Guaranteed Asset Protection (GAP) insurance is an optional add-on coverage that can help drivers cover the difference between the financed amount owed on their car and its actual cash value (ACV) in the event of a total loss. GAP insurance is not a warranty but rather a form of supplemental car insurance that can be purchased separately or added to an existing auto insurance policy. It is designed to protect drivers from financial loss if their vehicle is stolen or deemed a total loss after an accident, by covering the gap between the amount owed on the car loan or lease and the vehicle's current market value.

| Characteristics | Values |

|---|---|

| What is it? | Guaranteed Asset Protection (GAP) insurance |

| Type | Optional, add-on coverage |

| When to get it? | When the loan or lease balance is higher than the market value of the vehicle |

| When to cancel it? | When the loan is paid off or the vehicle is sold |

| What does it cover? | The difference between the amount owed on a car and its actual cash value (ACV) or market value |

| What does it not cover? | Unpaid finance charges, warranty costs, balloon payments, deductibles, damage from a previous accident |

| Who is it for? | Drivers who owe more on their car loan than the car is worth, drivers whose car or lease loan requires GAP insurance |

| Cost | $200-$300 when purchased independently; $20-$40 per year when bundled with an existing policy |

Explore related products

What You'll Learn

- GAP insurance covers the difference between the value of your car and the loan amount

- It is optional and can be purchased from a dealer, lender, or insurer

- It is intended to cover theft or damage beyond repair

- It does not cover repairs, maintenance, or commercial use

- It is not the same as a warranty but can be purchased alongside one

![]()

GAP insurance covers the difference between the value of your car and the loan amount

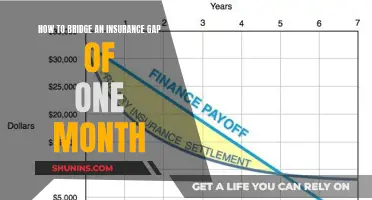

No, gap insurance is not a warranty. It is a type of auto insurance that covers the difference between the value of your car and the loan amount owed on it, in the event of a total loss. This "gap" can occur because cars depreciate quickly, sometimes by 10% in the first month of ownership.

Gap insurance is particularly useful if you owe more on your car loan than the car is worth. For example, if you owe $20,000 on your financing agreement, but due to depreciation, your car's actual cash value is only $15,000. If your car is completely written off as a result of an accident or theft, your car insurance policy will pay out $15,000. Gap insurance would cover the $5,000 "gap", i.e., the difference between the money you receive from the reimbursement and the amount you still owe on the car.

Gap insurance is not mandatory, but it might be required by your financing agreement. It is also a good idea for those who have made little or no down payment on their car, or who plan to drive in a way that might decrease its resale value quickly, such as taking many long road trips or exploring rough roads. Additionally, if you took out a car loan with a term longer than five years, gap insurance might be a good option.

The cost of gap insurance depends on your state, driving record, age, vehicle, and other factors. It can be purchased as an endorsement on your car insurance policy, or as separate coverage from the dealer.

Comp Insurance: Vehicle Protection

You may want to see also

Explore related products

![]()

It is optional and can be purchased from a dealer, lender, or insurer

Gap insurance is an optional form of protection that can be purchased at the same time as buying or leasing a new car. It can be purchased from a dealer, lender, or insurer. It is also known as Guaranteed Asset Protection (GAP) insurance.

When buying a car, a dealer or lender might offer you gap coverage. However, it is worth checking with your insurance agent to see if their company has a better deal. Gap products from a car dealer or bank may not be insurance, so it is important to read the information that comes with a bank or dealer gap product to know how to get help if you need it.

Gap insurance can also be purchased separately through a different provider, such as a bank or credit union. Most dealerships will offer gap coverage while negotiating financing, but they must wait two days before selling you the policy. This is to prevent buyers from feeling pressured into policies before they can research alternatives.

If you are considering buying gap insurance, it is worth noting that it is not required by any insurer or state. However, some leasing companies may require you to purchase it. Additionally, when purchasing a new car, some dealerships may automatically add gap insurance to your loan, but you can decline this coverage.

Update Your Vehicle Insurance Name

You may want to see also

Explore related products

![]()

It is intended to cover theft or damage beyond repair

Gap insurance is intended to cover theft or damage beyond repair. If your car is stolen and unrecovered, or if it is damaged beyond repair in an accident, gap insurance will cover the difference between the car's actual cash value and the amount still owed on the loan or lease. This is especially useful if the loan or lease balance is higher than the market value of the vehicle, which can often be the case in the early years of a vehicle's ownership.

For example, imagine your car is three years old and has an actual cash value of $20,000, but you still owe $25,000 in payments. If your car is stolen or written off in an accident, gap insurance will cover the $5,000 difference (minus your deductible). This can be a financial lifeline, as without gap insurance, you would be responsible for paying off the remaining loan or lease balance yourself.

Gap insurance is designed to protect you from being out of pocket in these situations. It ensures that you are not left with a large bill for a car that you can no longer drive. It bridges the gap between what your standard insurance will pay (the current market value of the vehicle) and what you actually owe on the vehicle.

It's important to note that gap insurance does not cover mechanical issues, engine failure, transmission failure, or any other type of repair. It also does not cover injuries, death, or funeral costs. Gap insurance is specifically for financial protection in the event of theft or total loss of your vehicle.

Florida's Vehicle Insurance Law Explained

You may want to see also

Explore related products

![]()

It does not cover repairs, maintenance, or commercial use

Gap insurance, or Guaranteed Asset Protection (GAP) insurance, is not a warranty and does not cover repairs, maintenance, or commercial use. It is an optional, add-on insurance product that covers the difference between the amount owed on a car loan and the car's actual cash value (ACV) in the event of a total loss or theft. This type of insurance is intended for drivers who owe more on their car loan than the car is worth.

While gap insurance can provide financial protection in the event of a total loss or theft, it does not cover repairs or maintenance. Repairs refer to the fixing or replacement of damaged or malfunctioning parts of a vehicle to restore it to its previous condition. Maintenance, on the other hand, involves routine servicing and upkeep of a vehicle to ensure its optimal performance and longevity. Gap insurance is not designed to cover these expenses.

Similarly, gap insurance does not extend to commercial use. Commercial use typically refers to using a vehicle for business or work-related purposes, such as transporting goods, providing transportation services, or travelling between different work locations. Gap insurance is designed for personal vehicle use and may not provide coverage for vehicles used primarily for commercial activities.

It is important to understand the limitations of gap insurance before purchasing it. While it can provide valuable financial protection in the event of a total loss or theft, it is not a comprehensive warranty that covers all aspects of vehicle ownership, use, and maintenance. Repairs, maintenance, and commercial use are generally excluded from the scope of gap insurance coverage.

To summarise, gap insurance is designed to protect against financial loss in the event of a total loss or theft of a vehicle, but it does not cover repairs, maintenance, or commercial use. As such, it is important for vehicle owners to carefully review the terms and conditions of their insurance policies to understand the specific inclusions and exclusions of their coverage.

Insurance Process for Wrecked Vehicles

You may want to see also

Explore related products

![]()

It is not the same as a warranty but can be purchased alongside one

Gap insurance, or Guaranteed Asset Protection insurance, is not the same as a warranty but can be purchased alongside one. It is an optional, additional coverage that can help drivers cover the difference between the financed amount owed on their car and its actual cash value (ACV) in the event of a covered incident where the car is declared a total loss.

Gap insurance is particularly useful for drivers who owe more on their car loan than the car is worth. This can occur when the down payment on the car was less than 20% or the loan is financed for 60 months or more. In these cases, the "gap" between the amount owed and the car's value can be significant, often thousands of dollars.

For example, let's say you bought a new car for $30,000 and you still owe $25,000 on your loan when you're involved in an accident. Your insurance company declares your vehicle a total loss and agrees to pay you the car's depreciated value, which is $20,000. With a deductible of $500, you would receive a check for $19,500, leaving you with a $5,500 gap to pay off your loan balance. If you had gap insurance, it would cover this difference, ensuring you don't have to pay out of pocket to cover the gap.

It's important to note that gap insurance is not the same as a warranty or regular car insurance. It only covers the difference between what you paid for your car and its value at the time of loss. It does not cover other costs such as interest on your loan, routine maintenance, repairs, or damage to other people's property. Additionally, gap insurance does not cover medical expenses resulting from an accident.

When considering gap insurance, it is essential to review the specific terms and conditions, as well as any exclusions or limitations, to ensure it meets your needs and provides the desired level of protection.

Red Alert: Are Your Wheels Covered?

You may want to see also

Frequently asked questions

Guaranteed Asset Protection (GAP) insurance is an optional product that covers the difference between the amount you owe on your auto loan and the amount the insurance company pays if your car is stolen or totaled.

GAP insurance covers the difference between what you owe on your car and what it is worth. You might need it if your car is worth less than what you owe on your car loan.

Cancel the policy when you owe less than your vehicle is worth. This usually takes about two years. Compare how much you owe on your loan with online car value guides.

The price of GAP insurance can vary. It can cost between $400 and $700 when wrapped into your loan by the dealer, and between $20 and $40 per year if you add it to your auto insurance policy.