The Affordable Care Act (ACA) has revolutionized healthcare access in the United States, but understanding its intricacies can be complex. One key aspect that often confuses individuals is how ACA health insurance subsidies are calculated. The question of whether these subsidies are based on gross or net income is crucial for determining eligibility and the level of financial assistance one can receive. In this article, we'll delve into the specifics of ACA subsidy calculations, clarifying the role of income in determining health insurance costs under the ACA.

Explore related products

What You'll Learn

- Gross Income vs. Net Income: Understanding the difference between gross and net income is crucial for ACA eligibility

- ACA Subsidy Calculation: Subsidies are based on income, but whether gross or net income is used can affect the amount

- Tax Credits and Income: ACA tax credits are tied to income levels, and the type of income used can impact credit amounts

- Eligibility Thresholds: ACA eligibility thresholds vary by state and are influenced by whether gross or net income is considered

- Impact on Premiums: The choice between gross and net income can significantly affect ACA premiums and out-of-pocket costs

![]()

Gross Income vs. Net Income: Understanding the difference between gross and net income is crucial for ACA eligibility

Understanding the difference between gross and net income is crucial when determining eligibility for the Affordable Care Act (ACA). Gross income refers to the total amount of money earned before taxes and other deductions are taken out. This includes wages, salaries, tips, bonuses, and any other form of compensation. On the other hand, net income is the amount of money left after all deductions, such as federal and state taxes, social security, and Medicare, have been subtracted from the gross income.

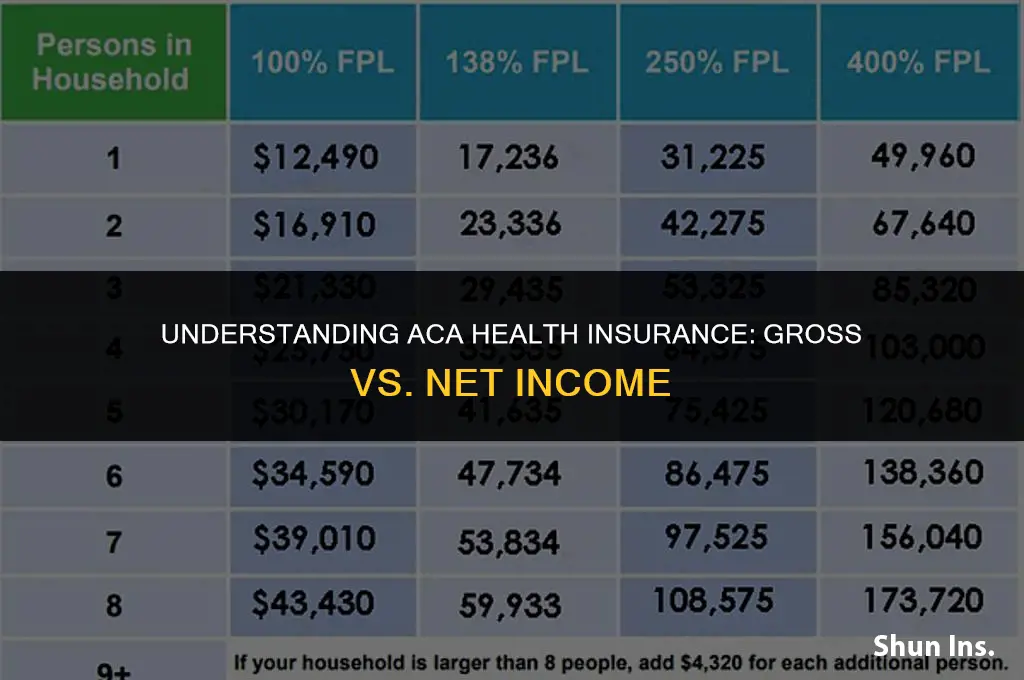

When it comes to ACA eligibility, the distinction between gross and net income is significant because the ACA uses a percentage of the federal poverty level (FPL) to determine who qualifies for subsidies and Medicaid expansion. This percentage is based on the modified adjusted gross income (MAGI), which is essentially the gross income with some adjustments. For example, if an individual's MAGI is below 138% of the FPL, they may be eligible for Medicaid expansion in states that have adopted it. Conversely, if their MAGI is between 100% and 400% of the FPL, they may qualify for premium tax credits to help pay for private insurance.

It's important to note that not all deductions are considered when calculating MAGI. For instance, the standard deduction or itemized deductions on a tax return are not taken into account. Additionally, certain types of income, such as Social Security benefits and some types of disability benefits, are excluded from MAGI calculations. This means that individuals who receive these types of income may have a lower MAGI than their gross income would suggest, potentially making them eligible for ACA subsidies.

To accurately determine ACA eligibility, individuals must carefully consider their gross income, net income, and MAGI. This involves understanding which types of income are included in each category and which deductions are applicable. By doing so, individuals can ensure they are correctly assessing their eligibility for ACA benefits and making informed decisions about their health insurance options.

AEW Wrestlers' Health Insurance: Coverage, Benefits, and Wellness Explained

You may want to see also

Explore related products

![]()

ACA Subsidy Calculation: Subsidies are based on income, but whether gross or net income is used can affect the amount

The Affordable Care Act (ACA) subsidies are a crucial component of the healthcare law, designed to make health insurance more affordable for millions of Americans. However, understanding how these subsidies are calculated can be complex, particularly when it comes to determining whether gross or net income is used. This distinction is vital because it can significantly impact the amount of financial assistance an individual or family receives.

In general, ACA subsidies are based on an individual's or family's modified adjusted gross income (MAGI). MAGI is a measure of income that includes most types of income, such as wages, salaries, tips, and investment income, but excludes certain items like Social Security benefits and tax-exempt interest. The reason MAGI is used instead of gross income is to provide a more accurate picture of an individual's or family's financial situation, as it takes into account certain deductions and exclusions that can reduce taxable income.

However, there are situations where net income might be considered. For example, if an individual or family has significant deductions or adjustments that are not reflected in their MAGI, such as high medical expenses or contributions to a Health Savings Account (HSA), their net income might be a better indicator of their ability to afford health insurance. In such cases, the ACA allows for some flexibility in determining the appropriate income measure to use for subsidy calculation.

One important note is that the ACA subsidy calculation is based on the income of all members of the household, not just the primary breadwinner. This means that the combined income of spouses, children, and other dependents must be considered when determining eligibility for subsidies. Additionally, the subsidy amount is not fixed and can vary depending on factors such as the size of the household, the ages of the members, and the cost of health insurance in the area where they live.

To further complicate matters, the ACA subsidy calculation is subject to annual changes based on inflation and other economic factors. This means that individuals and families must re-evaluate their eligibility and subsidy amount each year during the open enrollment period. Failure to do so could result in receiving too much or too little financial assistance, which could have significant financial consequences.

In conclusion, while ACA subsidies are generally based on modified adjusted gross income, there are circumstances where net income might be considered. Understanding the nuances of the subsidy calculation process is essential for individuals and families who rely on these financial assistance programs to afford health insurance. By staying informed about the latest changes and seeking guidance from qualified professionals, Americans can ensure they receive the appropriate level of support to maintain their health coverage.

Best Medical Insurance Options via Mass Health

You may want to see also

Explore related products

![]()

Tax Credits and Income: ACA tax credits are tied to income levels, and the type of income used can impact credit amounts

ACA tax credits are directly linked to an individual's income, which plays a pivotal role in determining the amount of financial assistance they can receive. The type of income considered for these credits can significantly impact the final credit amount, making it essential to understand the nuances of income calculation under the ACA.

The ACA uses a specific definition of income, known as Modified Adjusted Gross Income (MAGI), to determine eligibility and credit amounts. MAGI is calculated by taking an individual's Adjusted Gross Income (AGI) and adding back certain deductions and exclusions, such as the foreign earned income exclusion and the student loan interest deduction. This means that MAGI can be higher than AGI, potentially affecting the tax credit calculation.

For individuals who are self-employed, the calculation of MAGI can be more complex. Self-employed individuals must report their net business income on their tax return, which is calculated by subtracting business expenses from gross business receipts. However, for ACA purposes, self-employed individuals may need to estimate their MAGI based on their expected business income and expenses for the year.

It's also important to note that ACA tax credits are reconciled on an individual's tax return, meaning that any overpayment or underpayment of credits during the year must be accounted for. This reconciliation process can be affected by changes in income throughout the year, such as a job change or a significant increase in income.

Understanding the relationship between income and ACA tax credits is crucial for individuals to maximize their financial assistance and avoid potential penalties. By carefully considering the type of income used in the calculation and staying aware of any changes in income throughout the year, individuals can better navigate the complexities of ACA tax credits and ensure they receive the appropriate amount of assistance.

Unemployed and Uninsured: Do Jobless Individuals Need Health Coverage?

You may want to see also

Explore related products

![]()

Eligibility Thresholds: ACA eligibility thresholds vary by state and are influenced by whether gross or net income is considered

The Affordable Care Act (ACA) eligibility thresholds are a critical component in determining who qualifies for health insurance subsidies. These thresholds vary significantly by state, reflecting the federalist approach to healthcare policy in the United States. Each state has the autonomy to expand Medicaid under the ACA, which influences the eligibility criteria for residents.

One of the key factors affecting ACA eligibility is whether gross or net income is considered. Gross income refers to the total amount earned before taxes and deductions, while net income is the amount remaining after these deductions. States that have expanded Medicaid typically use gross income to determine eligibility, aligning with the federal poverty level guidelines. This approach ensures that individuals with lower incomes, who may have limited tax liabilities, are not unfairly penalized.

In contrast, states that have not expanded Medicaid often rely on net income calculations. This can result in a situation where individuals with similar gross incomes may have different net incomes due to varying tax obligations, potentially affecting their eligibility for ACA subsidies. For example, a person with a gross income of $30,000 in a state that uses net income might have a net income of $25,000 after taxes, which could place them below the eligibility threshold for subsidies.

The variation in eligibility thresholds also highlights the importance of understanding state-specific policies when navigating the ACA marketplace. Individuals may find that they qualify for subsidies in one state but not in another, based solely on the income calculation method used. This underscores the need for a nuanced approach to healthcare policy, one that takes into account the diverse economic circumstances of residents across different states.

In conclusion, the ACA eligibility thresholds are a complex interplay of federal and state policies, with the choice between gross and net income calculations playing a significant role in determining who qualifies for health insurance subsidies. This variation emphasizes the importance of state-specific knowledge and the need for a tailored approach to healthcare policy that addresses the unique needs of each state's population.

Extending Health Coverage: A Guide to COBRA Continuation Options

You may want to see also

![]()

Impact on Premiums: The choice between gross and net income can significantly affect ACA premiums and out-of-pocket costs

The Affordable Care Act (ACA) has revolutionized the healthcare landscape in the United States, providing millions of Americans with access to health insurance. However, the choice between gross and net income can have a profound impact on ACA premiums and out-of-pocket costs, affecting the affordability and accessibility of healthcare for many individuals and families.

Gross income refers to the total amount of money earned before taxes and other deductions, while net income is the amount remaining after these deductions. When applying for ACA health insurance, individuals must provide their projected gross income for the upcoming year. This figure is used to determine the premium tax credit, which helps offset the cost of insurance premiums.

The difference between gross and net income can lead to significant variations in premium costs. For instance, if an individual's gross income is relatively high, they may not qualify for a premium tax credit or may receive a smaller credit than if their net income were considered. This can result in higher out-of-pocket costs for insurance premiums. Conversely, if an individual's net income is lower due to deductions such as student loan interest or alimony payments, they may qualify for a larger premium tax credit, reducing their overall healthcare expenses.

Furthermore, the choice between gross and net income can also impact the cost-sharing reductions (CSRs) that help lower out-of-pocket costs for deductibles, copays, and coinsurance. CSRs are based on a percentage of the federal poverty level (FPL), and the gross income is used to determine eligibility. Individuals with higher gross incomes may not qualify for CSRs, leading to increased out-of-pocket expenses when utilizing healthcare services.

To mitigate the impact of gross income on ACA premiums and out-of-pocket costs, individuals can consider strategies such as maximizing tax deductions and credits, contributing to retirement accounts, or exploring health savings accounts (HSAs) or flexible spending accounts (FSAs). Additionally, understanding the nuances of the ACA and seeking guidance from a qualified healthcare professional can help individuals make informed decisions about their health insurance options.

In conclusion, the choice between gross and net income is a critical factor in determining ACA premiums and out-of-pocket costs. By understanding the implications of this choice and exploring strategies to optimize their income, individuals can make healthcare more affordable and accessible under the ACA.

Understanding Ophthalmology Coverage: What Your Health Insurance May Include

You may want to see also

Frequently asked questions

ACA health insurance subsidies are based on your modified adjusted gross income (MAGI), which is a measure of your income after certain deductions and exclusions.

The ACA uses your tax return information from the previous year to determine your income for subsidy purposes. If you're applying for coverage during the open enrollment period, the income information you provide on your application will be used.

Yes, if your income changes significantly during the year, you should report the change to the health insurance marketplace. This is because your subsidy amount may need to be adjusted based on your new income level.