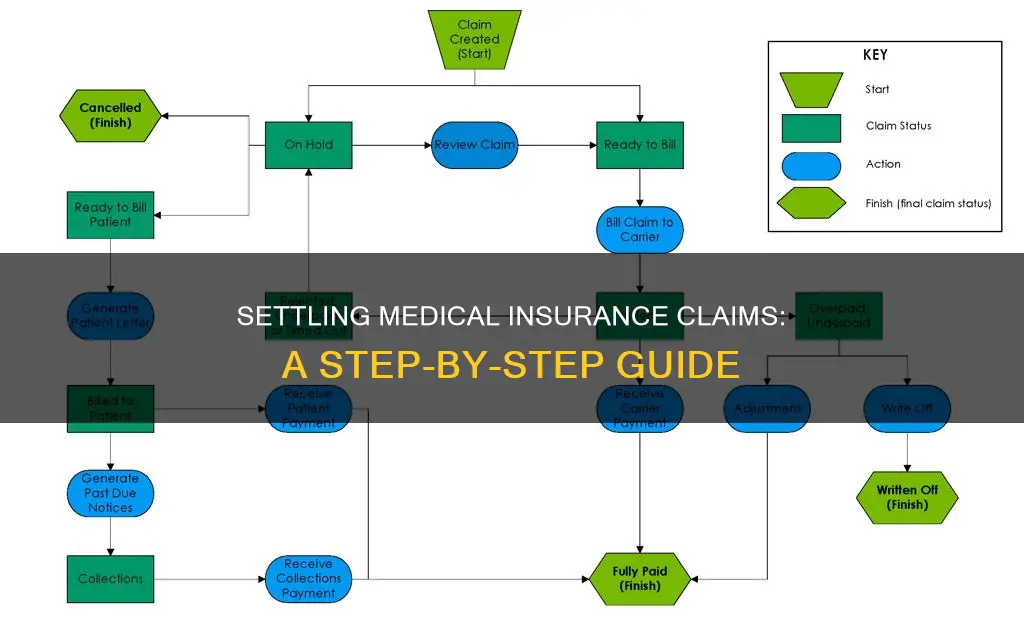

Settling a medical insurance claim can be a long and laborious process, requiring extensive paperwork and a lot of back and forth. The first step is to submit a demand letter to the responsible party's insurance company, detailing how the accident happened, how the defendant is responsible, the extent of your injuries and damages, and how you have suffered. Evidence is key to proving your case and winning your claim. The insurance adjuster will try to refute your claims, so it's important to respond with well-informed facts and to stay patient during the negotiation process. If you can't reach a settlement, you may have to take your claim to court.

How to Settle a Medical Insurance Claim

| Characteristics | Values |

|---|---|

| Evidence | Evidence is required to prove the liability of the policyholder for your injuries. |

| Demand Letter | A demand letter should be submitted to the responsible party's insurance company, including details of the accident, the extent of injuries, and damages. |

| Negotiation | Negotiation is key; remain patient and respond with facts to counter the insurance adjuster's attempts to refute claims. |

| Settlement | A settlement is reached when both parties agree on a fair amount. |

| Court | If a settlement cannot be reached, the claim may have to go to court, either small claims or civil court, depending on the damages. |

| Reimbursement | Reimbursement claims require the claimant to pay upfront and collect documents to submit for reimbursement. |

| Cashless Treatment | Some health insurance policies allow for cashless treatment at network hospitals, where the insurance company settles the bill directly with the hospital. |

| Time | The time taken to settle a health claim can vary from 6 months to 3 years; shorter wait times lead to better medical outcomes. |

| Paperwork | Paperwork is a significant component of the claim process, with medical records, police reports, and other documents required. |

Explore related products

What You'll Learn

![]()

Cashless and reimbursement claims

A cashless claim is a hassle-free facility provided by insurance companies that allows policyholders to receive medical treatment without paying upfront. The insurance company settles the bill directly with the hospital, per the policy terms and conditions. This option is available when the policyholder chooses to be treated at a network hospital. The policyholder will need to inform the insurer at least 72 hours before planned hospitalisation for a cashless claim.

A reimbursement claim, on the other hand, offers more flexibility in choosing the hospital. The policyholder pays the medical expenses upfront and later seeks reimbursement from the insurance company. This can be a time-consuming and complex process, as the policyholder must submit the required documents within 15 days of discharge from the hospital. The reimbursement claim process can take up to 45 days, depending on the specific request and health expenses.

Ultimately, the choice between cashless and reimbursement claims depends on individual preferences and specific policy terms and conditions. It is important to carefully evaluate both options to ensure you have the right health insurance coverage.

Understanding Medical Billing: Insurance Collection Timeframes

You may want to see also

Explore related products

![]()

Negotiating with insurance adjusters

Before negotiating, make sure you have gathered all the necessary evidence to support your claim. This includes medical records, prescriptions, diagnostic test results, bills, and any other relevant documentation. It is also essential to know the full extent of your injuries and the corresponding costs before initiating negotiations. Filing a claim too early, before your body has reached maximum medical improvement, may result in potential expenses being overlooked. On the other hand, be mindful of the statute of limitations in your state, as there are time limits for filing personal injury cases.

When negotiating, remain patient and stand your ground. Insurance adjusters may try to take advantage of your impatience by offering a lower settlement than what is reasonable. Respond to their arguments with well-informed facts and figures that justify the level of compensation you are requesting. Remember, the goal is to reach a fair settlement for both parties, so be prepared to make counteroffers and remain open to compromise.

If negotiations with the insurance adjuster reach an impasse, you may need to pursue other options. Depending on the amount of damages, you could take your claim to small claims court or civil court. In small claims court, you are not required to have legal representation, but you may choose to do so. For higher compensation amounts, it is highly advisable to hire a personal injury attorney to represent you in civil court. Settling out of court is generally less stressful and more efficient, so keep that in mind as you navigate the negotiation process.

Baylor Medical Center: Humana Insurance Acceptance and Your Healthcare

You may want to see also

Explore related products

![]()

Evidence and liability

In the case of personal injury, if someone injures you through negligence or misconduct, they are liable for your damages, and the liable party's insurance company must compensate you. Evidence is crucial to proving liability. You will need to show that the policyholder is responsible for your injuries. This could include medical records, a police report, or other documents. For example, if you are claiming for a broken toe, you will need to show that your toe was fine before the incident.

If you are making a claim against a medical professional for malpractice, you will need to prove that their actions caused you harm. This could include medical records, expert opinions, or other evidence. The medical professional's insurance company will likely take a central role in investigating and settling the claim.

It is important to be aware that your health insurance company may have a right to take part of your injury settlement to recover what they paid for your medical care. This is called subrogation and is intended to prevent your medical bills from being paid twice. Hospitals may also try to claim part of your settlement to cover what you owe them.

To protect your settlement, it is advisable to speak to a personal injury lawyer, who can guide you through the relevant insurance coverage laws in your state. It is also important to be patient during the negotiation process and not to settle for less than what is reasonable. If you cannot reach a settlement, you may have to take your claim to court.

Medical Insurance: A Necessary Evil or a Smart Choice?

You may want to see also

Explore related products

![]()

Claim settlement times

Evidence and Record Review:

The time it takes to gather and review all the necessary medical records, evidence, and supporting documents can impact settlement times. This process typically takes around 30 days but can be longer for more complex cases. It is important to provide comprehensive documentation, including medical practitioner prescriptions, hospitalization records, diagnostic test results, original bills, and receipts, to support your claim.

Negotiation and Counteroffers:

After submitting your claim, the insurance adjuster will investigate and negotiate with you. This back-and-forth negotiation process, which includes offers and counteroffers, can influence settlement times. It is important to remain patient and well-informed during this stage, as insurers may try to refute your claims or offer lower settlements.

Statute of Limitations:

Each state has its own statute of limitations for filing personal injury claims. For example, in Texas, personal injury cases must be filed within two years from the date of the accident. Failing to file within this timeframe may result in the loss of compensation. Therefore, it is crucial to be mindful of the applicable statute of limitations in your state.

Court Proceedings:

If negotiations with the insurance adjuster are unsuccessful, you may have to take your claim to court. This can extend the settlement time, as court proceedings can be lengthy. Depending on the amount of damages, you may pursue small claims court or civil court, with the latter typically requiring legal representation.

Type of Claim:

The type of health insurance claim can also impact settlement times. For example, research shows that personal injury claims in the United States can take anywhere between 6 months to 3 years to settle, while workers' compensation settlements typically take between 6 months to 2 years.

It is important to remember that while you want to ensure you receive a fair settlement, shorter wait times between the initial injury and insurance settlement are associated with better medical outcomes. Therefore, staying organized, providing comprehensive documentation, and actively engaging in the negotiation process can help expedite the settlement process.

Occupational Therapy: Is Medical Insurance Enough?

You may want to see also

Explore related products

![]()

Appealing a rejected claim

If your health insurance claim is rejected, you have the right to appeal the company's decision and have it reviewed by a third party. You can ask your insurance company to reconsider its decision, and they are required to explain why they denied your claim and inform you of how to dispute their decisions. There are two ways to appeal a health plan decision:

Internal Appeal

If your claim is denied or your health insurance coverage is canceled, you have the right to an internal appeal. You can request that your insurance company conduct a full and fair review of its decision. If your case is urgent, the insurance company must expedite this process.

External Review

You can also take your appeal to an independent third party for review, which is known as an external review. In this case, the insurance company loses its authority to make the final decision on whether to pay your claim.

Negotiating with the Insurance Adjuster

The insurance adjuster will try to refute your claims of liability and damages, referencing your medical records or police report. It is important to remain patient and respond with well-informed facts that support your claim for compensation. The negotiation process may involve several offers and counteroffers before a fair settlement is reached.

Taking Legal Action

If you are unable to reach a settlement through negotiation, you may need to pursue legal action. Depending on the amount of damages, you can file a lawsuit in small claims court or civil court. Keep in mind that civil court cases typically require the representation of a personal injury attorney. Settling out of court is generally less stressful and more efficient, so it is advisable to try to reach an agreement through the negotiation process before resorting to legal action.

Summit Medical Group: Insurance Coverage and Acceptance Details

You may want to see also

Frequently asked questions

The first step is to submit a demand letter to the responsible party's insurance company. This letter should include how the accident happened, how the defendant is responsible for the accident, the extent of your injuries and damages, and how you have suffered.

After submitting your demand letter, the insurance company will likely assign an adjuster to your case. The adjuster will investigate your claim and determine whether it falls within the scope of the insurance policy. They will also try to refute your claims of liability and damages. It is important to be patient during this process and not settle for less than what you deserve.

If your health insurer refuses to pay your claim or ends your coverage, you have the right to appeal their decision. You can request an internal appeal, where the insurance company conducts a full and fair review of its decision. If you are still unsatisfied, you can pursue an external review, where an independent third party will review the decision.