Medicare is a health insurance program for people aged 65 and over, and younger people with disabilities or specific health issues. Medicare Supplement Insurance, or Medigap, is extra insurance that helps pay for out-of-pocket costs in Original Medicare. Medigap is a type of secondary insurance, but not all secondary insurance is Medigap. Secondary insurance can also include other types of insurance, such as dental and vision, gap insurance, or disability insurance. The order of payment for these different insurance types is called coordination of benefits, with the primary payer paying first, and the secondary payer covering the remaining balance.

| Characteristics | Values |

|---|---|

| Primary payer | Pays up to the limit of its coverage |

| Secondary payer | Pays only if there are costs the primary insurance didn't cover |

| Medicare Supplement Insurance (Medigap) | Extra insurance to help pay your share of out-of-pocket costs in Original Medicare |

| Medigap policies | Generally do not cover long-term care, vision, dental, hearing aids, private-duty nursing, or prescription drugs |

| Medicare Secondary Payer (MSP) insurance | Occurs when Medicare is the next payer to another insurance company paying first or "primary" |

Explore related products

What You'll Learn

- Medicare Supplement Insurance (Medigap) is extra insurance to help pay your share of costs

- Original Medicare is primary to a Medicare Supplement plan

- Medicare Secondary Payer (MSP) insurance

- Secondary insurance can be a variety of insurance options

- Medicare Supplement plans are beneficial to protect from unexpected medical expenses

![]()

Medicare Supplement Insurance (Medigap) is extra insurance to help pay your share of costs

Medicare Supplement Insurance, also known as Medigap, is additional insurance that can be purchased from a private health insurance company to cover out-of-pocket costs in Original Medicare. Typically, individuals need to have Original Medicare, which includes Part A (Hospital Insurance) and Part B (Medical Insurance), before they can purchase a Medigap policy. Medigap policies help cover an individual's share of costs in Original Medicare, which may include deductibles, copayments, and coinsurance.

Medigap policies are standardized, and in most states, they are named by letters, such as Plan G or Plan K. The benefits offered by each lettered plan are the same, regardless of the insurance company selling it. The only difference between policies with the same letter sold by different companies is the price. It is important to note that Medigap policies generally do not cover long-term care, vision, dental, hearing aids, private-duty nursing, or prescription drugs. Additionally, if an individual is under 65, they may face challenges in purchasing a Medigap policy or may have to pay higher premiums.

Medigap functions as supplemental insurance, which is distinct from secondary insurance. Supplemental insurance is an additional form of insurance that helps cover costs not fully paid by the primary insurance. In the context of Medicare, the primary payer covers the costs up to the limits of its coverage, and then the remaining balance is sent to the supplemental insurance company for further processing and possible payment. This process is known as "coordination of benefits." On the other hand, secondary insurance, in the context of Medicare, refers to situations where Medicare itself becomes the secondary payer after another insurance company has paid as the primary payer. This scenario is often referred to as Medicare Secondary Payer (MSP) insurance.

Understanding the difference between supplemental and secondary insurance is crucial for coordinating benefits and ensuring that medical bills are sent to the correct payer to avoid delays in payment. Medicare beneficiaries should inform their doctors and healthcare providers if they have additional coverage, whether it be supplemental insurance, like Medigap, or secondary insurance from another source, to facilitate accurate billing and payment processes.

Getting Medical Insurance for Your Children: A Guide

You may want to see also

Explore related products

![]()

Original Medicare is primary to a Medicare Supplement plan

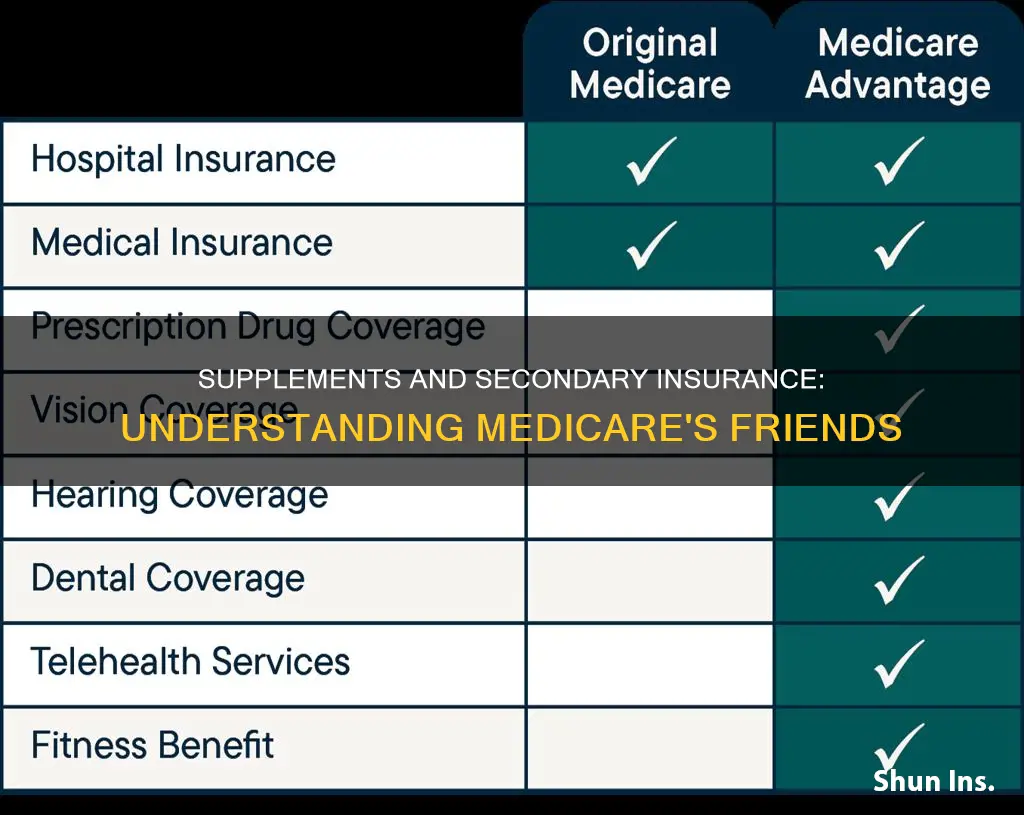

When you get a covered service, Medicare pays part of the cost, and you pay your share. Original Medicare consists of Part A (Hospital Insurance) and Part B (Medical Insurance). You can choose to get your health coverage through Original Medicare or Medicare Advantage. Medicare Advantage is an alternative to Original Medicare, and in many cases, you can only use doctors who are in the plan's network.

Medicare Supplement Insurance, also known as Medigap, is extra insurance you can buy from a private company to help pay your share of costs in Original Medicare. Medigap policies do not cover long-term care, vision, dental, hearing aids, private-duty nursing, or prescription drugs. Generally, you need to have Part A and Part B to buy a Medigap policy.

Medigap is a supplement to Original Medicare coverage. You can either buy Medigap or enroll in a Medicare Advantage Plan, but you cannot have both. If you want to switch to Original Medicare and buy a Medigap policy, you need to contact your Medicare Advantage Plan to see if you can disenroll.

Medigap policies are standardized, and in most states, they are named by letters, like Plan G or Plan K. The benefits in each lettered plan are the same, no matter the insurance company. The price is the only difference between policies with the same letter sold by different companies.

Living with HIV: Getting Medical Insurance Coverage

You may want to see also

Explore related products

![]()

Medicare Secondary Payer (MSP) insurance

The concept of MSP arose from legislation passed by Congress in 1980, which aimed to shift costs from Medicare to appropriate private sources of payment. This legislation ensured that Medicare does not pay for items and services that certain health insurance or coverage is primarily responsible for. The MSP provisions apply when Medicare is not the beneficiary's primary health insurance coverage.

In practice, this means that the primary payer covers costs up to the limits of its coverage, and then the remaining balance is sent to the secondary payer, which may be Medicare. If the secondary payer does not cover the remaining balance, the beneficiary may be responsible for the remaining costs.

It's important to note that Medicare can also be the primary payer in certain instances, such as for beneficiaries who are not covered by other types of health insurance or coverage. Additionally, federal law regarding MSP takes precedence over state laws and private contracts.

Becoming a Medical Insurance Agent in India: A Guide

You may want to see also

Explore related products

![]()

Secondary insurance can be a variety of insurance options

Medicare is a health insurance programme for people over 65 or with specific disabilities. It is primarily funded by the US federal government. Medicare consists of Part A (Hospital Insurance) and Part B (Medical Insurance). Once you've signed up for these two parts, you can choose how you get your health coverage. There are two main ways to get your Medicare coverage: Original Medicare and Medicare Advantage.

Supplemental insurance, or Medigap, is extra insurance that can be purchased from a private company to help pay your share of out-of-pocket costs in Original Medicare. Medigap policies do not cover long-term care, vision, dental, hearing aids, private-duty nursing, or prescription drugs.

The order of payment is called "coordination of benefits". If the secondary payer doesn't cover the remaining balance, the patient may be responsible for the remaining costs. Medicare may make a conditional payment if the primary payer does not pay promptly, and then later recover any payments the primary payer should have made.

Affording Medical Insurance: Strategies for Financial Planning

You may want to see also

Explore related products

![]()

Medicare Supplement plans are beneficial to protect from unexpected medical expenses

Medicare Supplement Insurance, also known as Medigap, is extra insurance provided by private companies to help cover out-of-pocket costs in Original Medicare. Medigap policies help pay your share of costs, such as copayments and coinsurance, that are not covered by Original Medicare (Part A and Part B). These policies are particularly beneficial for protecting against unexpected medical expenses, as they provide additional coverage for hospitalization, skilled nursing facility care, and hospice care.

For example, Medicare Supplement plans can pay your daily copayments for hospitalization expenses from the 61st to the 90th day of the Medicare benefit period. They can also cover the Medicare Part A coinsurance for an additional 365 days after Medicare benefits end. This extended coverage can provide significant financial relief in the event of prolonged or unexpected hospital stays.

Medigap policies also offer benefits for skilled nursing facility care. They may pay the copayments or coinsurance for post-hospital skilled nursing care, which can be crucial for individuals requiring extended recovery or rehabilitation. Additionally, some plans cover hospice care, including outpatient pain medication copayments and inpatient respite care coinsurance.

It's important to note that Medigap policies do not cover all expenses. They generally do not cover long-term care, such as nursing home care, vision, dental, hearing aids, private-duty nursing, or prescription drugs. However, some Medigap policies offer coverage for unexpected expenses when travelling outside the U.S., which can provide peace of mind during international travel.

Medicare Supplement plans are beneficial for individuals seeking protection from unexpected medical expenses. They fill the gaps in Original Medicare coverage, providing additional financial support for hospitalization, skilled nursing care, and hospice services. By purchasing a Medigap policy, individuals can reduce their financial risk and gain peace of mind, knowing that they have extra coverage for unexpected medical situations.

Young Adults: Uninsured and Unprotected

You may want to see also

Frequently asked questions

Medicare Supplement Insurance (Medigap) is extra insurance that can be purchased from a private company to help pay your share of costs in Original Medicare.

Secondary insurance for Medicare helps reduce your out-of-pocket costs. It is a variety of insurance options that extend your primary form of coverage.

The insurance that pays first (primary payer) pays up to the limits of its coverage. The insurance that pays second (secondary payer) pays if there are remaining costs that the primary insurance didn't cover.

Yes, Medigap is a type of secondary insurance. It is always secondary to Original Medicare, as it covers the remaining costs after Medicare pays first.