When liability insurance premiums increase, it’s essential to approach the conversation with clarity, empathy, and a focus on solutions. Start by acknowledging the financial impact and expressing understanding of the concerns it may raise. Clearly explain the reasons behind the increase, whether due to market trends, higher risk assessments, or policy adjustments. Provide transparency about the value the insurance offers, such as enhanced coverage or protection against potential liabilities. Offer actionable steps, such as exploring cost-saving options, adjusting coverage limits, or bundling policies. Encourage open dialogue to address questions or worries, ensuring the discussion remains constructive and collaborative. Ultimately, the goal is to balance financial responsibility with maintaining adequate protection, fostering trust and confidence in the decision-making process.

| Characteristics | Values |

|---|---|

| Understand the Reason | Research and understand why the liability insurance premium increased (e.g., claims history, industry trends, policy changes). |

| Be Prepared with Data | Gather data on your safety record, risk mitigation efforts, and any improvements made to reduce liability risks. |

| Focus on Value | Emphasize the value of the insurance coverage and how it protects your business from financial loss. |

| Negotiate Terms | Discuss potential adjustments to policy limits, deductibles, or coverage to manage costs without compromising protection. |

| Highlight Risk Management | Showcase your proactive risk management strategies (e.g., employee training, safety protocols) to justify lower premiums. |

| Compare Quotes | Obtain quotes from multiple insurers to demonstrate market competitiveness and negotiate better rates. |

| Long-Term Relationship | Leverage your long-term relationship with the insurer to request loyalty discounts or favorable terms. |

| Bundle Policies | Explore bundling liability insurance with other policies (e.g., property, workers' comp) for potential discounts. |

| Payment Flexibility | Request flexible payment options or annual payments to reduce immediate financial burden. |

| Review Policy Annually | Commit to annual policy reviews to ensure coverage aligns with your business needs and risk profile. |

| Consult an Expert | Seek advice from an insurance broker or attorney to navigate negotiations and ensure optimal coverage. |

| Stay Professional | Maintain a calm and professional tone during discussions to foster a collaborative negotiation environment. |

Explore related products

What You'll Learn

- Explain Coverage Changes: Highlight increased risks or policy adjustments driving the premium hike

- Compare Market Rates: Show how your new rate aligns with industry standards

- Risk Mitigation Steps: Share actions taken to reduce future claims and costs

- Payment Flexibility: Offer adjusted payment plans to ease financial burden

- Value Proposition: Emphasize continued benefits and protection despite higher costs

![]()

Explain Coverage Changes: Highlight increased risks or policy adjustments driving the premium hike

Insurance premiums don't rise in a vacuum. Policyholders often face increased liability insurance costs due to specific coverage changes, reflecting evolving risks or adjustments in policy terms. Understanding these changes is crucial for informed decision-making. For instance, a commercial policyholder might see a premium hike due to expanded coverage for cyber liability, a response to the rising tide of data breaches. This addition, while beneficial, directly impacts the overall cost.

Resisting the urge to simply accept or reject the increase, policyholders should scrutinize the policy documents for specific changes. Look for additions like increased coverage limits, new endorsements, or broadened definitions of covered events. These changes often correlate with emerging risks identified by insurers, such as increased litigation trends or new regulatory requirements.

Consider a scenario where a homeowner's liability insurance premium jumps by 15%. Instead of assuming it's arbitrary, delve into the policy details. Perhaps the insurer has added coverage for sewer backup damage, a growing concern in the area due to aging infrastructure. While this addition provides valuable protection, it directly contributes to the premium increase. Understanding this linkage empowers the policyholder to assess the value of the added coverage against the cost.

A proactive approach involves anticipating potential coverage changes. Reviewing industry trends and local risk factors can provide clues. For example, areas prone to wildfires might see insurers introduce stricter underwriting guidelines or higher deductibles for fire-related claims, leading to premium adjustments. Being aware of these trends allows policyholders to prepare for potential changes and engage in informed discussions with their insurers.

Ultimately, transparency is key. Insurers should clearly communicate coverage changes and their impact on premiums. Policyholders, armed with knowledge and a proactive mindset, can then evaluate the necessity of these changes and negotiate terms if needed. Remember, understanding the "why" behind the increase empowers you to make informed choices about your liability insurance coverage.

CDBG Funding and Self-Insured Entities: Eligibility and Compliance Explained

You may want to see also

Explore related products

![]()

Compare Market Rates: Show how your new rate aligns with industry standards

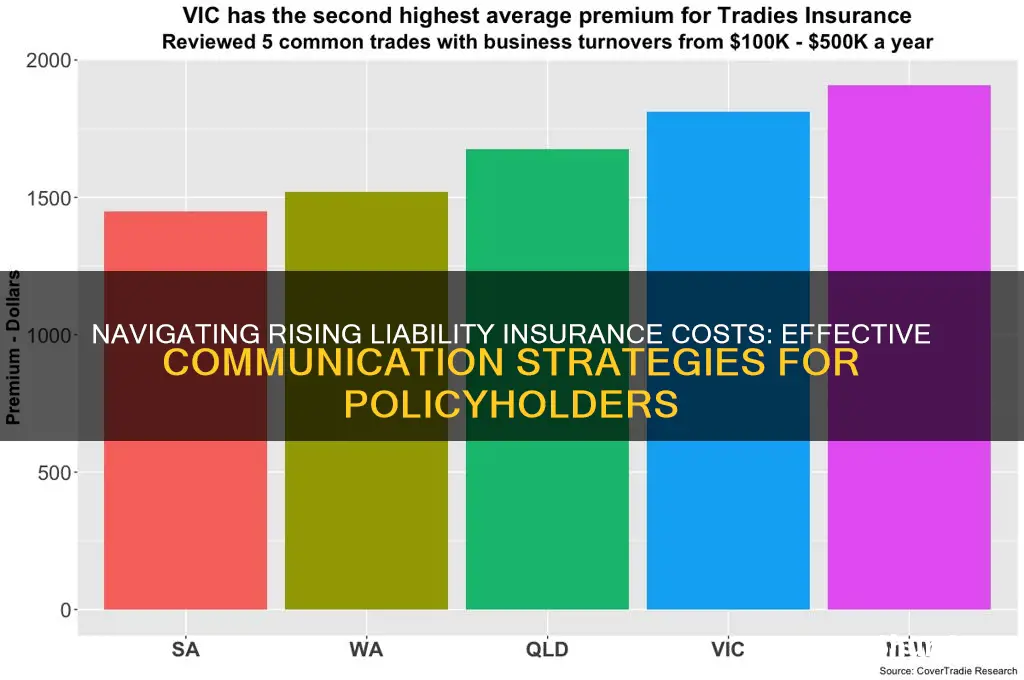

Insurance premiums don't exist in a vacuum. When faced with a liability insurance increase, your first instinct might be to balk at the number. Before you do, take a deep dive into the market. Compare your new rate against industry benchmarks for businesses of your size, location, and risk profile. Industry publications, insurance comparison websites, and even your broker can provide valuable data points.

Let's say you're a small landscaping business and your liability insurance just jumped 15%. Instead of simply reacting, research the average premium increase for landscaping businesses in your region over the past year. If the industry average is 12%, your increase, while unwelcome, is at least in line with market trends. This context is crucial for understanding whether your hike is an anomaly or a reflection of broader economic forces.

A 2022 survey by the Insurance Information Institute found that commercial liability insurance rates rose an average of 8% nationally, with certain industries like construction and transportation seeing even steeper climbs.

Don't rely solely on national averages. Local factors like litigation trends, regulatory changes, and even weather patterns can significantly impact insurance costs. For instance, a region prone to severe storms might see higher premiums due to increased property damage claims.

Armed with this market data, you can have a more informed conversation with your insurer. If your increase is significantly higher than industry averages, you have a stronger case for negotiating a better rate or exploring alternative providers. Remember, knowledge is power, especially when it comes to navigating the often opaque world of insurance.

Whole Life Insurance: Paid Up or Not?

You may want to see also

Explore related products

![]()

Risk Mitigation Steps: Share actions taken to reduce future claims and costs

Rising liability insurance premiums often signal a need to reevaluate risk management strategies. Instead of simply accepting higher costs, proactive businesses take concrete steps to demonstrate their commitment to safety and reduce future claims. This not only strengthens their negotiating position with insurers but also fosters a culture of responsibility.

Let's explore actionable risk mitigation measures that can effectively communicate your dedication to minimizing liability exposure.

Implement Comprehensive Training Programs: Invest in regular, role-specific training for all employees. This includes safety protocols, hazard identification, and proper equipment usage. For example, a construction company might mandate monthly refresher courses on fall protection for roofers, while a restaurant could implement quarterly food safety training for kitchen staff. Documenting these training sessions provides tangible evidence of your commitment to risk reduction.

Conduct Regular Risk Assessments: Proactively identify potential hazards through systematic inspections and audits. This could involve monthly walkthroughs of facilities, equipment checks, and reviews of incident reports. A manufacturing plant, for instance, might conduct weekly inspections of machinery for potential malfunctions, while a retail store could assess customer traffic flow to prevent slips and falls. Addressing identified risks promptly demonstrates a proactive approach to safety.

Establish Clear Policies and Procedures: Develop written policies outlining safety expectations, reporting procedures for incidents, and disciplinary actions for violations. Ensure these policies are easily accessible to all employees and regularly reviewed and updated. A clear, well-communicated policy framework minimizes confusion and encourages adherence to safety protocols.

Invest in Safety Equipment and Technology: Provide employees with the necessary tools and equipment to perform their jobs safely. This could include personal protective equipment (like hard hats and safety goggles), ergonomic furniture, or advanced safety systems like automated emergency shut-off mechanisms. For example, a landscaping company might invest in noise-canceling headphones for employees operating loud machinery, while a delivery service could equip vehicles with GPS tracking and dashcams.

Foster a Culture of Safety: Encourage open communication about safety concerns and empower employees to report hazards without fear of retaliation. Recognize and reward safe behavior, and actively involve employees in safety initiatives. A culture where safety is a shared responsibility significantly reduces the likelihood of accidents and claims.

By implementing these risk mitigation steps, businesses can demonstrably reduce their liability exposure, leading to lower insurance premiums and a safer work environment. Remember, insurers view proactive risk management favorably, translating into tangible cost savings and long-term stability.

Understanding COBRA: Life Insurance Coverage and Benefits

You may want to see also

Explore related products

![]()

Payment Flexibility: Offer adjusted payment plans to ease financial burden

Rising liability insurance premiums can strain even the most resilient businesses. One effective strategy to mitigate this financial pressure is to offer adjusted payment plans, providing clients with the flexibility they need to manage increased costs. This approach not only demonstrates empathy but also strengthens client relationships by showing a commitment to their long-term success.

Consider structuring payment plans around seasonal cash flow patterns. For instance, a landscaping business might face higher insurance costs during peak seasons but struggle with cash flow in winter months. Offering a plan that allows for lower payments during off-peak periods and higher payments when revenue is strong can alleviate financial stress. Similarly, businesses with predictable revenue cycles, such as retailers during holiday seasons, can benefit from aligned payment schedules. The key is to tailor plans to the client’s unique financial rhythm, ensuring payments are manageable without disrupting operations.

Another practical strategy is to introduce tiered payment options based on the client’s financial capacity. For example, small businesses with limited budgets could opt for monthly installments with slightly higher interest rates, while larger enterprises might prefer quarterly payments with reduced fees. This approach requires clear communication about the trade-offs involved, ensuring clients understand the implications of their choices. Providing a detailed breakdown of each plan’s total cost, including any additional fees, fosters transparency and trust.

To implement these plans effectively, leverage technology to streamline the process. Automated billing systems can handle recurring payments, reducing administrative burdens and minimizing errors. Additionally, offering digital payment portals allows clients to manage their accounts conveniently, enhancing their overall experience. Pairing these tools with personalized follow-ups ensures clients feel supported and valued, even as they navigate financial challenges.

Ultimately, offering adjusted payment plans is not just about easing financial burdens—it’s about building resilience. By providing clients with flexible options, you empower them to adapt to increased insurance costs without compromising their operations. This proactive approach not only preserves client relationships but also positions your business as a trusted partner in their financial journey.

Do Passengers Need Insurance When Riding with a Learner Driver?

You may want to see also

Explore related products

$33.14 $39.99

![]()

Value Proposition: Emphasize continued benefits and protection despite higher costs

Rising liability insurance premiums can feel like a punch to the gut, especially for small businesses already navigating tight margins. But before you hit the panic button, remember: this isn't just about cost, it's about value.

Reframe the Conversation: Instead of leading with the price hike, start by reaffirming the core value proposition of liability insurance. Remind your audience (clients, stakeholders, employees) that this coverage isn't a luxury, it's a shield. It protects their livelihood, their reputation, and their financial stability in the face of unforeseen events.

Quantify the Intangible: Don't just say "peace of mind" – show it. Share real-world examples of how liability insurance has safeguarded businesses similar to theirs. Highlight the potential financial devastation of a lawsuit without adequate coverage. For instance, a slip-and-fall claim can easily reach six figures, dwarfing even a significant premium increase.

Tiered Benefits: If possible, break down the policy into tiers of coverage, clearly outlining the additional protections each level offers. This allows clients to see the increased value they're receiving for the higher cost, making the decision less about price and more about choosing the level of protection that aligns with their risk tolerance.

Focus on Long-Term Savings: Frame the increased premium as an investment in long-term financial health. Emphasize that paying a higher premium now can prevent catastrophic losses down the line, ultimately saving them money and protecting their business's future. Think of it as preventative medicine for your business's financial well-being.

Reinstating Root Insurance: A Step-by-Step Guide to Restore Your Coverage

You may want to see also

Frequently asked questions

Be transparent and professional. Explain that due to rising industry costs or increased risk factors, your liability insurance premiums have gone up. Emphasize that this ensures continued protection for both parties and is a standard adjustment in your business operations.

Highlight the value of the added protection and how it benefits them. Frame it as a necessary step to maintain high standards of service and security. Offer to provide documentation or details about the insurance changes if they have concerns.

It depends on your business model and market conditions. If competitors are also adjusting prices, passing on a portion or all of the increase may be reasonable. Consider absorbing some of the cost if possible, but communicate the need for a price adjustment clearly and empathetically.

Anticipate questions and objections by preparing clear, concise explanations. Focus on the long-term benefits of the increased coverage and how it protects their interests. Offer alternatives, such as adjusted service packages, if feasible, to ease the transition.