill. If the policy uses a Per Diem (indemnity) formula, it will show the claim's original date of loss.

- Additional information: The 1099-LTC may also include the total number of days paid and other details related to the payment, such as contact information for the payer and policyholder.

Farmers Insurance: Navigating Florida's Unique Insurance Landscape

You may want to see also

Explore related products

![]()

Consulting a tax advisor

Understanding Tax Implications

Tax advisors are experts in tax laws and regulations. When it comes to long-term insurance payments, there can be complex tax implications, and a tax advisor can help you navigate them. They can explain whether your long-term insurance benefits are tax-exempt or taxable, and guide you through the relevant criteria. This is especially important if you have a non-tax-qualified contract, as there may be potential tax liabilities.

Completing Necessary Forms

Reporting long-term insurance payments often involves completing specific forms, such as the 1099 LTC form. A tax advisor can assist you in correctly filling out these forms and ensuring you provide all the necessary information. They can explain the meaning of each box on the form, such as gross benefits, per diem payments, reimbursement amounts, and tax-qualified status. This ensures your reporting is accurate and compliant with IRS requirements.

Claiming Exemptions and Deductions

Tax advisors are well-versed in identifying opportunities for tax exemptions and deductions. They can advise you on which expenses can be excluded from taxable income, such as qualified long-term care expenses or medical expenses related to personal injury or sickness. By claiming these exemptions, you can reduce your overall tax burden.

Compliance with Regulations

Individualised Guidance

Tax advisors provide personalised guidance based on your unique circumstances. They can review your long-term insurance policy, assess your specific situation, and offer tailored advice. This includes helping you understand the fine print of your policy, such as coverage triggers, waiting periods, and reimbursement processes. By seeking individualised guidance, you can make more informed decisions regarding your long-term insurance payments and their tax implications.

Farmers Insurance and Accident Binders: Understanding the Process

You may want to see also

Explore related products

![[OLD VERSION] TurboTax Home & Business 2024 Tax Software, Federal & State Tax Return [PC/MAC Download]](https://m.media-amazon.com/images/I/71b5aAzdXOL._AC_UY218_.jpg)

![]()

Understanding the claims process

The first step in understanding the claims process is to locate your long-term care insurance policy. If you are unsure where to find it, check bank accounts for past premium payments and mail for a bill or letter from an insurance company. Note down when the premiums are due and how they are paid. Once you have this information, you can request a copy of the policy from the insurance company. This contract will outline what is covered and to what extent, as well as when a claim can be filed and for what services.

It is important to understand the specifics of your policy, as not all services are covered, and some policies have limitations on where care can be received. Most policies have strict guidelines for when benefits begin, and there may be an elimination period during which you must cover the costs yourself before the insurance company will start paying. Review your policy thoroughly to ensure you are meeting the requirements and that the services being used are eligible for coverage. Keep all relevant documents, such as care plans, receipts, and medical records organized and easily accessible to prevent delays.

Once you have determined that you are eligible for long-term care benefits, notify the insurance company through the insurance agent or by contacting the insurer's claims department directly. The insurer will provide a claim form that needs to be completed, and they may also assign a case manager to guide you through the process and answer any questions. When contacting the insurer, be ready with key information, including personal details, policy information, and details of the claim.

After a disaster, you will want to get back to normal as soon as possible, and your insurance company wants that too. In most instances, an adjuster will inspect the damage and offer you a sum of money for repairs, based on the terms and limits of your policy. The first check you get from your insurance company is often an advance against the total settlement amount, not the final payment. If you are offered an on-the-spot settlement, you can accept the check right away, but if you find other damage later, you can reopen the claim and file for an additional amount.

Indiana Farmers Insurance: Understanding the Reach and Service Network

You may want to see also

Frequently asked questions

First, locate the policy or any records of premium payments. Then, call the agent or insurance company to see if the policy is still in force. If it is, find out the specifics of their coverage, including how you trigger the policy and start receiving benefits. Typically, to start receiving benefits, the policyholder must need help with at least two activities of daily living or help due to a cognitive impairment.

Insurance companies that pay long-term care insurance benefits are required by the Internal Revenue Service (IRS) to provide claimants with a 1099 LTC form. This form is used to report the payments made under a long-term care insurance contract. Insurance companies usually issue these 1099 LTC Forms in January for the prior tax year.

Tax-qualified Long-Term Care Insurance benefits are generally tax-free. However, if you have a Non-Tax Qualified Contract, then some or all of your benefits may be taxable, and you should consult a tax advisor.