The question of whether an insurance schedule is the same as a certificate often arises due to the overlapping information they provide, yet they serve distinct purposes in the insurance process. An insurance schedule typically outlines the specific details of coverage, including policy limits, deductibles, and covered items, acting as a comprehensive breakdown of the policyholder’s protection. In contrast, an insurance certificate, also known as a proof of insurance, is a concise document that confirms the existence of a policy and its basic terms, often used to demonstrate compliance with legal or contractual requirements. While both documents are essential in managing and verifying insurance coverage, they differ in their level of detail and intended use, making it crucial to understand their unique roles in safeguarding assets and fulfilling obligations.

| Characteristics | Values |

|---|---|

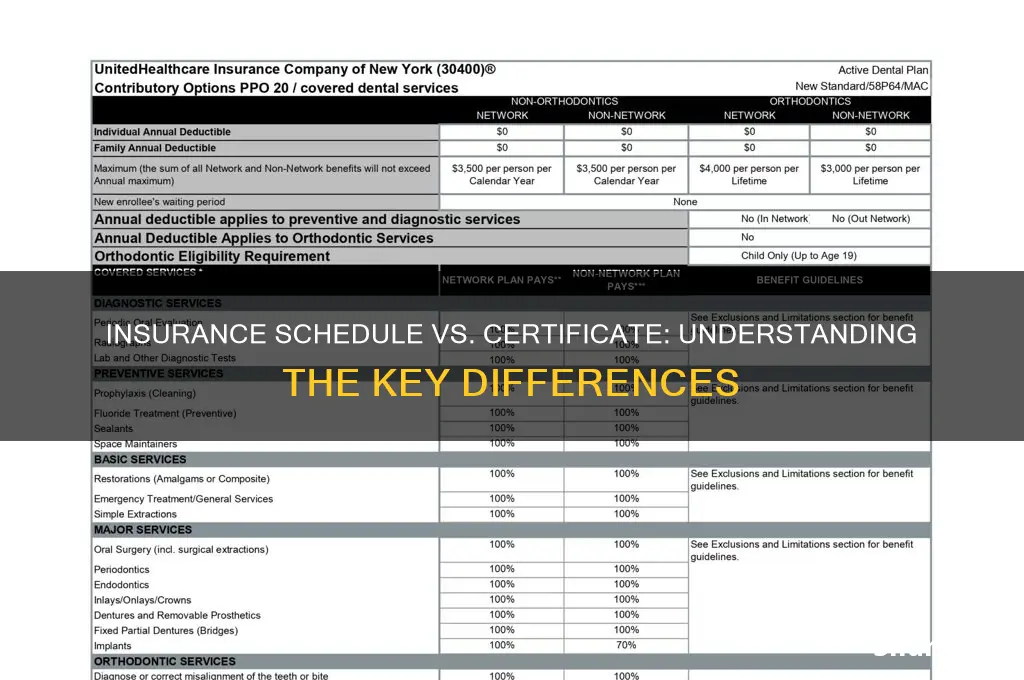

| Definition | An insurance schedule is a detailed list of items or assets covered under a policy, including their descriptions and values. A certificate of insurance (COI) is a document that verifies the existence of an insurance policy and summarizes key details. |

| Purpose | Schedules provide specific coverage details for individual items. Certificates prove insurance coverage to third parties (e.g., clients, landlords). |

| Content | Schedules include itemized lists with descriptions, values, and coverage limits. Certificates include policyholder details, insurer information, coverage types, and policy periods. |

| Recipient | Schedules are typically for the policyholder’s reference. Certificates are issued to third parties as proof of insurance. |

| Legally Binding | Schedules are part of the policy and are legally binding. Certificates are not standalone contracts but confirm the existence of a policy. |

| Format | Schedules are often detailed and attached to the policy. Certificates are concise, standardized documents. |

| Usage | Schedules are used for claims and policy management. Certificates are used to meet contractual or regulatory requirements. |

| Example | A jewelry schedule lists each piece with its value. A COI confirms a contractor has liability insurance for a project. |

| Update Frequency | Schedules may be updated when items are added/removed. Certificates are typically issued once per policy period unless requested. |

| Interchangeability | They are not the same; a schedule is part of the policy, while a certificate is proof of coverage. |

Explore related products

What You'll Learn

![]()

Definition of Insurance Schedule

An insurance schedule is a detailed document that outlines the specific items, assets, or risks covered under an insurance policy. Unlike a general policy document, which provides broad terms and conditions, the schedule itemizes what is insured, often including descriptions, values, and coverage limits for each entry. For instance, in a home insurance policy, the schedule might list high-value items like jewelry, art, or electronics, specifying their appraised worth and the extent of coverage. This precision ensures both the policyholder and insurer have a clear understanding of what is protected, reducing disputes during claims.

Consider the analytical perspective: the insurance schedule serves as a contract appendix, bridging the gap between abstract policy language and tangible assets. It transforms vague coverage into actionable details, making it a critical tool for risk management. For example, a business insurance schedule might detail machinery, inventory, and intellectual property, each with distinct coverage amounts. This granularity allows businesses to assess whether their policy aligns with their actual risk exposure, enabling informed decisions about additional coverage or risk mitigation strategies.

From an instructive standpoint, creating or reviewing an insurance schedule requires meticulous attention to detail. Policyholders should regularly update their schedules to reflect changes in asset value or new acquisitions. For instance, if a homeowner purchases a rare painting, it should be added to the schedule with a professional appraisal to ensure adequate coverage. Similarly, businesses should conduct annual audits of their insured assets, adjusting the schedule to account for depreciation, upgrades, or new investments. Failure to update can lead to underinsurance, leaving significant gaps in protection.

A comparative analysis highlights the distinction between an insurance schedule and a certificate of insurance. While both documents are related to insurance policies, they serve different purposes. A certificate of insurance is a summary document, often used to prove coverage to third parties, such as landlords or contractors. It provides basic policy information, including coverage types, limits, and effective dates. In contrast, the schedule is an internal, detailed record focused on the insured items themselves. For example, a contractor might present a certificate to a client to demonstrate liability coverage, but their insurance schedule would list specific tools and equipment covered under their policy.

Practically, understanding and maintaining an insurance schedule can save policyholders time, money, and stress during the claims process. For instance, if a fire damages a home, a well-maintained schedule allows the insurer to quickly verify the value of lost items, expediting the settlement. Conversely, a missing or outdated schedule can delay claims, as the insurer may require additional proof of ownership and value. To maximize the utility of an insurance schedule, policyholders should keep supporting documents, such as receipts, appraisals, and photographs, organized and accessible. This proactive approach ensures that the schedule remains a reliable tool for both risk management and claims resolution.

Does Erie Insurance Cover Towing? A Comprehensive Guide for Policyholders

You may want to see also

Explore related products

![]()

Purpose of Insurance Certificate

Insurance certificates and schedules serve distinct purposes, though they are often confused due to their overlapping roles in policy documentation. While a schedule typically outlines the specifics of coverage, such as limits, deductibles, and exclusions, an insurance certificate is a concise proof of insurance. Its primary purpose is to verify that a policy exists and is active, providing third parties with assurance that the insured party meets certain coverage requirements. For instance, contractors may need to present a certificate of insurance to clients to secure a job, ensuring they are protected against potential liabilities.

From a practical standpoint, the purpose of an insurance certificate is to streamline verification processes. It condenses complex policy details into a standardized format, making it easier for stakeholders to confirm compliance with legal or contractual obligations. For example, landlords often require tenants to provide a certificate of renters insurance to protect the property. This document eliminates the need to review the entire policy, saving time and reducing the risk of misunderstandings. It acts as a snapshot of coverage, ensuring transparency and trust between parties.

Analytically, the certificate’s role extends beyond mere proof—it serves as a risk management tool. By mandating a certificate, businesses and individuals can mitigate potential financial losses by ensuring their partners, vendors, or tenants are adequately insured. For instance, event organizers might require vendors to submit a certificate of liability insurance before participating in a festival. This proactive approach minimizes exposure to claims that could arise from accidents or damages during the event, safeguarding all involved parties.

Persuasively, the insurance certificate also enhances credibility. For businesses, presenting a certificate to clients or partners demonstrates professionalism and reliability. It signals that the company takes risk management seriously and is prepared to handle unforeseen circumstances. This can be a decisive factor in competitive markets, where trust and assurance are paramount. For example, a construction firm bidding on a project might use a certificate of general liability insurance to differentiate itself from competitors, showcasing its commitment to safety and compliance.

In conclusion, the purpose of an insurance certificate is multifaceted—it provides proof of coverage, simplifies verification, aids in risk management, and bolsters credibility. Unlike a schedule, which details the intricacies of a policy, the certificate is a practical tool designed for quick reference and assurance. Understanding its unique role ensures that individuals and businesses can effectively use it to meet their needs and protect their interests.

Is Healthcare Insurance Mandatory? Understanding Legal Requirements and Benefits

You may want to see also

Explore related products

![]()

Key Differences Explained

Insurance schedules and certificates serve distinct purposes in the realm of policy documentation, often leading to confusion among policyholders. At first glance, both documents provide details about coverage, but their functions diverge significantly. An insurance schedule typically outlines the specific items or assets covered under a policy, along with their respective values and coverage limits. For instance, in a homeowners’ policy, the schedule might list jewelry, art, or electronics, detailing the insured value of each item. In contrast, an insurance certificate is a proof of coverage document, often required by third parties like landlords or contractors, confirming that a policy exists and summarizing its key terms.

Consider a scenario where a contractor requests proof of liability insurance before starting work. The policyholder would provide an insurance certificate, which verifies coverage without revealing intricate details like itemized assets or policy limits. This distinction is crucial for privacy and practicality, as sharing a full schedule could expose sensitive information. Certificates are concise, standardized, and designed for external use, whereas schedules are detailed and primarily for the policyholder’s reference.

Analyzing the structure of these documents further highlights their differences. A schedule is often a multi-page document, meticulously listing covered items, their descriptions, and insured amounts. For example, a business property schedule might include office equipment, inventory, and machinery, each with specific coverage limits. Conversely, a certificate is typically a single-page document, focusing on broad policy details such as the insured party, policy number, coverage period, and insurer’s contact information. This brevity ensures it serves its purpose without overwhelming the recipient.

Practical implications of these differences cannot be overstated. For instance, a landlord requiring proof of renters’ insurance would be satisfied with a certificate, as it confirms coverage without delving into the tenant’s personal belongings. However, if a policyholder needs to file a claim for a stolen laptop, the schedule becomes indispensable, as it specifies the laptop’s insured value. Understanding these roles ensures policyholders use the right document in the right context, avoiding unnecessary complications.

In conclusion, while both insurance schedules and certificates are vital components of policy documentation, their purposes, structures, and usage scenarios differ markedly. Schedules provide detailed, itemized coverage information for the policyholder’s reference, while certificates offer concise proof of coverage for external parties. Recognizing these distinctions empowers policyholders to navigate insurance requirements effectively, ensuring compliance and clarity in all interactions.

Is Your IRA Secure in an Insurance Company Annuity?

You may want to see also

Explore related products

![]()

Legal Implications Compared

Insurance schedules and certificates serve distinct purposes, and their legal implications vary significantly. An insurance schedule typically outlines the specific details of coverage, including policy limits, deductibles, and covered items, whereas a certificate of insurance (COI) provides proof of insurance and summarizes key policy details. This distinction is crucial in legal contexts, as each document is used differently in contractual and liability scenarios. For instance, a schedule might be referenced in a dispute over coverage limits, while a COI is often required to demonstrate compliance with contractual obligations.

Consider a construction project where a contractor must provide proof of liability insurance to the property owner. A COI suffices to meet this requirement, as it confirms the existence and basic terms of the policy. However, if a claim arises and the insurer disputes coverage for specific damages, the schedule becomes the focal point. It contains the granular details that determine whether the claim falls within the policy’s scope. Misunderstanding this difference could lead to legal exposure, such as a contractor being held personally liable for damages if their COI was accepted but their schedule excluded the type of incident in question.

From a legal standpoint, the enforceability of these documents also differs. A COI is generally not a legally binding contract but rather a snapshot of the policy at a given time. In contrast, the schedule is part of the policy itself and carries legal weight in court. For example, if a business is sued and the plaintiff’s attorney discovers that the schedule explicitly excludes the cause of action, the insurer may deny coverage, leaving the business financially vulnerable. This underscores the importance of reviewing both documents carefully, especially in high-risk industries like healthcare or transportation, where coverage gaps can result in catastrophic liabilities.

Practical steps can mitigate these risks. First, always request both the COI and the full policy schedule when entering into contracts involving insurance requirements. Second, ensure that legal counsel reviews these documents to verify alignment with contractual obligations and to identify potential exclusions. Third, periodically update COIs and schedules, particularly after policy renewals or modifications, to avoid discrepancies that could invalidate coverage. For instance, a COI issued last year may no longer reflect current policy terms, exposing all parties to unforeseen risks.

In conclusion, while both documents are integral to insurance management, their legal roles are not interchangeable. The COI serves as a verification tool, whereas the schedule is the authoritative source for coverage details. Ignoring this distinction can lead to costly legal disputes, particularly in industries where insurance is a critical risk management component. By understanding and leveraging these differences, individuals and businesses can better protect themselves from liability and ensure compliance with legal and contractual standards.

Exploring Kansas Insurers Offering Obamacare Plans: A Comprehensive Guide

You may want to see also

Explore related products

![]()

When to Use Each Document

Insurance schedules and certificates serve distinct purposes, and understanding when to use each is crucial for effective policy management. An insurance schedule is a detailed document that outlines the specifics of your coverage, including policy limits, deductibles, and covered items. It acts as a comprehensive reference for both the policyholder and the insurer, ensuring clarity on what is protected and under what conditions. For instance, if you have a homeowners’ policy, the schedule might list individual valuables like jewelry or artwork, along with their insured values. This level of detail is essential during claims processing, as it provides a clear basis for assessing losses.

In contrast, an insurance certificate is a concise proof of coverage, often required by third parties to verify that a policy is in effect. It typically includes the policyholder’s name, insurer details, policy number, and coverage period. For example, contractors may need to provide a certificate of liability insurance to clients before starting a project, or landlords might request one from tenants to ensure they have renters’ insurance. The certificate is not a substitute for the policy itself but rather a snapshot confirming that coverage exists. Its simplicity makes it ideal for situations where a full policy document is unnecessary or impractical to share.

When deciding which document to use, consider the context and the information required. If you’re filing a claim or need to review the specifics of your coverage, the insurance schedule is the go-to document. Its detailed breakdown ensures you understand exactly what is covered and to what extent. On the other hand, if you’re dealing with a third party who needs verification of your insurance status, the certificate is the appropriate choice. Its streamlined format provides the necessary proof without exposing sensitive policy details.

Practical scenarios further illustrate the distinction. Imagine you’re a small business owner leasing a commercial space. Your landlord will likely request an insurance certificate to confirm you have liability coverage, protecting them in case of accidents on your premises. However, if your business experiences a fire and you need to file a claim, the insurer will refer to your schedule to determine the extent of your property coverage and any applicable exclusions. Misusing these documents—such as providing a schedule when a certificate is requested—can lead to delays or misunderstandings, underscoring the importance of selecting the right one for the situation.

In summary, while both documents are integral to insurance management, their applications differ significantly. The schedule is your detailed coverage roadmap, essential for claims and policy reviews, whereas the certificate is a quick proof of insurance for external parties. By recognizing the unique role of each, policyholders can navigate insurance requirements more effectively, ensuring compliance and clarity in all interactions.

Does a Windshield Claim Increase Your AAA Insurance Premiums?

You may want to see also

Frequently asked questions

No, an insurance schedule is a detailed list of items or assets covered under a policy, while a certificate of insurance is a document proving that a policy exists and summarizing its key details.

An insurance schedule usually includes details such as the insured items, their values, coverage limits, and specific terms or conditions related to those items.

A certificate of insurance serves as proof of coverage and is often required by third parties, such as landlords or contractors, to verify that insurance is in place.

No, a certificate of insurance does not replace an insurance schedule, as it lacks the detailed itemized information found in a schedule.

The policyholder usually receives the insurance schedule for their records, while a certificate of insurance is often provided to third parties who need proof of coverage.