Health insurance is a critical aspect of modern healthcare systems, providing financial protection against medical expenses. However, the accessibility and affordability of health insurance can vary significantly based on an individual's income level. In many countries, health insurance is closely tied to employment, with employers often subsidizing premiums for their employees. This can create disparities in access to healthcare, as those with lower incomes or without employer-sponsored insurance may struggle to afford adequate coverage. Furthermore, government-funded health insurance programs, such as Medicaid in the United States, are designed to assist low-income individuals, but eligibility criteria and coverage levels can differ by state or region. Understanding the relationship between income and health insurance is essential for policymakers and healthcare advocates working to improve equitable access to healthcare services.

| Characteristics | Values |

|---|---|

| Definition | Health insurance income is based on the premiums paid by individuals or employers for health coverage. |

| Types of Income | Includes premiums from private health insurance, Medicaid, Medicare, and other government-sponsored health programs. |

| Taxation | Health insurance premiums are often tax-deductible for individuals and businesses. |

| Regulation | Health insurance income is subject to state and federal regulations, including the Affordable Care Act (ACA). |

| Market Dynamics | The health insurance market is competitive, with multiple providers offering various plans and coverage options. |

| Consumer Choice | Individuals can choose from a range of health insurance plans based on their needs, budget, and preferences. |

| Provider Networks | Health insurance providers often have networks of healthcare providers, which can influence the cost and quality of care. |

| Cost Factors | Premiums can vary based on factors such as age, health status, location, and the level of coverage provided. |

| Benefits | Health insurance provides financial protection against high medical costs and ensures access to necessary healthcare services. |

| Challenges | The complexity of health insurance plans and the variability in coverage can make it difficult for consumers to understand and compare options. |

| Trends | There is a growing trend towards consumer-driven health care, with more emphasis on transparency and cost-sharing. |

| Future Outlook | The health insurance industry is expected to continue evolving, with potential changes in regulations, market dynamics, and consumer preferences. |

Explore related products

What You'll Learn

- Sliding Scale Premiums: Adjusting health insurance costs based on income to ensure affordability

- Subsidies and Assistance: Government aid to help low-income individuals afford health insurance

- Income-Based Eligibility: Qualification for certain health plans or benefits dependent on income level

- Premium Tax Credits: Tax incentives to reduce the cost of health insurance premiums

- Medicaid Expansion: Extending Medicaid coverage to more low-income adults under the Affordable Care Act

![]()

Sliding Scale Premiums: Adjusting health insurance costs based on income to ensure affordability

Sliding scale premiums are a mechanism used in health insurance to adjust costs based on an individual's income, ensuring that coverage remains affordable for people across different economic brackets. This approach is particularly relevant in discussions about income-based health insurance, as it directly ties the cost of premiums to the policyholder's financial capacity. By doing so, sliding scale premiums aim to make health insurance more accessible and equitable.

The implementation of sliding scale premiums typically involves a tiered system where individuals are categorized based on their income levels. Each tier corresponds to a different premium rate, with lower-income individuals paying less and higher-income individuals paying more. This system is designed to reduce the financial burden on those who might otherwise struggle to afford health insurance, while still maintaining a level of cost-sharing that encourages responsible use of healthcare services.

One of the key benefits of sliding scale premiums is that they can help to mitigate the impact of income disparities on access to healthcare. By making health insurance more affordable for lower-income individuals, this approach can contribute to improved health outcomes and reduced healthcare costs in the long run. Additionally, sliding scale premiums can promote a sense of fairness and social responsibility within the healthcare system, as they ensure that everyone contributes to the cost of healthcare based on their ability to pay.

However, the implementation of sliding scale premiums also presents certain challenges. One potential issue is the need for accurate income verification to ensure that individuals are placed in the correct tier. This can be a complex and resource-intensive process, requiring coordination between insurers, government agencies, and healthcare providers. Another challenge is the potential for adverse selection, where healthier individuals in higher-income brackets may opt out of the system, leaving a disproportionate share of healthcare costs to be borne by those in lower-income brackets.

Despite these challenges, sliding scale premiums remain an important tool in efforts to create a more equitable and accessible healthcare system. By directly linking the cost of health insurance to an individual's income, this approach can help to ensure that everyone has the opportunity to access necessary healthcare services, regardless of their financial circumstances. As such, sliding scale premiums are a critical component of broader initiatives aimed at reforming healthcare financing and improving health outcomes for all.

Finding Medical Insurance and HMO Premiums: A Guide

You may want to see also

Explore related products

![]()

Subsidies and Assistance: Government aid to help low-income individuals afford health insurance

In the realm of health insurance, subsidies and assistance programs play a crucial role in ensuring that low-income individuals can access necessary medical care. These government-funded initiatives help bridge the gap between affordability and necessity, providing financial support to those who might otherwise struggle to secure adequate insurance coverage. By examining the intricacies of these programs, we can gain a deeper understanding of how they function and the impact they have on the lives of those they serve.

One key aspect of subsidies and assistance is the eligibility criteria. Typically, these programs are designed to target individuals and families with incomes below a certain threshold, often determined by the federal poverty level. Applicants must demonstrate financial need and, in some cases, may be required to contribute a portion of their income towards their insurance premiums. The specific requirements can vary depending on the program and the state in which it is administered, highlighting the importance of understanding local guidelines and regulations.

Another important consideration is the types of health insurance plans that are eligible for subsidies. In many cases, government assistance is only available for plans purchased through official health insurance marketplaces or exchanges. These plans are subject to certain standards and regulations, ensuring that they provide comprehensive coverage and meet the needs of low-income individuals. By limiting subsidies to these plans, governments can help ensure that resources are directed towards high-quality, affordable insurance options.

The application process for subsidies and assistance can be complex, requiring careful attention to detail and a thorough understanding of the relevant forms and documentation. Applicants may need to provide proof of income, residency, and other personal information, and may also be required to undergo a verification process to confirm their eligibility. This can be a time-consuming and potentially daunting task, particularly for those who are unfamiliar with the system or who may have limited access to resources and support.

Despite these challenges, subsidies and assistance programs remain a vital component of the healthcare system, helping to ensure that all individuals, regardless of income, have access to essential medical care. By providing financial support and guidance, these programs can help low-income individuals navigate the complexities of the health insurance landscape and secure the coverage they need to maintain their health and well-being.

Term Insurance: Medical Expenses Covered?

You may want to see also

Explore related products

![]()

Income-Based Eligibility: Qualification for certain health plans or benefits dependent on income level

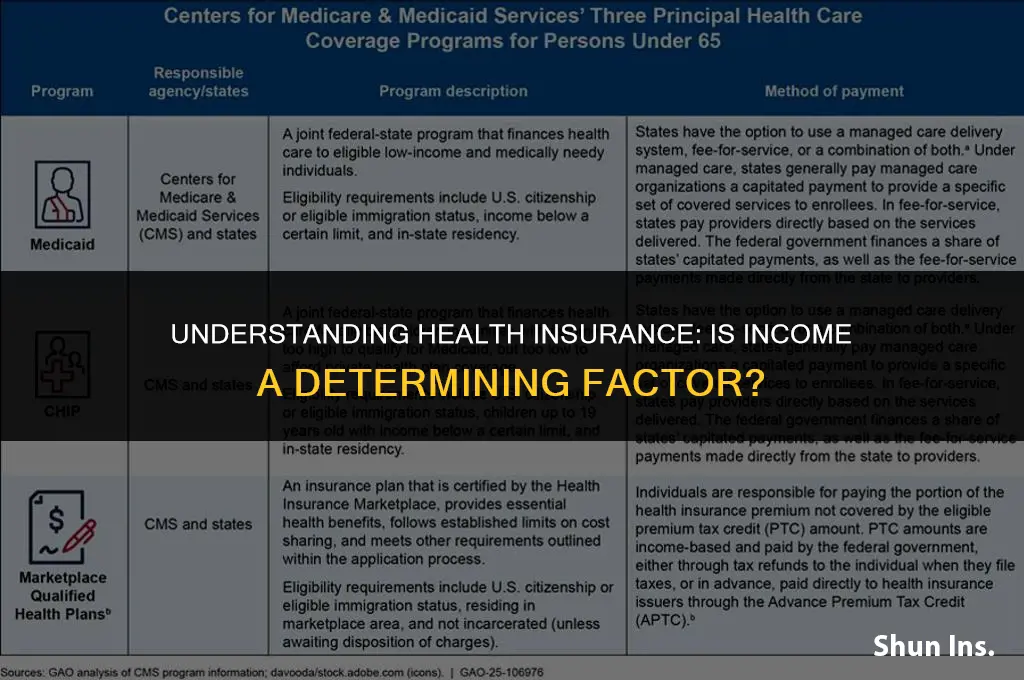

Income-based eligibility plays a crucial role in determining qualification for various health plans and benefits. This system ensures that individuals with lower incomes have access to essential healthcare services that they might not otherwise afford. Programs such as Medicaid and the Children's Health Insurance Program (CHIP) are prime examples of initiatives that use income-based criteria to provide health coverage to eligible participants.

To qualify for these programs, individuals must meet specific income thresholds, which vary depending on the state and the size of the household. For instance, in some states, a family of four earning up to 250% of the Federal Poverty Level (FPL) may be eligible for Medicaid. The FPL is a measure of income issued annually by the Department of Health and Human Services (HHS) and is used to determine eligibility for various federal programs.

The application process for income-based health plans typically involves providing proof of income, such as pay stubs, tax returns, or bank statements. Applicants may also need to furnish documentation of their household size and composition. Once the application is submitted, the relevant state agency will review the information and determine eligibility based on the established income criteria.

It is important to note that income-based eligibility is not the only factor considered in qualifying for health plans. Other criteria, such as residency status, citizenship, and disability status, may also apply. Additionally, some health plans may have specific requirements or restrictions, such as age limits or coverage exclusions, which can impact eligibility.

In conclusion, income-based eligibility is a critical component of ensuring access to healthcare for low-income individuals and families. By understanding the income thresholds and application processes for various health plans, eligible participants can take advantage of these essential benefits to maintain their health and well-being.

Multicultural Medical Group: Insurance Coverage Options

You may want to see also

Explore related products

![]()

Premium Tax Credits: Tax incentives to reduce the cost of health insurance premiums

Premium Tax Credits (PTCs) are a crucial component of the Affordable Care Act (ACA), designed to make health insurance more affordable for lower-income individuals and families. These tax incentives reduce the monthly premium cost for those who purchase health insurance through the ACA marketplaces. The PTC is calculated based on a sliding scale, taking into account the individual's or family's income and the cost of the benchmark plan in their area.

To qualify for PTCs, individuals must meet certain criteria. They must be U.S. citizens or lawfully present immigrants, and their income must fall between 100% and 400% of the Federal Poverty Level (FPL). Additionally, they cannot be eligible for employer-sponsored health insurance or Medicaid. The PTC is applied directly to the monthly premium, and the amount is reconciled at tax time.

One unique aspect of PTCs is that they are advanceable, meaning individuals can receive the credit throughout the year rather than waiting until tax season. This helps to make health insurance more immediately affordable. However, it's important to note that if an individual's income changes significantly during the year, they may need to adjust their PTC to avoid owing money back at tax time.

PTCs are not income-based in the sense that they are not a direct function of an individual's income, but rather they are designed to assist those within a specific income range. The goal is to ensure that health insurance is accessible and affordable for a broader segment of the population, particularly those who might otherwise struggle to afford it.

In summary, Premium Tax Credits are a targeted financial assistance program aimed at reducing the cost of health insurance premiums for lower-income individuals and families. By understanding the eligibility criteria and how the credits are calculated and applied, individuals can better navigate the ACA marketplaces and find a plan that fits their needs and budget.

Health Insurance Impact: How It Influences Health Scientists' Work and Research

You may want to see also

Explore related products

![]()

Medicaid Expansion: Extending Medicaid coverage to more low-income adults under the Affordable Care Act

Medicaid expansion under the Affordable Care Act (ACA) represents a significant shift in how health insurance coverage is determined for low-income adults. Unlike traditional Medicaid eligibility, which was often limited to specific categories such as children, pregnant women, and the elderly or disabled, the ACA's expansion allows states to extend Medicaid coverage to all adults with incomes up to 138% of the federal poverty level. This change is particularly noteworthy because it delinks Medicaid eligibility from specific demographic characteristics and instead bases it solely on income.

One of the key aspects of Medicaid expansion is that it provides a pathway to health insurance coverage for individuals who may not have been eligible under previous Medicaid rules. This includes low-income working adults, individuals without dependent children, and those who are not elderly or disabled. By expanding Medicaid based on income, the ACA aims to reduce the number of uninsured individuals and improve access to healthcare services for those who need it most.

The implementation of Medicaid expansion has varied across states, with some states opting in and others choosing not to expand their Medicaid programs. This has led to significant disparities in health insurance coverage across the country. States that have expanded Medicaid have seen substantial reductions in their uninsured rates, while states that have not expanded Medicaid continue to struggle with higher rates of uninsured individuals.

Medicaid expansion has also had economic implications, both for individuals and for states. For individuals, Medicaid coverage provides financial protection against high medical costs and can help prevent medical debt. For states, expanding Medicaid can lead to increased federal funding and can help offset the costs of providing healthcare services to low-income residents. However, some states have expressed concerns about the long-term sustainability of Medicaid expansion and the potential for increased state costs.

In conclusion, Medicaid expansion under the ACA represents a significant change in how health insurance coverage is determined for low-income adults. By basing eligibility on income rather than specific demographic characteristics, the ACA has provided a pathway to health insurance coverage for millions of Americans. While the implementation of Medicaid expansion has varied across states, the evidence suggests that it has led to improved access to healthcare services and reduced rates of uninsured individuals in states that have opted in.

Widow's Health Insurance: Understanding Coverage After Husband's Disability

You may want to see also

Frequently asked questions

No, not all health insurance is income-based. While some programs like Medicaid are designed to assist low-income individuals, other health insurance plans are available regardless of income level.

Private health insurance plans, such as those offered by employers or purchased individually, are typically not income-based. Additionally, Medicare is a federal program available to individuals over 65 and those with certain disabilities, regardless of income.

Medicaid eligibility is determined based on income level, family size, and other factors. Each state has its own guidelines, but generally, it is designed to assist low-income individuals and families.

Yes, the Children's Health Insurance Program (CHIP) is another income-based program that provides health coverage to children from low-income families who do not qualify for Medicaid.

To determine eligibility for income-based health insurance programs, you can contact your state's Medicaid office or visit the Healthcare.gov website to explore options and apply for coverage.