The question of whether a property located 10 feet above sea level is insurable is a critical concern for homeowners and insurers alike, particularly in regions prone to flooding, storm surges, or rising sea levels. Insurability at this elevation depends on various factors, including the property’s location, local flood risk assessments, and the insurer’s underwriting guidelines. Properties at or near sea level often face higher premiums or limited coverage due to increased vulnerability to water damage. However, being 10 feet above sea level may offer some protection, potentially reducing risk and making the property more insurable, though this can vary based on specific geographic and climatic conditions. Understanding FEMA flood maps, local zoning regulations, and the property’s history of claims is essential for determining insurability and securing adequate coverage.

| Characteristics | Values |

|---|---|

| Insurability | Generally insurable, but depends on specific location, flood zone designation, and insurer's guidelines |

| Flood Risk | Moderate to high risk, depending on proximity to coast, rivers, or other water bodies |

| FEMA Flood Zone | Likely Zone AE, A, or V (high-risk zones) |

| Base Flood Elevation (BFE) | Typically below 10 feet, requiring flood insurance and elevation compliance |

| Insurance Premiums | Higher than properties at greater elevations due to increased flood risk |

| Coverage Requirements | Flood insurance through the National Flood Insurance Program (NFIP) or private insurers is often mandatory for mortgages in high-risk zones |

| Mitigation Measures | Elevation certificates, flood vents, and flood-resistant construction may be required to reduce premiums |

| State-Specific Regulations | Varies by state; some states may have additional requirements or incentives for flood-prone properties |

| Climate Change Impact | Increasing risk due to rising sea levels and more frequent severe weather events |

| Appraisal and Inspection | Properties at 10 feet above sea level may require specialized appraisals and inspections to assess flood risk |

| Resale Value | May be affected by flood risk and insurance costs, potentially impacting property value |

Explore related products

![Flood proofing : how to evaluate your options : decision tree. 1995 [Leather Bound]](https://m.media-amazon.com/images/I/61IX47b4r9L._AC_UY218_.jpg)

What You'll Learn

![]()

Flood risk assessment criteria

Flood risk assessment is a critical component in determining whether a property located 10 feet above sea level is insurable. Insurers rely on detailed criteria to evaluate the likelihood and potential severity of flooding, which directly impacts policy premiums and coverage terms. These assessments are not one-size-fits-all; they are tailored to the property’s specific location, topography, and historical data. For instance, a property at 10 feet elevation in a region with frequent storm surges may face higher risk than one in a drier climate, even at the same height. Understanding these criteria helps property owners gauge their insurability and take proactive measures to mitigate risk.

One key criterion in flood risk assessment is the property’s proximity to water bodies and its position within a floodplain. FEMA’s Flood Insurance Rate Maps (FIRMs) categorize areas into zones based on risk, such as Zone A (high risk) or Zone X (low risk). A property 10 feet above sea level might still fall into a high-risk zone if it’s near a river or coastline prone to flooding. Insurers cross-reference these zones with elevation data to determine risk. For example, a property at 10 feet elevation in Zone A may require additional flood insurance, while the same elevation in Zone X might be covered under standard policies. Knowing your zone and elevation is the first step in assessing insurability.

Another critical factor is the property’s construction and protective measures. Insurers evaluate whether the building is elevated on pilings, has flood vents, or uses flood-resistant materials. For a property at 10 feet above sea level, these features can significantly reduce risk and lower insurance costs. For instance, elevating mechanical systems above the base flood elevation (BFE) can prevent costly damage during a flood. Similarly, installing backflow valves or sump pumps can minimize water intrusion. Property owners should consult FEMA’s guidelines for flood-resistant construction to enhance their insurability and reduce long-term costs.

Historical flood data and climate trends also play a pivotal role in risk assessment. Insurers analyze past flood events in the area and project future risks based on climate change models. A property 10 feet above sea level in a region experiencing rising sea levels or increased storm frequency may face escalating premiums over time. Tools like NOAA’s Sea Level Rise Viewer can help property owners visualize potential risks. By staying informed about local climate trends, owners can make data-driven decisions, such as investing in additional flood barriers or purchasing supplemental insurance.

Finally, community-level flood mitigation efforts can influence insurability. Participation in the National Flood Insurance Program’s Community Rating System (CRS) can reduce premiums for residents in eligible communities. These programs encourage measures like preserving natural floodplains, enforcing stricter building codes, and maintaining drainage systems. For a property at 10 feet elevation, living in a CRS-participating community can offset some of the risks associated with its location. Property owners should check their community’s CRS rating and advocate for local flood mitigation initiatives to improve their insurability.

By understanding these flood risk assessment criteria, property owners can navigate the complexities of insuring a property 10 feet above sea level. From zoning and construction to historical data and community efforts, each factor plays a role in determining risk and coverage. Proactive steps, such as elevating structures or participating in mitigation programs, can make a significant difference in both insurability and long-term resilience.

Handling Traffic Citation Letters: Insurance Tips for a Smooth Resolution

You may want to see also

Explore related products

![]()

Insurance policy coverage limits

Properties situated 10 feet above sea level face unique risks, particularly from flooding, which raises critical questions about insurance policy coverage limits. Standard homeowners’ insurance policies typically exclude flood damage, necessitating separate flood insurance through the National Flood Insurance Program (NFIP) or private insurers. For properties at this elevation, coverage limits are often tied to flood zone designations, with moderate-to-low-risk areas (Zone X) having lower premiums but potentially insufficient coverage for catastrophic events. Policyholders must assess whether the default limits—up to $250,000 for residential structures and $100,000 for contents under NFIP—adequately protect their investment, especially in regions prone to storm surges or rising sea levels.

When evaluating coverage limits, consider the property’s replacement cost, not its market value. A home 10 feet above sea level may still be vulnerable to floodwaters during extreme events, and rebuilding costs can exceed policy caps. Private flood insurance policies often offer higher limits, sometimes up to $5 million, and may include additional living expenses during repairs. However, these policies come with stricter underwriting criteria and higher premiums. For instance, a property in Florida with a $300,000 replacement cost might require a private policy to ensure full coverage, despite being slightly above the base flood elevation.

Another factor to weigh is the deductible structure, which directly impacts out-of-pocket costs after a claim. NFIP policies have separate deductibles for building and contents, typically ranging from $1,000 to $10,000. Higher deductibles lower premiums but increase financial exposure during a claim. For a property at 10 feet above sea level, opting for a $5,000 deductible might save $500 annually in premiums but could strain finances if a flood occurs. Balancing affordability with risk tolerance is essential when selecting deductible levels.

Insurability at 10 feet above sea level also hinges on local flood mitigation efforts and historical claims data. Communities with robust flood defenses, such as levees or drainage systems, may qualify for lower premiums and higher coverage limits. Conversely, areas with frequent claims or inadequate infrastructure often face reduced policy options and stricter limits. For example, a property in Houston’s 100-year floodplain might struggle to secure coverage beyond NFIP limits due to repeated flooding events.

Finally, policyholders should periodically review and adjust coverage limits to reflect changing risk profiles. Rising sea levels, increased storm frequency, and urban development can elevate flood risks over time. An annual policy review, coupled with professional appraisals every 3–5 years, ensures coverage remains aligned with current needs. For properties at 10 feet above sea level, staying proactive in assessing and updating insurance limits is not just prudent—it’s a necessity in safeguarding against unforeseen financial losses.

Does FedEx Insure Jewelry? Shipping Precious Items Safely Explained

You may want to see also

Explore related products

![]()

Elevation certificate requirements

An elevation certificate is a critical document for homeowners and insurers alike, particularly in flood-prone areas. It provides precise details about a property’s elevation relative to sea level, which directly impacts flood insurance rates and coverage eligibility. Without this certificate, insurers often default to higher-risk assumptions, resulting in inflated premiums or denied policies. For properties at or near 10 feet above sea level, this document can be the difference between affordable coverage and financial strain.

Obtaining an elevation certificate involves hiring a licensed land surveyor or engineer to measure the property’s height compared to the Base Flood Elevation (BFE), a benchmark set by the Federal Emergency Management Agency (FEMA). The process typically costs between $500 and $1,500, depending on location and property complexity. The surveyor uses specialized equipment to record data, which is then compiled into a standardized FEMA form. This certificate remains valid unless significant changes are made to the property or flood maps are updated.

One common misconception is that elevation certificates are only necessary for homes in designated flood zones. However, properties just outside these zones, such as those 10 feet above sea level, can still benefit from the certificate. Insurers often offer lower rates for homes with documented elevations, even if they’re slightly above the BFE. Additionally, lenders may require this certificate for mortgages in areas with perceived flood risk, regardless of zoning.

For homeowners, the key takeaway is proactive planning. If your property is near 10 feet above sea level, investing in an elevation certificate can yield long-term savings on flood insurance premiums. It also provides clarity during policy renewals or when switching insurers. Keep the certificate updated and readily accessible, as it may be required for FEMA appeals or post-flood claims. In the context of rising sea levels and increased flooding, this document is not just a formality—it’s a safeguard for your financial stability.

Is Insurance Specialist Legit? Uncovering the Truth Behind the Claims

You may want to see also

Explore related products

![]()

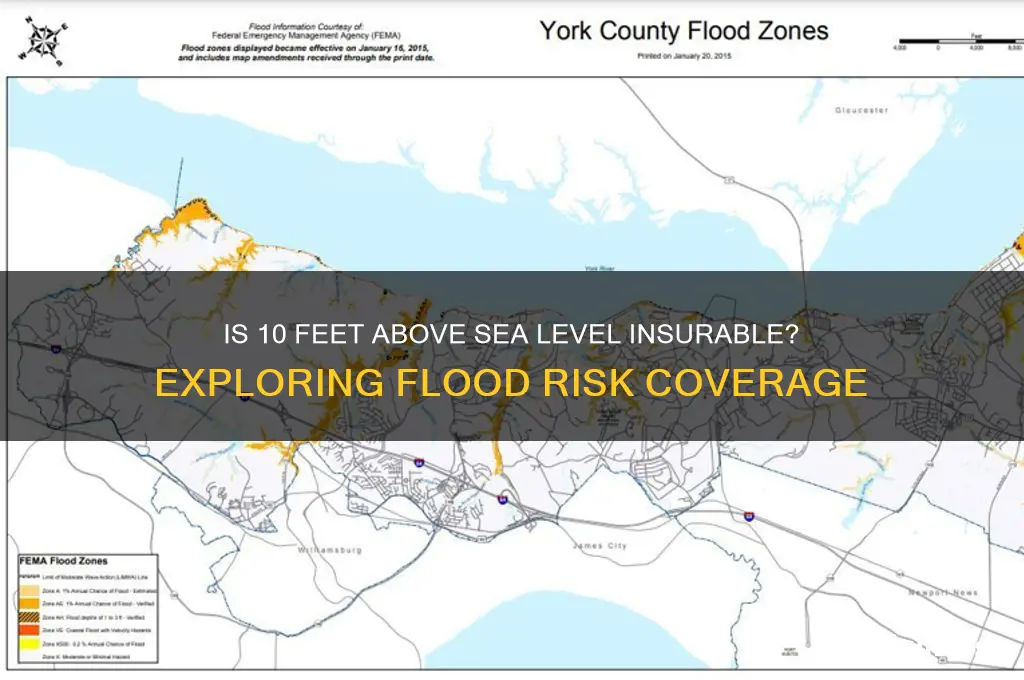

FEMA flood zone categories

The Federal Emergency Management Agency (FEMA) categorizes flood zones to assess risk and guide insurance requirements. These designations, from Zone A to Zone X, reflect varying levels of flood hazard based on factors like elevation, historical data, and proximity to water bodies. Understanding your property’s FEMA flood zone is critical for determining insurability, particularly if it sits 10 feet above sea level. For instance, Zone AE areas have a 1% annual flood risk, while Zone X represents minimal risk. Properties at higher elevations may fall into lower-risk zones, potentially reducing insurance costs. However, FEMA’s maps are periodically updated, so staying informed is essential.

Analyzing FEMA’s Special Flood Hazard Areas (SFHAs) reveals why elevation matters. SFHAs, typically Zones A and AE, require flood insurance for mortgaged properties. If your property is 10 feet above sea level, it might still be in an SFHA if the base flood elevation (BFE) exceeds this height. For example, a BFE of 12 feet would place a 10-foot elevation property in a high-risk zone. Conversely, properties in Zone X or shaded X zones are generally outside SFHAs, making flood insurance optional but still advisable. FEMA’s Flood Map Service Center allows homeowners to verify their zone and BFE, providing clarity on insurability and potential risks.

Persuasively, FEMA’s Community Rating System (CRS) offers a pathway to lower insurance premiums for properties in high-risk zones. Communities participating in the CRS implement floodplain management measures, earning discounts for residents. Even if your property is 10 feet above sea level but in a high-risk zone, living in a CRS community could reduce costs. For example, a property in Zone AE might save up to 45% on flood insurance premiums depending on the community’s CRS rating. This incentivizes proactive local flood mitigation efforts and highlights the importance of community-level actions in individual insurance outcomes.

Comparatively, FEMA’s coastal and riverine flood zones differ in how elevation impacts insurability. Coastal zones, like V (velocity hazard) and VE (coastal high hazard), account for wave action, making elevation alone insufficient for risk assessment. A property 10 feet above sea level in a VE zone might still face significant risk due to storm surges. In contrast, riverine zones focus on stillwater flooding, where elevation directly correlates with risk. For instance, a 10-foot elevation in a riverine AE zone could be safer than a similar elevation in a coastal VE zone. Understanding these distinctions ensures accurate risk evaluation and appropriate insurance coverage.

Descriptively, FEMA’s Letter of Map Amendment (LOMA) process allows property owners to challenge their flood zone designation if they believe their elevation is misclassified. For a property 10 feet above sea level, a LOMA could reclassify it from a high-risk to a low-risk zone, eliminating mandatory flood insurance requirements. This process requires a certified surveyor to provide elevation data, which FEMA reviews. Successfully obtaining a LOMA can save thousands in insurance premiums annually, making it a worthwhile investment for properties near the BFE threshold. However, FEMA’s scrutiny ensures only genuinely low-risk properties benefit, maintaining the integrity of the flood zone system.

Life, Death, and Dismemberment: Group Insurance Explained

You may want to see also

Explore related products

![]()

Premium cost factors for 10 feet elevation

Elevation plays a critical role in determining insurance premiums, particularly for properties near sea level. At 10 feet above sea level, a property’s risk profile shifts significantly compared to lower elevations. Insurers assess this height as a partial buffer against flooding, reducing the likelihood of damage from storm surges or high tides. However, it’s not a guarantee of safety, as severe weather events can still overwhelm this elevation. This nuanced risk assessment directly influences premium costs, with insurers balancing the reduced risk against the potential for catastrophic loss.

To understand premium cost factors at 10 feet elevation, consider the property’s location relative to flood zones. FEMA’s flood maps categorize areas based on risk, with zones like AE or VE indicating high-risk regions. A property at 10 feet elevation may fall just above the base flood elevation (BFE) in some areas, potentially lowering premiums. However, insurers also evaluate proximity to bodies of water, slope of the land, and historical flood data. For instance, a home 10 feet above sea level in a coastal area with a history of hurricanes will face higher premiums than one in a calmer inland region.

Another factor is the construction and mitigation measures of the property. Homes built to exceed the 10-foot elevation mark with features like raised foundations, flood vents, or waterproof materials can significantly reduce premiums. Insurers often offer discounts for properties adhering to stricter building codes or those with certified elevation certificates. For example, elevating mechanical systems above the base flood elevation can lower premiums by 20–30%, depending on the insurer. Investing in such measures not only enhances safety but also provides long-term savings on insurance costs.

Comparatively, properties at 10 feet elevation often fare better than those at lower levels but still face unique challenges. While they may avoid the highest-risk flood insurance categories, they remain vulnerable to heavy rainfall, rising water tables, or infrastructure failures. Premiums reflect this middle ground, typically costing 10–25% less than properties at 5 feet elevation but still higher than those at 20 feet or more. Policyholders can further reduce costs by bundling flood insurance with homeowners’ policies or opting for higher deductibles, though this requires careful consideration of out-of-pocket risk.

In conclusion, premium cost factors for properties at 10 feet elevation are shaped by location, construction, and historical risk data. While this elevation offers some protection, it’s not a silver bullet against flooding. Property owners can take proactive steps—such as obtaining elevation certificates, investing in flood-resistant features, and shopping for competitive policies—to optimize their insurance costs. Understanding these factors empowers homeowners to make informed decisions, balancing risk and affordability in flood-prone areas.

Renewing Your Bupa Insurance: A Step-by-Step Guide for Policyholders

You may want to see also

Frequently asked questions

Yes, properties at 10 feet above sea level are generally insurable, but coverage and rates may vary based on location, flood risk, and insurer policies.

Being 10 feet above sea level can reduce flood insurance premiums compared to lower elevations, but it depends on FEMA flood zone designations and historical flood data.

Not necessarily. Even at 10 feet above sea level, lenders may still require flood insurance if the property is in a high-risk flood zone or near water bodies.

Yes, standard homeowners insurance is typically available for properties at 10 feet above sea level, but it may not cover flood damage, requiring a separate flood insurance policy.