Amerex self-funded health insurance is a type of health insurance plan in which the employer assumes the financial risk for providing health care benefits to its employees. In practice, self-funded employers pay for each out-of-pocket claim as they are incurred instead of paying a fixed premium to an insurance carrier. Employers often work with a third-party administrator (TPA) to manage the plan, and this model is often more prevalent in larger firms due to their ability to pool risk effectively across a larger employee base. This approach can offer employers more control over health care costs and plan design but also requires careful financial planning and risk management.

Explore related products

What You'll Learn

- Overview of Amerex Self-Funded Health Insurance: Introduction to Amerex's self-funded health insurance options and their benefits

- Eligibility Criteria: Details on who is eligible to enroll in Amerex's self-funded health insurance plans

- Coverage and Benefits: Explanation of the coverage provided and benefits included in Amerex's self-funded health insurance

- Claims Process: Information on how to file claims and the process involved in Amerex's self-funded health insurance

- FAQs: Common questions and answers about Amerex's self-funded health insurance plans and policies

![]()

Overview of Amerex Self-Funded Health Insurance: Introduction to Amerex's self-funded health insurance options and their benefits

Amerex self-funded health insurance offers a unique approach to managing healthcare costs for employers and employees alike. Unlike traditional fully-insured plans, self-funded insurance allows companies to pay for each out-of-pocket claim as they are incurred instead of paying a fixed premium to an insurance carrier. This can lead to significant cost savings for employers, as they only pay for the actual healthcare expenses of their employees rather than a predetermined premium amount.

One of the key benefits of Amerex self-funded health insurance is the flexibility it provides to employers in designing their health benefits packages. Companies can tailor their plans to meet the specific needs of their workforce, offering a range of coverage options and benefit levels. This customization can help employers attract and retain top talent by providing competitive health benefits that align with the needs of their employees.

Another advantage of self-funded health insurance is the potential for lower administrative costs. By working directly with healthcare providers and managing claims internally, employers can reduce the fees associated with insurance carrier administration. Additionally, self-funded plans can offer more transparency in healthcare pricing, as employers have direct insight into the costs of each claim.

However, it's important to note that self-funded health insurance also comes with certain risks and responsibilities. Employers must be prepared to handle the financial burden of unexpected healthcare expenses, which can be significant. Additionally, managing a self-funded plan requires a certain level of expertise and resources, as employers must navigate the complexities of healthcare regulations and claims processing.

Overall, Amerex self-funded health insurance can be a valuable option for employers looking to take control of their healthcare costs and provide customized benefits to their employees. By understanding the unique aspects and potential benefits of self-funded insurance, companies can make informed decisions about whether this approach is right for their organization.

Why Insurance Companies Cancel IMEs: Key Reasons and Implications

You may want to see also

Explore related products

![]()

Eligibility Criteria: Details on who is eligible to enroll in Amerex's self-funded health insurance plans

To determine eligibility for Amerex's self-funded health insurance plans, it's essential to understand the specific criteria set forth by the company. Amerex, like many large corporations, offers self-funded health insurance as a benefit to its employees. This type of insurance plan is typically available to full-time employees who meet certain conditions.

One of the primary eligibility criteria is employment status. Generally, only full-time employees are eligible for self-funded health insurance plans. Part-time employees, contractors, and temporary workers may not qualify. Additionally, there may be a waiting period for new hires before they become eligible for the plan. This waiting period can vary but is often around 90 days.

Another important factor is the employee's location. Amerex operates in multiple states and countries, and the availability of self-funded health insurance plans can vary by location. Some states may have different regulations or requirements that affect eligibility. For example, certain states may require employers to offer health insurance to part-time employees or may have different waiting periods.

Age can also be a factor in determining eligibility. While most self-funded health insurance plans do not have an age limit, some plans may have specific provisions for employees over a certain age. For instance, employees over 65 may be required to enroll in Medicare in addition to the company's plan.

Dependents of eligible employees may also qualify for coverage under Amerex's self-funded health insurance plans. This typically includes spouses and children. However, there may be additional requirements or restrictions for dependent coverage, such as proof of dependency or age limits for children.

It's important for employees to review Amerex's specific eligibility criteria to ensure they meet all the necessary requirements. This information is usually available in the company's benefits guide or through the human resources department. Understanding the eligibility criteria can help employees make informed decisions about their health insurance options and ensure they are properly enrolled in the plan.

Square Trade Insurance: Beyond Accidents

You may want to see also

Explore related products

![]()

Coverage and Benefits: Explanation of the coverage provided and benefits included in Amerex's self-funded health insurance

Amerex's self-funded health insurance offers a comprehensive range of coverage and benefits designed to meet the diverse needs of its employees. One of the key advantages of this plan is its flexibility, allowing employees to choose from a variety of coverage options that best suit their individual circumstances. This includes the ability to select different levels of coverage for medical, dental, and vision care, as well as the option to add dependent coverage.

In terms of benefits, Amerex's self-funded plan provides generous coverage for preventive care, including annual check-ups, vaccinations, and screenings. This emphasis on preventive care not only helps employees maintain their overall health but also reduces the likelihood of more serious health issues down the line. Additionally, the plan offers substantial coverage for prescription medications, with a wide range of drugs included in the formulary.

For those with chronic conditions or ongoing health concerns, Amerex's self-funded insurance provides access to specialized care and treatment options. This includes coverage for mental health services, physical therapy, and occupational therapy, among others. The plan also offers support for employees looking to make healthy lifestyle choices, such as smoking cessation programs and weight management resources.

One unique aspect of Amerex's self-funded plan is its focus on employee wellness. The company offers a variety of wellness initiatives and programs designed to promote overall health and well-being. These include fitness challenges, nutrition counseling, and stress management workshops. By investing in employee wellness, Amerex aims to create a healthier, more productive workforce.

Overall, Amerex's self-funded health insurance provides a robust package of coverage and benefits that cater to the diverse needs of its employees. From preventive care to specialized treatment options, the plan is designed to support employees in maintaining their health and well-being.

Understanding Medical Insurance: Utilizing Your Coverage Effectively

You may want to see also

Explore related products

![]()

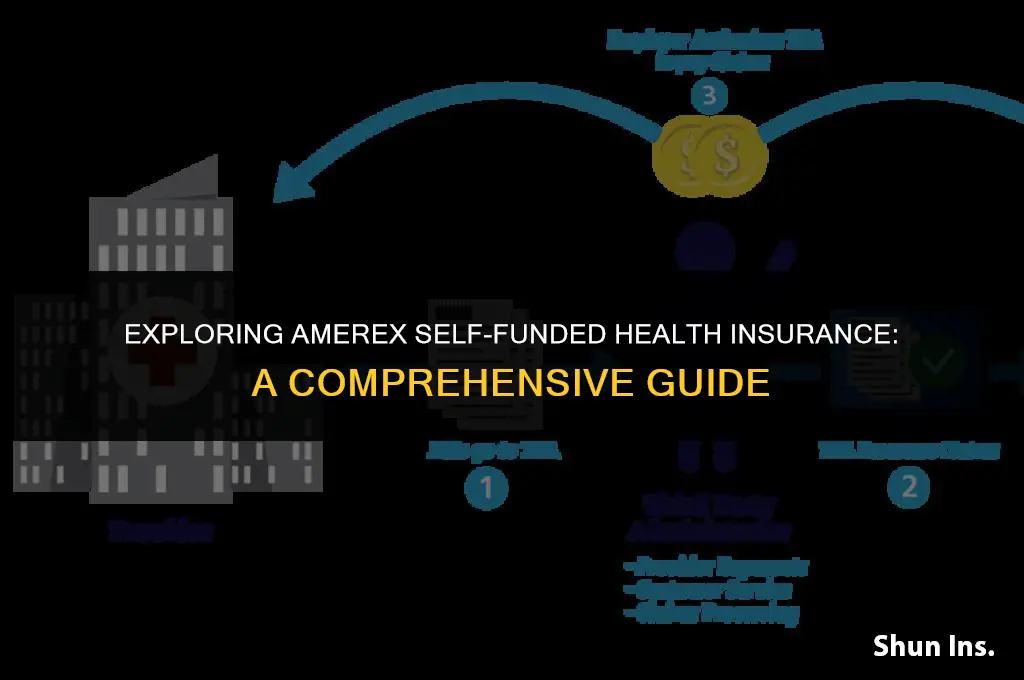

Claims Process: Information on how to file claims and the process involved in Amerex's self-funded health insurance

To file a claim under Amerex's self-funded health insurance, policyholders must follow a specific process. This begins with obtaining the necessary claim forms, which can typically be found on the Amerex website or by contacting their customer service department. The forms will require detailed information about the medical services received, including dates of service, provider names, and itemized charges. It's crucial to ensure all forms are completed accurately and thoroughly to avoid delays in processing.

Once the claim forms are filled out, they should be submitted to Amerex along with any supporting documentation, such as medical bills or receipts. This can usually be done online, by mail, or through a designated claims portal. Policyholders should keep a copy of all submitted documents for their records. After submission, Amerex will review the claim to determine eligibility and coverage. This process may involve verifying the medical necessity of the services, checking for any exclusions or limitations, and coordinating with healthcare providers for additional information if needed.

During the claims process, policyholders may need to provide additional information or clarification regarding their claim. It's important to respond promptly to any requests from Amerex to ensure the claim is processed as quickly as possible. Once a decision has been made, Amerex will notify the policyholder in writing, detailing the amount of the claim that has been approved or denied, along with any applicable deductibles or coinsurance. If a claim is denied, the policyholder has the right to appeal the decision by submitting a written request for review.

Understanding the claims process is essential for policyholders to navigate Amerex's self-funded health insurance effectively. By following the outlined steps and providing accurate information, policyholders can help ensure their claims are processed efficiently and fairly. It's also important for policyholders to familiarize themselves with the terms and conditions of their plan, including coverage limits, exclusions, and any requirements for pre-authorization or referrals. This knowledge can help policyholders make informed decisions about their healthcare and avoid unexpected costs.

Low Interest Rates: A Hidden Threat to Insurance Company Stability

You may want to see also

Explore related products

![]()

FAQs: Common questions and answers about Amerex's self-funded health insurance plans and policies

Amerex's self-funded health insurance plans are designed to provide comprehensive coverage to employees while allowing the company to manage healthcare costs more effectively. One common question is how these plans differ from traditional fully-insured plans. In a self-funded plan, Amerex assumes the financial risk for providing health care benefits to its employees. In practice, this means that the company pays for each out-of-pocket claim as they are incurred instead of paying a fixed premium to an insurance carrier. This approach can lead to significant cost savings for the company, especially if the employee population is relatively healthy.

Another frequently asked question is about the level of coverage provided under Amerex's self-funded plans. These plans typically offer a wide range of benefits, including medical, dental, and vision care, as well as prescription drug coverage. The specific benefits and limitations will vary depending on the plan design chosen by the company, but generally, self-funded plans can be customized to meet the unique needs of the workforce.

Employees often inquire about the process of filing claims under a self-funded plan. With Amerex, claims are usually processed through a third-party administrator (TPA), which handles the paperwork and ensures that claims are paid according to the plan's provisions. Employees may need to provide documentation to support their claims, such as medical bills and receipts for out-of-pocket expenses.

One of the key advantages of self-funded plans is the potential for cost savings, both for the company and its employees. By managing its own health insurance plan, Amerex can avoid the administrative costs and profit margins associated with traditional insurance carriers. This can result in lower premiums for employees and increased flexibility in plan design. Additionally, self-funded plans can offer more competitive benefits packages, which can be a valuable tool for attracting and retaining top talent.

However, self-funded plans also come with certain risks and challenges. One potential drawback is that the company bears the full financial risk of healthcare costs, which can be unpredictable and potentially catastrophic. To mitigate this risk, Amerex may choose to purchase stop-loss insurance, which provides protection against unusually high claims. Another challenge is the administrative burden of managing a self-funded plan, which can be complex and time-consuming. To address this, companies often work with TPAs and other experts to ensure that their plans are running smoothly and efficiently.

In conclusion, Amerex's self-funded health insurance plans offer a unique approach to managing healthcare costs and providing comprehensive benefits to employees. While these plans can offer significant advantages in terms of cost savings and flexibility, they also come with certain risks and challenges that must be carefully considered and managed.

Understanding Lieu Payments: Are They Taxable for Health Insurance?

You may want to see also

Frequently asked questions

Amerex Self-Funded Health Insurance is a type of health insurance plan where the employer assumes the financial risk for providing health care benefits to its employees. In practice, self-funded employers pay for each out-of-pocket claim as they are incurred instead of paying a fixed premium to an insurance carrier. Employers often work with a third-party administrator (TPA) to manage the plan, and this model is also known as a self-insured or self-pay plan.

Unlike traditional health insurance, where employers pay a fixed premium to an insurance company that then covers the health care costs of employees, Amerex Self-Funded Health Insurance involves the employer directly paying for each claim. This approach can potentially save employers money if their employees have fewer health care needs than the average population, as they avoid paying unnecessary premiums. However, it also means that employers bear the full risk of unexpected or high medical costs.

The advantages of Amerex Self-Funded Health Insurance include potential cost savings for employers if their employees have lower than average health care needs, greater control over plan design and benefits, and the ability to customize the plan to better fit the needs of their workforce. On the other hand, the disadvantages include increased financial risk for employers due to the possibility of high or unexpected medical costs, the need for more administrative resources to manage the plan, and the potential for higher costs if the employee population has significant health care needs.