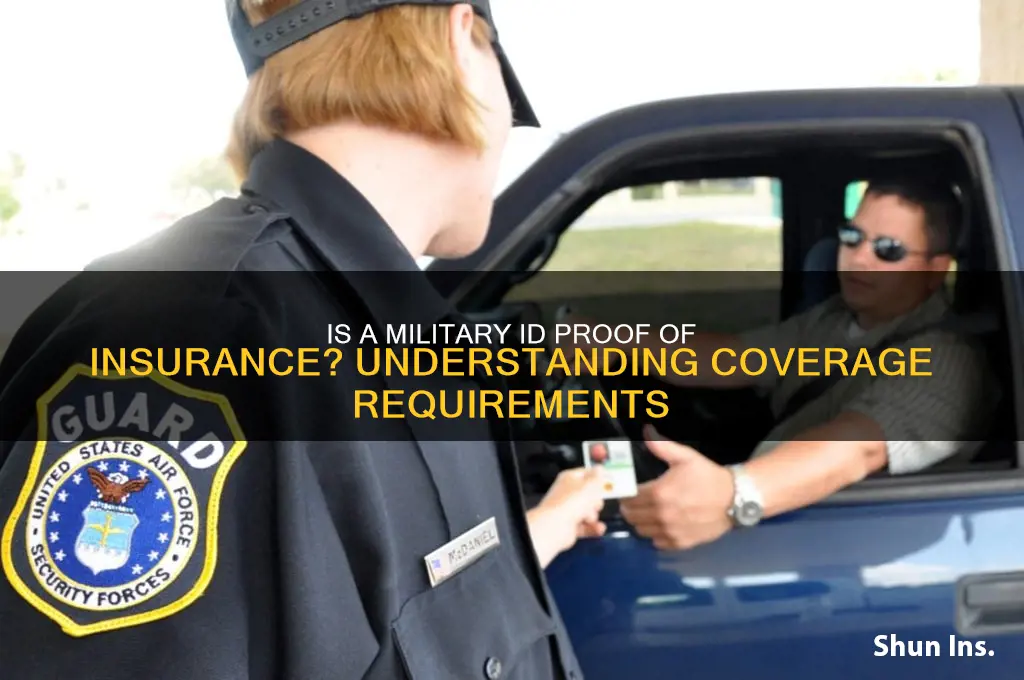

The question of whether a military ID serves as proof of insurance is a common one, particularly among service members and their families. While a military ID is a crucial form of identification that verifies an individual’s status in the armed forces, it does not inherently function as proof of insurance. Military personnel typically receive health coverage through TRICARE, but this is separate from the ID itself. For auto or other types of insurance, service members must carry specific documentation provided by their insurance provider, as a military ID alone does not meet legal or administrative requirements for proving insurance coverage. Understanding this distinction is essential to avoid confusion and ensure compliance with relevant laws and regulations.

| Characteristics | Values |

|---|---|

| Is a Military ID Proof of Insurance? | No, a military ID is not considered proof of insurance. |

| Purpose of Military ID | Identifies service members, grants access to military facilities, and verifies eligibility for benefits. |

| Proof of Insurance Requirements | Typically requires an insurance card, policy document, or digital proof from an insurance provider. |

| Legal Acceptance | Military IDs are not legally recognized as proof of insurance in most jurisdictions. |

| State-Specific Regulations | Some states may have unique rules, but generally, military IDs do not suffice for insurance verification. |

| Alternative Documents | Insurance cards, SR-22 forms (if required), or letters from insurance companies are accepted as proof. |

| Military-Specific Insurance | Military members often have access to specific insurance programs (e.g., USAA), but a military ID does not replace official insurance documentation. |

| Common Misconceptions | Many assume a military ID covers insurance needs, but it does not fulfill legal or administrative requirements for proof of insurance. |

Explore related products

What You'll Learn

- Military ID Coverage Limits: Does it meet state insurance requirements for vehicle or health coverage

- Acceptance by Authorities: Are military IDs recognized as valid proof of insurance by law enforcement

- Military Health Insurance: Does TRICARE or other military plans satisfy insurance proof needs

- State-Specific Rules: Do state laws accept military IDs as proof of insurance

- Alternative Documentation: What other documents can be used if military ID is insufficient

![]()

Military ID Coverage Limits: Does it meet state insurance requirements for vehicle or health coverage?

A military ID serves primarily as proof of service and eligibility for benefits, not as a substitute for insurance coverage. While it grants access to military healthcare and certain privileges, it does not inherently meet state insurance requirements for vehicle or health coverage. Understanding this distinction is crucial for service members and their families navigating civilian insurance mandates.

For vehicle insurance, states require proof of financial responsibility, typically in the form of a policy meeting minimum liability limits. A military ID does not fulfill this requirement, as it does not provide coverage for accidents, property damage, or bodily injury. Service members stationed in a new state must obtain a policy compliant with local laws, even if they have access to military healthcare. For example, Texas requires drivers to carry at least $30,000 in bodily injury liability per person, $60,000 per accident, and $25,000 in property damage liability. A military ID offers no such protection.

In the realm of health insurance, TRICARE, the military’s healthcare program, provides comprehensive coverage for active-duty members and their dependents. However, TRICARE may not meet the Affordable Care Act’s (ACA) minimum essential coverage standards in all cases, particularly for reservists or family members with specific needs. States like California and New York have additional health insurance mandates, and TRICARE’s coverage limits or exclusions could leave gaps. For instance, some states require coverage for specific services, such as mental health parity or maternity care, which TRICARE may not fully address for certain beneficiaries.

To ensure compliance, service members should verify their coverage against state requirements. For vehicle insurance, purchasing a policy from a private insurer is non-negotiable. For health insurance, while TRICARE often suffices, supplemental policies may be necessary to avoid penalties or gaps. Practical steps include reviewing state insurance laws, consulting a military benefits counselor, and comparing TRICARE benefits to ACA standards. Ignoring these steps could result in fines, denied claims, or inadequate protection during emergencies.

In conclusion, a military ID is not proof of insurance and does not satisfy state vehicle or health insurance requirements. Service members must proactively secure compliant coverage, leveraging TRICARE for health needs while supplementing with private policies where necessary. This dual approach ensures legal compliance and comprehensive protection, bridging the gap between military benefits and civilian mandates.

Permanent Life Insurance: Where to Get Covered for Life

You may want to see also

Explore related products

![]()

Acceptance by Authorities: Are military IDs recognized as valid proof of insurance by law enforcement?

Military IDs serve primarily as identification for service members, but their acceptance as proof of insurance by law enforcement is a nuanced issue. In most U.S. states, drivers are required to carry auto insurance and provide proof during traffic stops. While military IDs verify identity and affiliation, they do not inherently contain insurance information. Law enforcement officers typically look for documents explicitly stating insurance coverage, such as an insurance card or digital proof. Thus, relying solely on a military ID during a traffic stop could lead to citations if insurance proof is not readily available.

The confusion often arises from the misconception that military IDs grant special exemptions or privileges. However, traffic laws apply equally to all drivers, regardless of military status. Some states allow digital proof of insurance via smartphone apps, but a military ID does not substitute for these methods. Service members must still carry valid insurance documentation, just like civilian drivers. Failure to provide proper proof can result in fines, license suspension, or other penalties, even for those in uniform.

One exception worth noting is on military bases, where rules may differ. Base security personnel often require only a military ID for entry, and insurance checks are less common within these controlled environments. However, this does not extend to public roads or interactions with civilian law enforcement. Service members should not assume their military ID will suffice outside these specific contexts. Always carrying proof of insurance remains a legal requirement, regardless of military affiliation.

To avoid complications, service members should take proactive steps. First, ensure auto insurance coverage meets state minimum requirements. Second, keep a physical or digital copy of the insurance card in the vehicle at all times. Third, familiarize oneself with state-specific laws regarding acceptable forms of proof. For example, some states permit electronic proof, while others require physical documents. Staying informed and prepared minimizes the risk of misunderstandings during traffic stops.

In conclusion, military IDs are not recognized as valid proof of insurance by law enforcement. Their purpose is to verify military status, not insurance coverage. Service members must adhere to the same legal requirements as civilian drivers, carrying appropriate documentation to avoid penalties. By understanding these distinctions and taking practical precautions, military personnel can navigate traffic stops smoothly and comply with state laws.

Physician Assistants and Insurance Contracts: Understanding Coverage and Agreements

You may want to see also

Explore related products

![]()

Military Health Insurance: Does TRICARE or other military plans satisfy insurance proof needs?

Military ID cards are not proof of insurance, but they are key to accessing TRICARE and other military health plans. These plans, designed for active-duty service members, retirees, and their families, provide comprehensive medical coverage that often exceeds civilian insurance requirements. However, when asked for proof of insurance—whether for vehicle registration, certain state mandates, or other purposes—a military ID alone won’t suffice. Instead, beneficiaries must obtain official documentation from TRICARE or their specific military health plan to demonstrate compliance with insurance laws.

TRICARE, the primary health care program for the military, offers multiple plans tailored to different groups, such as TRICARE Prime, Select, and Reserve Select. Each plan provides proof of coverage through enrollment documents, benefit summaries, or official letters. For instance, active-duty members can request a "Certificate of Coverage" from their installation’s TRICARE office, while retirees may access their proof via the TRICARE website or by contacting their regional contractor. These documents explicitly state the policyholder’s name, coverage dates, and scope of benefits, satisfying most proof-of-insurance requirements.

One common misconception is that a military ID card, which grants access to military treatment facilities and TRICARE, automatically serves as proof of insurance. This confusion arises because the ID card is often used interchangeably with health care access. However, states and agencies typically require formal documentation that outlines the specifics of the insurance plan. For example, a TRICARE beneficiary registering a vehicle in a state with mandatory auto insurance laws would need to provide a TRICARE enrollment letter, not just their military ID, to prove they meet the state’s health insurance criteria.

To ensure compliance, military personnel and their families should proactively gather proof of insurance documents. Active-duty members can visit their local TRICARE service center or log into the TRICARE Beneficiary Web Enrollment portal to download enrollment verification. Retirees and family members may use the TRICARE website’s "Proof of Coverage" tool or contact their regional contractor for assistance. Additionally, some states accept the Department of Defense Form 1173 (Uniformed Services Identification and Privilege Card) as supplementary proof, but this varies by jurisdiction, so verifying local requirements is essential.

In summary, while military health plans like TRICARE provide robust coverage, a military ID card alone does not meet proof-of-insurance needs. Beneficiaries must obtain official documentation from their specific plan to comply with state or agency mandates. By understanding the distinction between access to care and proof of coverage, military families can avoid complications and ensure they meet all legal requirements. Proactive steps, such as downloading enrollment letters or contacting TRICARE representatives, are simple yet effective ways to stay prepared.

Understanding EOI: A Comprehensive Guide to Evidence of Insurability

You may want to see also

Explore related products

![]()

State-Specific Rules: Do state laws accept military IDs as proof of insurance?

Military IDs serve primarily as verification of service member status, not as proof of insurance. However, state laws vary widely in their acceptance of such documents for insurance verification purposes. In states like Texas and Florida, law enforcement officers may accept military IDs during traffic stops as a secondary form of identification but still require valid insurance documentation. Conversely, states like California and New York strictly enforce the presentation of official insurance cards or digital proofs, leaving no room for military IDs as substitutes. Understanding these state-specific rules is crucial for military personnel to avoid legal complications.

For military families relocating across state lines, navigating these discrepancies can be particularly challenging. Some states, such as North Carolina, offer grace periods for service members to update their insurance documentation after moving, while others, like Illinois, demand immediate compliance. To mitigate confusion, military personnel should consult their installation’s legal office or JAG (Judge Advocate General) for state-specific guidance. Additionally, maintaining a digital copy of insurance documents on a smartphone can provide quick access during traffic stops, regardless of state regulations.

A comparative analysis reveals that states with large military populations, such as Virginia and Georgia, often adopt more flexible policies to accommodate service members. For instance, Virginia allows military IDs to expedite verification processes in certain situations, though not as a standalone proof of insurance. In contrast, states with smaller military footprints, like Vermont or Oregon, adhere strictly to standardized insurance documentation requirements. This disparity highlights the need for federal and state collaboration to streamline policies for military families.

Practical tips for service members include keeping a physical insurance card in the vehicle at all times, even if digital proofs are permitted. In states where military IDs might be accepted as supplementary identification, carrying a copy of the state’s insurance laws can help clarify misunderstandings with law enforcement. Finally, enrolling in military-specific insurance programs, such as USAA, often provides additional resources and support tailored to navigating state-specific regulations. Awareness and preparation are key to avoiding penalties and ensuring compliance.

WSL Pension and Insurance: What Benefits Do Surfers Receive?

You may want to see also

Explore related products

![]()

Alternative Documentation: What other documents can be used if military ID is insufficient?

Military ID cards primarily verify service affiliation, not insurance coverage. While they grant access to military healthcare, they lack details like policy numbers, provider names, or coverage limits. When proof of insurance is required—for instance, in civilian contexts like car rentals or medical appointments—alternative documentation becomes essential.

Step 1: Verify Insurance Through Official Channels

Contact your military branch’s insurance office (e.g., TRICARE for active-duty members) to request a Certificate of Coverage. This document explicitly states policy details, including effective dates and covered individuals. For dependents, ensure their enrollment is up-to-date in the Defense Enrollment Eligibility Reporting System (DEERS), as this directly ties to insurance eligibility.

Step 2: Leverage Digital Tools

Most military insurance programs offer online portals (e.g., TRICARE’s *www.tricare.mil*) where beneficiaries can download digital proof of coverage. Screenshots or printed summaries from these portals often suffice for civilian entities. For added credibility, include the portal’s URL and your name/policy number in the document.

Step 3: Cross-Reference with Civilian Requirements

Civilian entities may demand specific formats. For example, car rental companies typically require a Declaration Page, while medical providers may accept an insurance card. If military-issued documents don’t align, request a customized letter from your insurance provider detailing coverage in the required format.

Caution: Avoid Common Pitfalls

Never rely solely on verbal confirmation of coverage. Always carry physical or digital copies of supplementary documents. Be wary of outdated information—insurance policies can change with deployments, separations, or retirements. Verify details annually or after significant life events.

While military ID cards are indispensable for service-related purposes, they’re insufficient for insurance verification. By proactively securing alternative documents—certificates, digital summaries, or customized letters—military personnel and their families can navigate civilian systems seamlessly. Preparation ensures compliance and avoids delays, whether renting a vehicle or accessing healthcare.

Variable Life Insurance: Death Benefit Guaranteed?

You may want to see also

Frequently asked questions

No, a military ID is not proof of insurance. It serves as identification for military personnel but does not provide information about insurance coverage.

While a military ID indicates eligibility for military health benefits (e.g., TRICARE), it is not a standalone proof of insurance. You may need additional documentation to verify coverage.

No, a military ID does not replace a car insurance card. You must carry a separate proof of auto insurance as required by state laws.

A military ID alone is not sufficient to enroll in civilian insurance plans. You will need additional documentation, such as proof of eligibility or coverage details.

No, a military ID does not prove life insurance coverage. Military members may have Servicemembers' Group Life Insurance (SGLI), but the ID itself does not serve as proof.

![Ashlin Genuine Leather Double ID Holder. Drivers License|MetroPass|Double Photos Holder| Black [7503-07-01]](https://m.media-amazon.com/images/I/81aPU95VEUL._AC_UL320_.jpg)