The question of whether $70 a month for health insurance is a lot depends on various factors, including individual financial situations, the cost of living in one's area, and the specific coverage provided by the insurance plan. For some, $70 might be a manageable expense, while for others, it could represent a significant financial burden. It's important to consider the overall value of the insurance, such as the deductible, copays, and the network of healthcare providers included. Additionally, comparing this cost to the potential out-of-pocket expenses without insurance can provide a clearer perspective on its affordability.

Explore related products

![Meal Planner: Weekly Menu Planner with Grocery List [ Softback * Large (8" x 10") * 52 Spacious Records & more * Carnival ] (Food Planners)](https://m.media-amazon.com/images/I/81jkEDeXl0L._AC_UY218_.jpg)

What You'll Learn

- Average Costs: Comparing $70 to typical monthly health insurance premiums for individuals and families

- Coverage Quality: Evaluating the benefits and coverage provided for $70 per month

- Subsidies and Assistance: Exploring potential subsidies or financial assistance options for health insurance

- Alternative Plans: Discussing other health insurance options that might offer better value or lower costs

- Personal Circumstances: Considering how personal factors, like age and health status, impact the affordability of $70 monthly premiums

![]()

Average Costs: Comparing $70 to typical monthly health insurance premiums for individuals and families

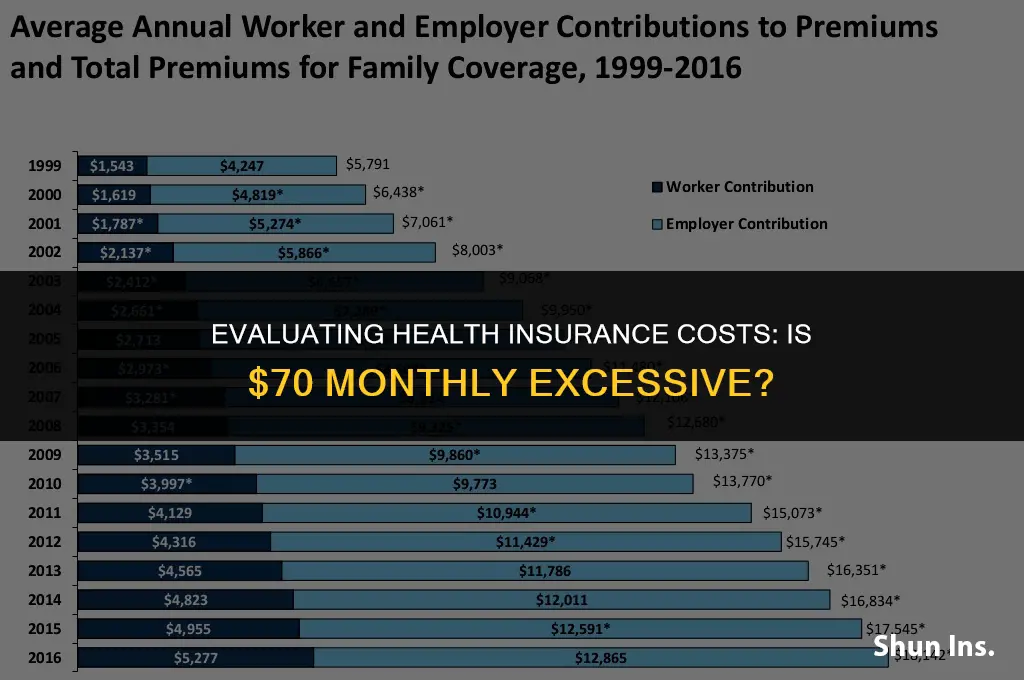

The average cost of health insurance can vary significantly based on several factors, including the type of plan, the insurance provider, and the geographic location of the insured individual or family. As of the latest data available, the average monthly premium for an individual health insurance plan in the United States is around $400, while the average for a family plan is approximately $1,000. Given these figures, a monthly premium of $70 would be considered quite low.

One way to contextualize the affordability of a $70 monthly premium is to compare it to the costs of other essential services. For instance, the average monthly cost of a gym membership is around $60, and the average cost of a streaming service subscription is about $15. In this light, $70 for health insurance could be seen as a reasonable expense, especially considering the potential benefits and protections it provides.

However, it's important to note that the value of a $70 health insurance plan would depend on the specific coverage and benefits included. Some plans with lower premiums may have higher deductibles, copays, or coinsurance, which could increase the overall cost of care. Additionally, plans with lower premiums might offer more limited provider networks or less comprehensive coverage, which could impact the quality of care available to the insured individual or family.

When evaluating the affordability of a $70 monthly health insurance premium, it's also crucial to consider the potential alternatives. For individuals who are eligible, Medicaid or other government-assisted programs might offer even lower premiums or no premiums at all. Furthermore, employer-sponsored health insurance plans often provide more affordable options, with average monthly premiums ranging from $100 to $300 for individuals and $300 to $700 for families.

In conclusion, while $70 a month for health insurance might seem like a lot to some, it's actually quite low compared to the average costs of individual and family plans in the United States. However, the true value of such a plan would depend on the specific coverage and benefits offered, as well as the individual or family's unique circumstances and needs.

Exploring Private Health Insurance Options in Denmark: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Coverage Quality: Evaluating the benefits and coverage provided for $70 per month

Evaluating the benefits and coverage provided for $70 per month requires a detailed analysis of the insurance plan's features. This includes examining the plan's deductible, copayments, coinsurance, and out-of-pocket maximum. Additionally, it's essential to consider the network of healthcare providers included in the plan, as well as any exclusions or limitations on coverage. By comparing these factors to other plans available at similar price points, individuals can determine whether the $70 per month plan offers adequate coverage for their healthcare needs.

One approach to evaluating coverage quality is to assess the plan's actuarial value, which represents the percentage of healthcare costs that the insurance company is expected to cover. Plans with higher actuarial values typically provide more comprehensive coverage, but may come with higher premiums. Another important consideration is the plan's drug formulary, which lists the medications covered under the plan. Individuals with chronic conditions or those who take multiple medications should carefully review the formulary to ensure that their necessary medications are included.

Furthermore, it's crucial to evaluate the plan's customer service and claims processing efficiency. A plan with a high level of customer satisfaction and a streamlined claims process can significantly enhance the overall experience for policyholders. Additionally, individuals should consider the plan's preventive care coverage, as many plans now offer free or low-cost preventive services such as annual check-ups, vaccinations, and screenings. By taking a comprehensive approach to evaluating coverage quality, individuals can make an informed decision about whether the $70 per month plan is a good value for their healthcare needs.

Profit Margins: Medical Insurance Companies' Performance

You may want to see also

Explore related products

![]()

Subsidies and Assistance: Exploring potential subsidies or financial assistance options for health insurance

Navigating the complex landscape of health insurance affordability can be daunting, but understanding potential subsidies and assistance options can significantly alleviate financial burdens. One such avenue is the Health Insurance Marketplace, established under the Affordable Care Act, which offers subsidies to individuals based on income levels. These subsidies can drastically reduce monthly premiums, making health insurance more accessible.

For instance, individuals earning up to 400% of the federal poverty level may qualify for premium tax credits. These credits can be applied directly to monthly premiums, reducing the overall cost. Additionally, cost-sharing reductions are available for those earning up to 250% of the federal poverty level, which can lower out-of-pocket expenses such as deductibles and copays.

Another option to consider is Medicaid expansion, available in many states, which provides health coverage to low-income adults. Eligibility criteria vary by state, but generally, individuals with incomes up to 138% of the federal poverty level may qualify. Furthermore, the Children's Health Insurance Program (CHIP) offers affordable health coverage for children in families that earn too much to qualify for Medicaid but still cannot afford private insurance.

Employer-sponsored health insurance is another potential source of assistance. Many employers offer health benefits as part of their compensation packages, which can include subsidies or contributions towards monthly premiums. It's essential to explore these options through your employer's human resources department.

Lastly, for those who are self-employed or do not have access to employer-sponsored insurance, health insurance cooperatives (co-ops) can be a viable alternative. Co-ops are member-owned, democratically governed organizations that aim to provide affordable health coverage to their members. By pooling resources and negotiating with healthcare providers, co-ops can offer competitive rates and subsidies to their members.

In conclusion, exploring various subsidies and assistance options can make health insurance more affordable and accessible. From federal subsidies through the Health Insurance Marketplace to state-specific programs like Medicaid expansion, and from employer-sponsored benefits to health insurance cooperatives, there are multiple avenues to consider when seeking to reduce monthly health insurance costs.

Does UCLA Medical Accept Medicare Insurance?

You may want to see also

Explore related products

![]()

Alternative Plans: Discussing other health insurance options that might offer better value or lower costs

If you're paying $70 a month for health insurance and wondering if there are better options, you're not alone. Many individuals and families are constantly seeking ways to reduce their healthcare costs without compromising on coverage. In this section, we'll explore alternative health insurance plans that might offer better value or lower costs, helping you make an informed decision about your healthcare.

One alternative to consider is a Health Savings Account (HSA) paired with a high-deductible health plan (HDHP). This option is particularly attractive for those who are generally healthy and don't require frequent medical attention. An HSA allows you to save money tax-free for qualified medical expenses, and the high-deductible plan typically comes with lower monthly premiums. However, it's essential to understand that this option may not be suitable for everyone, especially those with chronic conditions or high healthcare needs.

Another option to explore is a Flexible Spending Account (FSA), which is often offered by employers. An FSA allows you to set aside pre-tax dollars for qualified medical expenses, reducing your taxable income and, consequently, your overall healthcare costs. Unlike an HSA, an FSA is not portable and must be used within the plan year, so it's crucial to estimate your healthcare needs accurately to avoid losing unused funds.

For those who are self-employed or don't have access to employer-sponsored health insurance, a health insurance marketplace plan might be a viable alternative. These plans are available through state or federal exchanges and offer a range of coverage options to suit different needs and budgets. Depending on your income, you may also be eligible for subsidies to help lower your monthly premiums.

When evaluating alternative health insurance options, it's essential to consider factors beyond just the monthly premium. Take into account the plan's deductible, copayments, coinsurance, and out-of-pocket maximums. Additionally, ensure that the plan covers your essential healthcare needs, including prescription medications, preventive care, and any ongoing treatments or conditions.

In conclusion, while $70 a month for health insurance may seem like a significant expense, there are alternative plans available that could offer better value or lower costs. By carefully considering your healthcare needs and exploring options such as HSAs, FSAs, and marketplace plans, you can make an informed decision about your health insurance coverage and potentially save money in the process.

SSI and Health Insurance: Does It Count as Gross Income?

You may want to see also

Explore related products

![]()

Personal Circumstances: Considering how personal factors, like age and health status, impact the affordability of $70 monthly premiums

Age is a significant factor in determining the affordability of health insurance premiums. As individuals age, their health insurance costs tend to increase due to the higher likelihood of developing chronic conditions or requiring more medical care. For someone in their 20s or 30s, a $70 monthly premium might be quite manageable, representing a small fraction of their disposable income. However, for older adults, particularly those in their 50s or 60s, this same premium could be a substantial financial burden, especially if they are living on a fixed income or have other significant expenses.

Health status is another critical personal factor that impacts the affordability of health insurance. Individuals with pre-existing conditions or those who require frequent medical attention may find that their premiums are higher than those of healthier individuals. In some cases, people with serious health conditions might struggle to find affordable insurance at all, as insurers may view them as high-risk and charge exorbitant rates. For these individuals, a $70 monthly premium might seem relatively reasonable compared to the potential costs of medical care without insurance.

Income level and employment status also play a role in determining the affordability of health insurance premiums. Full-time employees often have access to employer-sponsored health insurance, which can significantly reduce their out-of-pocket costs. However, part-time workers, freelancers, or those who are self-employed may need to purchase individual health insurance policies, which can be more expensive. For someone earning a modest income, a $70 monthly premium could represent a significant portion of their budget, forcing them to make difficult choices between health insurance and other essential expenses.

Family size and composition can also influence the affordability of health insurance. Families with children may need to purchase more comprehensive policies to cover pediatric care, which can increase premiums. Additionally, families with multiple members may find that their total health insurance costs are higher, even if each individual's premium is relatively low. In such cases, a $70 monthly premium per person could add up quickly, becoming a substantial financial commitment for the household.

Ultimately, the affordability of a $70 monthly health insurance premium depends on a complex interplay of personal factors, including age, health status, income, employment, and family composition. For some individuals, this premium may be quite manageable, while for others, it could represent a significant financial strain. When evaluating the affordability of health insurance, it is essential to consider these personal circumstances and to shop around for policies that offer the best value and coverage for one's specific needs.

Exploring the Benefits of Supplemental Health Insurance: Is It Worth It?

You may want to see also

Frequently asked questions

The affordability of health insurance varies based on factors like age, location, and the type of plan. For some individuals, $70 a month might be reasonable, while for others, it could be considered expensive. It's essential to compare prices and benefits to determine if it's a good value for your specific situation.

Several factors can affect health insurance premiums, including your age, gender, location, health status, the type of plan you choose, and whether you qualify for subsidies. Additionally, lifestyle choices, such as smoking, can impact your rates.

Yes, there are several strategies to reduce health insurance costs. You can explore options like increasing your deductible, choosing a Health Savings Account (HSA) plan, or opting for a catastrophic plan if you're young and healthy. Additionally, maintaining a healthy lifestyle and taking advantage of preventive care can help lower your premiums.

When evaluating health insurance plans, consider the benefits that are most important to you. These may include coverage for doctor visits, prescription medications, mental health services, and preventive care. Additionally, check the plan's network to ensure your preferred healthcare providers are included and review the out-of-pocket costs associated with the plan.

To determine if $70 a month is a good deal for health insurance in your area, research the average premiums for similar plans in your region. You can use online tools or consult with a health insurance agent to compare prices and benefits. Additionally, consider your personal healthcare needs and budget to assess whether the plan is a good fit for you.