Understanding whether you have a Health Savings Account (HSA) or traditional insurance can be confusing, as both are tools for managing healthcare costs but serve different purposes. An HSA is a tax-advantaged savings account paired with a high-deductible health plan (HDHP), allowing you to save pre-tax dollars for qualified medical expenses, while traditional insurance typically offers broader coverage with lower out-of-pocket costs but may not include an HSA. To determine which you have, review your plan documents, check for an HSA-eligible high-deductible plan, or contact your employer’s benefits administrator or insurance provider for clarification. Knowing the difference is crucial for maximizing your healthcare benefits and financial planning.

Explore related products

$14.98 $24.99

What You'll Learn

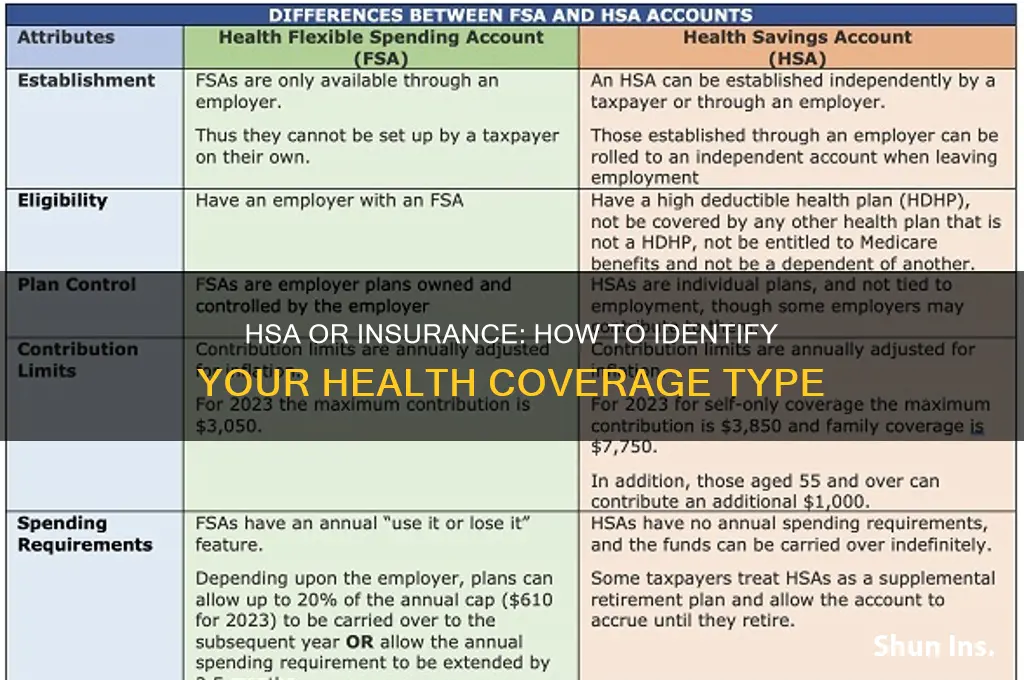

- Check account type: Look for HSA label on statements or account details

- Review plan documents: Verify if your insurance includes HSA contributions

- Tax forms: Check Form 8889 or 1099-SA for HSA activity

- Employer benefits: Ask HR if your health plan includes an HSA

- Provider portal: Log in to your insurance portal to see HSA status

![]()

Check account type: Look for HSA label on statements or account details

One straightforward method to determine if you have a Health Savings Account (HSA) is to scrutinize your financial statements or account details for an explicit HSA label. Financial institutions typically use clear terminology to distinguish HSAs from other accounts, such as checking, savings, or flexible spending accounts (FSAs). Look for terms like "HSA," "Health Savings Account," or similar identifiers on monthly statements, online banking dashboards, or mobile app interfaces. This label is often accompanied by a unique account number or suffix that differentiates it from other accounts. If you’re unsure, cross-reference the account type with any documentation provided when the account was opened, as this will often explicitly state its purpose.

Analyzing your account statements can reveal more than just the label. HSAs often come with specific transaction patterns, such as contributions from your employer or yourself, withdrawals for qualified medical expenses, and potential investment activity if the account offers that feature. For instance, contributions to an HSA are typically tax-deductible, so you might notice regular deposits labeled as "HSA Contribution" or "Employer HSA Deposit." Withdrawals, on the other hand, should align with medical expenses, often accompanied by descriptions like "Pharmacy Purchase" or "Doctor Visit." If your account reflects these patterns, it’s a strong indicator that you have an HSA rather than a general insurance policy or FSA.

A practical tip for those who manage multiple accounts is to use color-coding or digital tags to differentiate your HSA from other accounts. Most online banking platforms allow you to rename or categorize accounts for easier identification. Labeling your HSA clearly in your digital banking tools can prevent confusion, especially if you have multiple health-related accounts. Additionally, if you’re still uncertain after reviewing statements, contact your bank or HSA provider directly. They can confirm the account type and provide guidance on how to maximize its benefits, such as understanding contribution limits (e.g., $3,850 for individuals and $7,750 for families in 2023) or eligible expenses.

Comparatively, while insurance policies often come with detailed summaries of coverage, premiums, and deductibles, HSAs are financial accounts tied to high-deductible health plans (HDHPs). This distinction is crucial because an HSA is not insurance itself but a tool to save for medical expenses. If your account details include terms like "deductible," "coinsurance," or "out-of-pocket maximum," you’re likely looking at insurance documentation, not an HSA. However, if the focus is on contributions, balances, and transactions, it’s almost certainly an HSA. Understanding this difference ensures you don’t mistakenly conflate the two, allowing you to leverage both effectively for your healthcare needs.

Life Insurance Arbitration: What You Need to Know

You may want to see also

Explore related products

![]()

Review plan documents: Verify if your insurance includes HSA contributions

Your health insurance plan documents are the definitive source for understanding whether your coverage includes a Health Savings Account (HSA). These documents, often dense and jargon-heavy, hold the key to unlocking this crucial detail. Think of them as a treasure map, where "HSA eligibility" or "HSA contributions" are the X marking the spot.

Step 1: Locate the Summary of Benefits and Coverage (SBC). This concise document, typically 4-6 pages, provides a snapshot of your plan's key features. Look for a section titled "Health Savings Account" or "HSA Compatibility." If present, it will explicitly state whether your plan is HSA-eligible and may even outline contribution limits or employer matching programs.

Step 2: Scrutinize the Plan Document or Certificate of Coverage. This more comprehensive document delves deeper into the specifics of your plan. Search for terms like "High Deductible Health Plan (HDHP)" – a prerequisite for HSA eligibility. HSA-compatible plans are always HDHPs, but not all HDHPs are HSA-eligible, so confirmation is essential.

Caution: Don't be misled by terms like "health savings" or "flexible spending account" (FSA). These are distinct from HSAs and have different rules and tax implications.

Step 3: Contact Your Insurance Provider or Employer. If the documents remain unclear, don't hesitate to reach out. Customer service representatives or HR personnel can provide clarification and guide you to the relevant sections within the plan documents.

Takeaway: While deciphering insurance documents can be daunting, identifying HSA eligibility is a worthwhile endeavor. HSAs offer unique tax advantages and flexibility for managing healthcare expenses. By carefully reviewing your plan documents and seeking clarification when needed, you can unlock the potential benefits of this powerful financial tool.

European Insurance Systems: Diverse Approaches to Risk Management and Coverage

You may want to see also

Explore related products

![]()

Tax forms: Check Form 8889 or 1099-SA for HSA activity

If you're unsure whether you have a Health Savings Account (HSA), tax season offers a clear opportunity to verify its existence. Two specific IRS forms—Form 8889 and Form 1099-SA—are designed to report HSA activity, making them essential tools for confirmation. Form 8889, titled "Health Savings Accounts (HSAs)," is used to report contributions, distributions, and the account's fair market value. If you've received this form, it’s a strong indicator that you have an active HSA. Similarly, Form 1099-SA, "Distributions From an HSA, Archer MSA, or Medicare Advantage MSA," details any withdrawals made from your HSA during the tax year. Both forms are sent to you and the IRS by your HSA custodian, ensuring transparency and compliance.

Analyzing these forms provides more than just confirmation—it offers insight into your HSA usage. Form 8889 breaks down contributions, including those made by your employer, and tracks whether distributions were used for qualified medical expenses. This form also calculates any excess contributions, which may require repayment or incur penalties. Form 1099-SA, on the other hand, lists all distributions, helping you verify that withdrawals were tax-free if used for eligible expenses. Together, these forms serve as a financial snapshot of your HSA, highlighting its role in your healthcare and tax strategy.

For those unfamiliar with these forms, navigating them can seem daunting. Start by locating the forms in your tax documents or online portal. Form 8889 is typically filed with your tax return, while Form 1099-SA is issued by January 31st if you made any HSA distributions. If you’re missing either form but suspect you have an HSA, contact your HSA custodian immediately. They can provide copies or clarify whether an account exists under your name. Remember, failing to report HSA activity accurately can lead to penalties, so diligence is key.

A practical tip for maximizing these forms’ utility is to cross-reference them with your HSA statements. Ensure contributions and distributions match your records to catch discrepancies early. For instance, if Form 1099-SA shows a distribution you don’t recall, investigate whether it was an automatic payment for a qualified expense. Additionally, use Form 8889 to plan future contributions, as it highlights contribution limits and potential tax benefits. By treating these forms as more than just tax requirements, you can actively manage your HSA to align with your financial and healthcare goals.

In conclusion, Forms 8889 and 1099-SA are not just tax documents—they’re diagnostic tools for understanding your HSA. Whether you’re confirming the account’s existence, verifying activity, or planning for the future, these forms provide critical information. By familiarizing yourself with their structure and purpose, you can ensure compliance while optimizing your HSA’s benefits. Don’t overlook them; they’re your gateway to a clearer picture of your healthcare savings strategy.

Insurance Careers: A-1 Opportunities and Benefits

You may want to see also

Explore related products

![]()

Employer benefits: Ask HR if your health plan includes an HSA

Your employer’s benefits package is a treasure trove of potential savings, but deciphering its contents can feel like cracking a code. One key question to unlock hidden value: *Does my health plan include a Health Savings Account (HSA)?* HSAs aren’t just another acronym in the benefits alphabet—they’re tax-advantaged accounts that can supercharge your healthcare savings. Unlike Flexible Spending Accounts (FSAs), HSAs roll over year to year, grow tax-free, and can be invested for long-term growth. But here’s the catch: HSAs are only available with high-deductible health plans (HDHPs), which your employer may or may not offer.

Start by reviewing your benefits summary, but don’t stop there. HR departments are your best resource for clarity. Schedule a meeting or send a detailed email asking: *“Is my current health plan paired with an HSA option?”* Be specific. Mention whether you’re enrolled in an HDHP, as this is a prerequisite for HSA eligibility. If you’re unsure, ask HR to confirm the plan type. They can also guide you on contribution limits—for 2023, individuals can contribute up to $3,850, and families up to $7,750, with an additional $1,000 catch-up contribution if you’re 55 or older.

Here’s why this matters: HSAs offer a triple tax advantage—contributions are tax-deductible, funds grow tax-free, and withdrawals for qualified medical expenses are also tax-free. Even better, once you turn 65, you can use HSA funds for non-medical expenses without penalty (though they’ll be taxed as income). If your employer offers an HSA, they may even contribute to it, effectively giving you free money. For example, some companies match contributions up to $500 annually, boosting your savings without additional cost.

A word of caution: Not all HDHPs are created equal. While an HSA can offset high out-of-pocket costs, ensure the plan’s deductible and premiums align with your healthcare needs. If you’re young and healthy, an HDHP with an HSA might be ideal. But if you have chronic conditions or frequent medical needs, the high deductible could outweigh the HSA’s benefits. Ask HR for a breakdown of the plan’s costs, including deductibles, copays, and coinsurance, to make an informed decision.

Finally, take action. If your plan includes an HSA, enroll immediately and maximize your contributions. If not, ask HR if they’re considering adding an HDHP with HSA option in the future. Employers often adjust benefits based on employee feedback. By advocating for HSA-compatible plans, you’re not just securing your own financial health—you’re helping shape a benefits package that benefits everyone. Remember, clarity starts with a conversation, and HR is your gateway to unlocking this powerful tool.

Year-Round Insurance Coverage for School Bus Drivers: What You Need to Know

You may want to see also

Explore related products

![]()

Provider portal: Log in to your insurance portal to see HSA status

One of the most direct ways to determine whether you have a Health Savings Account (HSA) is by accessing your insurance provider’s portal. This digital platform serves as a centralized hub for policy details, benefits, and account statuses, including HSA information. If you’re unsure whether your plan includes an HSA, logging in can provide immediate clarity. Most insurance portals categorize HSA details under sections like “Benefits,” “Accounts,” or “Coverage Details.” Look for terms such as “HSA Balance,” “Contributions,” or “Eligible Expenses” to confirm its presence.

To access this information, start by visiting your insurance provider’s website and locating the login section for policyholders. You’ll typically need your username and password, which were provided when you enrolled in the plan. If you’ve forgotten your credentials, use the “Forgot Password” or “Need Help Logging In?” feature to regain access. Once logged in, navigate to the dashboard or main menu. HSA details are often listed alongside other account features, such as claims history or deductible tracking. If the interface feels overwhelming, use the search bar (if available) and type “HSA” to quickly locate relevant information.

A key advantage of using the provider portal is its real-time data. Unlike paper statements or customer service calls, the portal reflects up-to-date contributions, balances, and transactions. For example, if your employer recently made an HSA contribution, it will appear here first. Additionally, many portals offer tools to manage your HSA, such as transferring funds, viewing eligible expenses, or linking a debit card. This functionality not only confirms the existence of your HSA but also empowers you to actively manage it.

However, be aware of potential limitations. Not all insurance portals are user-friendly, and some may bury HSA details under layers of menus. If you’re struggling to find the information, consider reaching out to your provider’s customer service for guidance. Another caution: ensure you’re logging into the correct portal, especially if you have multiple insurance plans. For instance, if you have separate medical and dental coverage, the HSA details will only appear in the portal associated with your high-deductible health plan (HDHP).

In conclusion, logging into your insurance provider’s portal is a straightforward and efficient method to verify your HSA status. By leveraging this tool, you gain immediate access to critical account details and management options. While the process may require some navigation, the clarity it provides is invaluable for understanding your healthcare and financial benefits. Make it a habit to check your portal periodically, especially during open enrollment or after significant plan changes, to stay informed about your HSA and overall coverage.

Life Insurance and Globulin: Understanding the Rating Connection

You may want to see also

Frequently asked questions

Check your enrollment documents or contact your employer’s benefits department. An HSA is typically paired with a high-deductible health plan (HDHP), while regular insurance may have lower deductibles and no HSA.

An HSA is a tax-advantaged savings account used for medical expenses, paired with an HDHP. Traditional insurance usually has lower out-of-pocket costs but does not include an HSA.

No, HSAs are only available with high-deductible health plans (HDHPs). If you have regular insurance with a low deductible, you cannot contribute to an HSA.

Your plan must meet IRS requirements for a high-deductible health plan (HDHP). Check your plan’s summary or ask your insurance provider for confirmation.

Look for statements from your HSA provider (if applicable) or review your insurance plan documents. You can also check your payroll deductions for HSA contributions.