Prepaid insurance is a payment made by individuals and businesses to their insurers in advance for insurance services or coverage. It is considered a prepaid asset, which is a way to express the benefits of the insurance policy in accounting terms. Prepaid insurance is important because it helps businesses correctly record all their transactions and resources to have accurate financial statements. Prepaid insurance is usually recorded in a T-account, where the unexpired cost is reported in the current asset account. The expired portion is then moved from the current asset account to the income statement account.

| Characteristics | Values |

|---|---|

| Definition | Prepaid insurance refers to payments made by individuals and businesses to their insurers in advance for insurance services or coverage. |

| Importance | Prepaid insurance helps businesses correctly record all their transactions and resources to have accurate financial statements. |

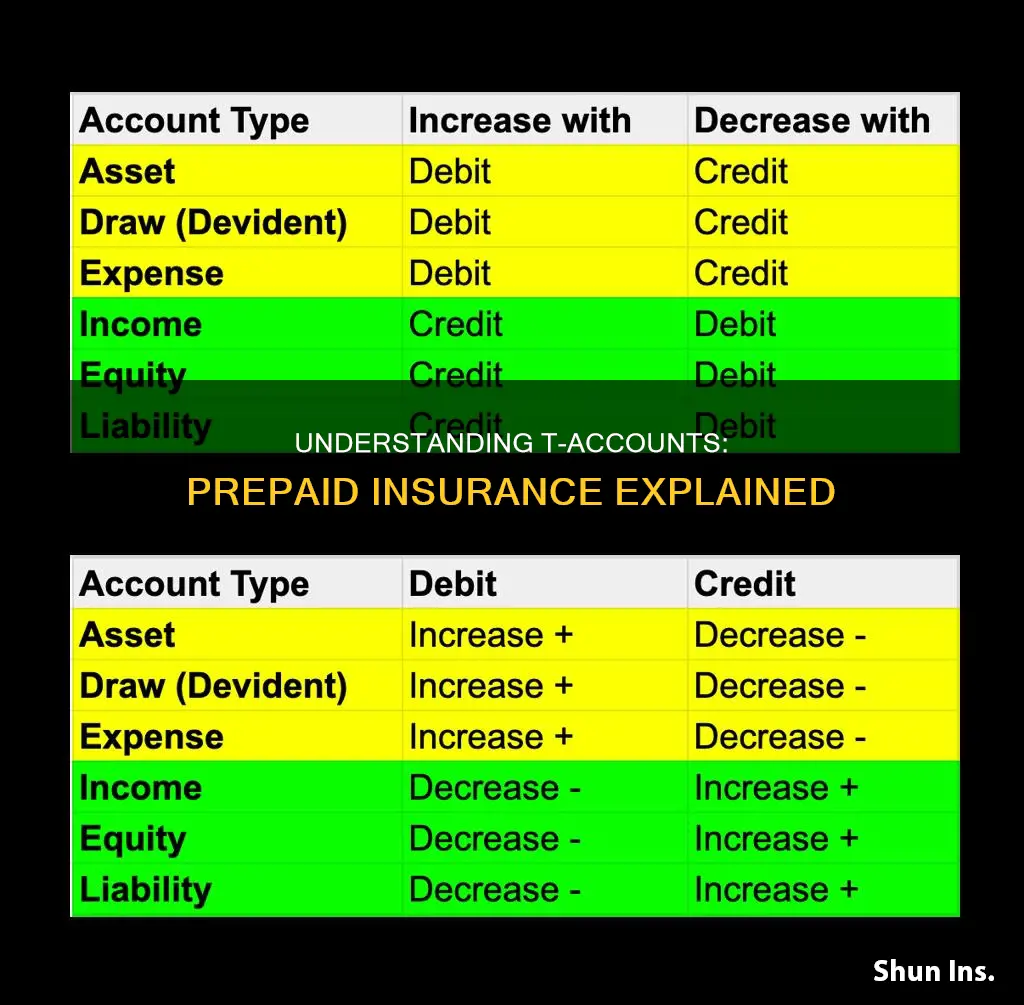

| Accounting | Prepaid insurance is recorded as a current asset and adjusted as the policy is consumed to reflect the true value of the policy over time. |

| Journal Entries | Adjusting journal entries are done each month, and at the end of the year, the prepaid insurance balance would be 0. |

| Renewal | Prepaid insurance is usually renewable by the policyholder before the expiry date on the same terms and conditions as the original contract, with potentially marginally higher premiums. |

| Long-term Asset | If a prepaid expense is not consumed within a year, it becomes a long-term asset, which is rare. |

Explore related products

What You'll Learn

![]()

Recording prepaid insurance as an asset

Prepaid insurance is a type of prepaid expense, which are expenditures that have been paid in advance by a company but have not yet been recorded as an expense. Prepaid expenses are considered assets because they represent money that has future value to the company. In the case of prepaid insurance, it is the portion of an insurance premium that has been paid in advance and has not expired as of the date of a company's balance sheet.

When a company prepays for an expense, it is initially recognised as a prepaid asset on the balance sheet, with a simultaneous entry being recorded that reduces the company's cash account by the same amount. Prepaid expenses are first recorded in the prepaid asset account on the balance sheet. Most prepaid expenses appear on the balance sheet as current assets unless they are not incurred until after 12 months, in which case they become long-term assets.

As the benefits of the expenses are recognised, the related asset account is decreased and expensed. This is done through adjusting journal entries, which are typically made each month. For prepaid insurance, this involves moving the expired portion of the prepaid expense from the current asset account Prepaid Insurance to the income statement account Insurance Expense. At the end of the year, when the insurance policy has no future economic benefits, the prepaid insurance balance would be 0.

It is important to note that prepaid expenses require careful tracking to ensure accurate financial reporting. Investors and auditors look at how companies handle their prepaid expenses to gauge financial health and compliance with accounting standards. Proper tracking of prepaid expenses is also crucial for taxes and financial reporting since the costs must be recognised in the same period the benefits are used, not when the payment is made.

Insurance Money and Tithing: Should You Include It?

You may want to see also

Explore related products

![]()

Adjusting journal entries

Prepaid insurance is an insurance payment made by individuals and businesses to their insurers in advance for insurance services or coverage. Prepaid expenses are expenses paid for in advance and do not provide value right away. Instead, they provide value over time, generally over multiple accounting periods. Prepaid expenses are considered assets because they provide future economic benefits to the company.

Prepaid expenses may need to be adjusted at the end of the accounting period. The adjusting entry for prepaid expenses depends on the journal entry made when it was initially recorded. There are two ways of recording prepayments: the asset method and the expense method. Under the asset method, a prepaid expense account (an asset) is recorded when the amount is paid. Prepaid expense accounts include prepaid insurance, prepaid rent, and office supplies.

To create the first journal entry for prepaid expenses, debit your prepaid expense account. Assets are increased by debits, and for every debit, there must also be a credit. Credit the corresponding account used to make the payment, such as a Cash or Checking account. As you use the prepaid item, decrease your Prepaid Expense account and increase your actual Expense account. To do this, debit your Expense account and credit your Prepaid Expense account. This creates a prepaid expense adjusting entry.

For example, if you prepay six months' worth of rent, which totals $6,000, you would first debit the Prepaid Expense account to show an increase in assets. Then, you would credit the Cash account to show the loss of cash. As each month passes, adjust the accounts by the amount of rent used. Since the prepayment is for six months, divide the total cost by six ($6,000 / 6). Adjust your accounts by $1,000 each month. Expense $1,000 of the rent with a debit. Reduce the Prepaid Expense account with a credit.

The adjusting journal entry is done each month, and at the end of the year, when the insurance policy has no future economic benefits, the prepaid insurance balance would be 0.

Understanding Adjustable ComLife Insurance: Flexibility for a Dynamic Life

You may want to see also

Explore related products

![]()

Calculating the unexpired portion of the policy

Prepaid insurance is a payment made by individuals and businesses to their insurers in advance for insurance services or coverage. It is usually paid annually, but in some cases, it may cover more than 12 months. When prepaid insurance is purchased, the contract generally covers a period of time in the future. For example, a company may pay an insurance premium of $2400 for insurance protection during a six-month period from December 1 to May 31.

The full value of the prepaid insurance is recorded as a debit to the asset account and as a credit to the cash account. As the benefits of the expenses are recognized, the related asset account is decreased and expensed. Each month, as a portion of the prepaid premiums are applied, an adjusting journal entry is made as a credit to the asset account and as a debit to the insurance expense account. This is usually done at the end of each accounting period.

For instance, on November 20, a company pays an insurance premium of $2400 for insurance protection during the six-month period of December 1 through May 31. On November 20, the payment is entered with a debit of $2400 to Prepaid Insurance and a credit of $2400 to Cash. As of November 30, none of the $2400 cost has expired, and the entire $2400 will be reported on the balance sheet as Prepaid Insurance or Prepaid Expenses. On December 31, an adjusting entry will debit Insurance Expense for $400 (the amount that expired: 1/6 of $2400) and will credit Prepaid Insurance for $400. This means that the debit balance in Prepaid Insurance at December 31 will be $2,000 (5/6 of the $2,400 cost), since this is the amount that has not yet expired.

At the end of the year, when the insurance policy has no future economic benefits, the prepaid insurance balance would be 0. This is because the asset value of the prepaid insurance will be reduced to zero at the end of the time period that was paid for in advance.

Adjusting Insurance Stipends: The Age Factor

You may want to see also

Explore related products

![]()

Recognising the economic benefits of prepaid insurance

Prepaid insurance is a type of prepaid expense, which refers to payments made by individuals and businesses to their insurers in advance for insurance services or coverage. It is usually paid a full year in advance, but in some cases, it may cover more than 12 months. Prepaid insurance is considered an asset because it provides future economic benefits to the insured party.

From a financial accounting perspective, prepaid insurance is considered a prepayment. It is initially recorded as a current asset on the balance sheet, reflecting the fact that the coverage is for a future point in time. As the coverage term progresses and sections of the prepaid insurance are expensed, the related asset account is decreased and the prepaid insurance account is credited to reflect the decrease in the prepaid amount. This process is known as the matching principle in accounting, where expenses are matched with the revenues they generate.

The economic benefits of prepaid insurance include financial stability, budgeting precision, and risk mitigation. By paying for insurance coverage in advance, businesses can smoothen their financial operations and enhance overall risk management. Prepaid insurance provides the benefit of obtaining services at a predetermined cost, aiding in budgeting and financial planning. It also ensures continual risk prevention, as the insurance coverage is already in place for a specified period.

Additionally, prepaid insurance can simplify accounting processes. As mentioned earlier, the matching principle helps align expenses with the corresponding revenues. This makes it easier to track and manage financial transactions, especially with the assistance of AI/ML-powered tools that can automate data extraction and reconciliation. Prepaid insurance also provides flexibility in terms of renewal. Unless a claim is filed, prepaid insurance policies can usually be renewed shortly before the expiry date on the same terms and conditions, with potential adjustments for inflation and other factors.

TRIA and Commercial Insurance: What You Need to Know

You may want to see also

Explore related products

![]()

The process of renewing prepaid insurance

Prepaid insurance is a type of insurance in which the premium or payment is made in advance of the insurance coverage period. It is typically paid a full year in advance, but in some cases, it may cover a longer period. Prepaid insurance is considered a current asset on a company's balance sheet until it is consumed or expires. As the prepaid insurance amount is consumed or expires, it is moved from the current asset account (Prepaid Insurance) to the income statement account (Insurance Expense). This is usually done through an adjusting entry at the end of each month or accounting period.

When it comes to renewing prepaid insurance, the process typically begins three to four months before the current policy's expiration date. During this period, it is important to review the renewal proposal at least 30 days before the policy's expiration to ensure satisfaction and address any concerns. Creating a stewardship assessment report can help the institution and the insurance provider to align their expectations and ensure that the services provided meet the institution's needs.

Effective insurance renewal involves proactive marketing to assess competitiveness across insurance carriers. It is beneficial to maintain a strong relationship with the current insurance carrier and give them the first opportunity to retain the business. However, it is also crucial to compare quotes and renewal pricing from other carriers to ensure the best value and coverage for the institution.

To renew prepaid insurance, the policyholder can usually renew the coverage shortly before the expiry date on the same terms and conditions as the original insurance contract. The premiums may be slightly higher to account for inflation and other factors. It is important to note that the renewal process may vary depending on the insurance provider and the specific terms of the policy.

Farmers Insurance Commercials: Fact or Fiction?

You may want to see also

Frequently asked questions

Prepaid insurance is a type of prepaid expense where payments are made to insurers in advance for insurance services or coverage. It is considered a prepaid asset because it benefits future accounting periods.

Prepaid insurance is recorded in the general ledger as a prepaid asset under current assets. The full value of the prepaid insurance is recorded as a debit to the asset account and as a credit to the cash account. Each month, as a portion of the prepaid premiums are applied, an adjusting journal entry is made as a credit to the asset account and as a debit to the insurance expense account.

Prepaid insurance relieves businesses of the monthly premium expense, reducing their costs while retaining the benefit of coverage. It also has economic value as it can be redeemed at a later time, similar to an investment in stocks or bonds.