The question regarding whether the Affordable Care Act (ACA) insurance penalty for health coverage is still in effect is a common one. The ACA, also known as Obamacare, was a landmark healthcare reform law enacted in 2010 that aimed to increase access to affordable health insurance for millions of Americans. One of the key components of the ACA was the individual mandate, which required most Americans to have health insurance coverage or pay a penalty. However, in 2017, the Tax Cuts and Jobs Act (TCJA) was passed, which included a provision that effectively eliminated the individual mandate penalty starting in 2019. This change led to some confusion among consumers about whether they were still required to have health insurance or if they would face any penalties for not doing so.

Explore related products

What You'll Learn

- Current status of health insurance penalties under the Affordable Care Act (ACA)

- Changes to individual mandate penalties in recent years

- State-specific health insurance penalty information

- Exemptions from health insurance penalties under federal law

- Impact of health insurance penalties on enrollment rates

![]()

Current status of health insurance penalties under the Affordable Care Act (ACA)

The Affordable Care Act (ACA), commonly known as Obamacare, introduced significant changes to the healthcare landscape in the United States, including the implementation of health insurance penalties for individuals who failed to maintain minimum essential coverage. However, the status of these penalties has evolved over time due to legislative and administrative actions.

As of now, the individual mandate penalty, which was a key component of the ACA, has been effectively eliminated. This change was introduced by the Tax Cuts and Jobs Act of 2017, which reduced the penalty amount to $0 starting from the 2019 tax year. This means that individuals are no longer required to pay a penalty if they do not have health insurance coverage.

Despite the elimination of the federal penalty, some states have taken steps to implement their own individual mandates and corresponding penalties. For example, states like California, Massachusetts, and New Jersey have enacted laws requiring residents to maintain health insurance coverage or face state-level penalties. These state-specific mandates and penalties vary in terms of their structure and enforcement mechanisms.

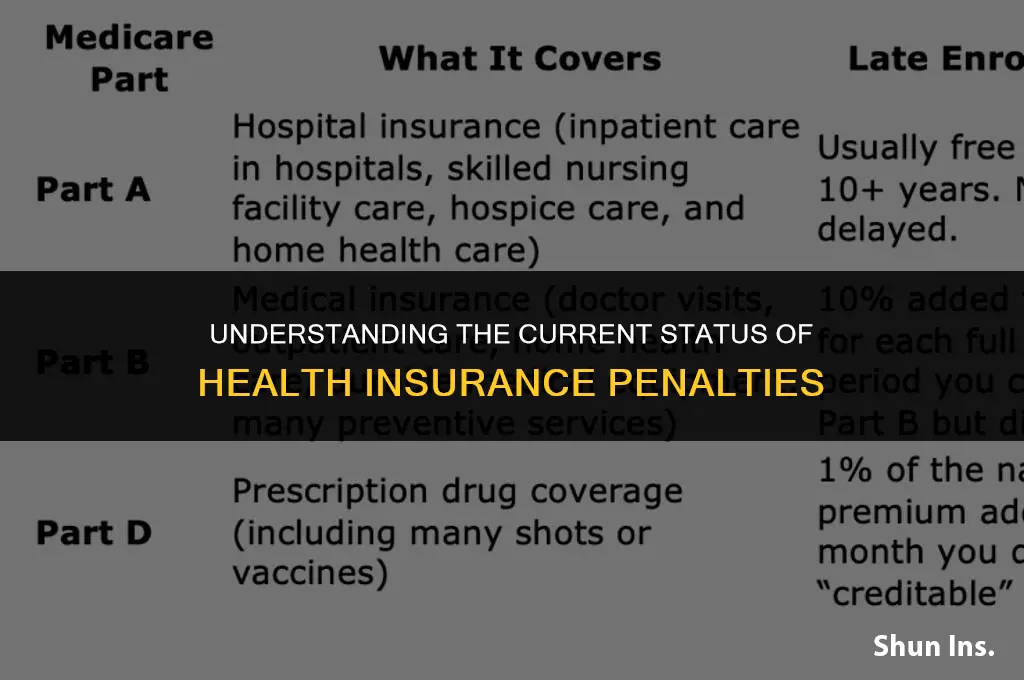

Furthermore, the ACA's employer mandate, which requires certain employers to offer health insurance coverage to their employees or face penalties, remains in effect. Employers with 50 or more full-time employees are generally subject to this mandate, and they must provide coverage that meets minimum essential health benefits standards.

In conclusion, while the federal individual mandate penalty under the ACA has been eliminated, the landscape of health insurance penalties is complex and varies by state. Additionally, the employer mandate continues to be a significant aspect of the ACA, impacting businesses and their employees.

Health Insurance: A Lifeline for Heart Failure Treatment and Care

You may want to see also

Explore related products

![]()

Changes to individual mandate penalties in recent years

The individual mandate penalty, a key component of the Affordable Care Act (ACA), has undergone significant changes in recent years. Initially designed to encourage Americans to maintain health insurance coverage, the penalty was set at a percentage of one's income or a flat fee, whichever was higher. However, the Tax Cuts and Jobs Act of 2017 (TCJA) effectively eliminated the individual mandate penalty starting in 2019, reducing it to $0. This change marked a substantial shift in healthcare policy, as it removed the financial incentive for individuals to purchase health insurance.

Despite the federal penalty's elimination, some states have taken steps to reinstate their own individual mandate penalties. For instance, California, Massachusetts, and New Jersey have implemented state-level penalties to encourage residents to maintain health coverage. These state penalties vary in structure and amount, with some mirroring the original federal penalty and others adopting different approaches. The reinstatement of state penalties reflects the ongoing debate over the role of government in ensuring healthcare access and affordability.

The elimination of the federal individual mandate penalty has had notable implications for the health insurance market. Without the penalty, some younger and healthier individuals may opt out of purchasing insurance, potentially leading to an increase in the number of uninsured Americans. This could result in higher healthcare costs for those who remain insured, as the risk pool becomes less diverse. Additionally, the lack of a penalty may encourage some employers to reconsider their health insurance offerings, potentially impacting the employer-sponsored insurance market.

In conclusion, the changes to individual mandate penalties in recent years have significantly altered the healthcare landscape in the United States. While the federal penalty's elimination has reduced the financial burden on some Americans, it has also raised concerns about the potential consequences for the health insurance market and access to care. The actions of individual states to reinstate penalties highlight the ongoing efforts to address these challenges and ensure that residents have access to affordable health coverage.

Does Private Health Insurance Cover Occupational Therapy? What You Need to Know

You may want to see also

Explore related products

$17.99

![]()

State-specific health insurance penalty information

As of the latest updates, several states have implemented their own health insurance penalty systems to encourage residents to maintain health coverage. These penalties vary widely in terms of structure and severity. For instance, some states like California and New Jersey have established a state-level individual mandate, requiring residents to have health insurance or pay a penalty. The penalties in these states are often calculated as a percentage of the resident's income or a flat fee, whichever is higher.

In contrast, other states have opted for different approaches. For example, Texas and Florida do not have a state-level individual mandate, but they may impose penalties in other forms, such as higher premiums for those who do not maintain continuous coverage. Additionally, some states have expanded Medicaid under the Affordable Care Act, which indirectly influences the penalty structure by providing more affordable health coverage options to low-income residents.

It's crucial for individuals to understand their state's specific health insurance penalty information to avoid unexpected fines and ensure they have adequate coverage. Residents can typically find this information through their state's health department website or by consulting with a licensed insurance agent. Staying informed about these penalties can help individuals make more informed decisions about their health insurance and avoid unnecessary financial burdens.

Why Insurance Companies Use BMI: Understanding Its Role in Policies

You may want to see also

Explore related products

![]()

Exemptions from health insurance penalties under federal law

Under the Affordable Care Act (ACA), most U.S. citizens and legal residents are required to have health insurance or pay a penalty. However, there are several exemptions from this penalty, which can be broadly categorized into three groups: exemptions based on income, exemptions based on hardship, and exemptions based on other circumstances.

Income-based exemptions are available for individuals whose household income is below a certain threshold. For example, if your income is less than 138% of the federal poverty level, you may be eligible for Medicaid, which would exempt you from the penalty. Additionally, if your income is between 100% and 400% of the federal poverty level, you may be eligible for premium tax credits, which can help reduce the cost of health insurance and potentially exempt you from the penalty.

Hardship exemptions are available for individuals who have experienced certain types of financial or personal hardship. For example, if you have filed for bankruptcy, are homeless, or have been evicted, you may be eligible for a hardship exemption. Other circumstances that may qualify for a hardship exemption include the death of a family member, a serious illness, or a natural disaster.

Exemptions based on other circumstances are available for individuals who meet certain criteria that are not related to income or hardship. For example, if you are a member of a federally recognized tribe, are eligible for Medicare, or are a veteran, you may be exempt from the penalty. Additionally, if you are a foreign national or a non-resident alien, you may be exempt from the penalty.

It's important to note that the process for obtaining an exemption can be complex and may require documentation to prove your eligibility. If you believe you may be eligible for an exemption, it's recommended that you consult with a healthcare professional or a tax advisor to discuss your options.

Adding a Dependent to Health Insurance: A Step-by-Step Guide

You may want to see also

Explore related products

$41.99 $33.29

![]()

Impact of health insurance penalties on enrollment rates

The impact of health insurance penalties on enrollment rates has been a subject of significant debate and analysis. Historically, penalties were introduced as a means to encourage individuals to maintain health coverage, thereby reducing the financial burden on healthcare systems and ensuring a more stable insurance market. However, the effectiveness of these penalties in actually increasing enrollment rates has been a matter of contention.

Research indicates that while penalties can indeed motivate some individuals to enroll in health insurance plans, the overall impact on enrollment rates is often modest. This is partly because many people who are subject to penalties may already be aware of the importance of health insurance and are more likely to enroll regardless of the penalty. Additionally, penalties may disproportionately affect lower-income individuals who may find the cost of insurance prohibitive, even with the threat of a penalty.

Moreover, the design and implementation of penalty systems can greatly influence their effectiveness. For instance, penalties that are too low may not provide sufficient motivation for individuals to enroll, while penalties that are too high may lead to resentment and non-compliance. Furthermore, the complexity of penalty structures and the difficulty of understanding them can also hinder their effectiveness in promoting enrollment.

In recent years, there has been a shift towards alternative approaches to increasing health insurance enrollment, such as expanding Medicaid, implementing subsidies, and improving outreach and education efforts. These strategies have shown promise in increasing coverage rates without the need for punitive measures. Nonetheless, the role of penalties in health insurance systems remains a topic of ongoing discussion and evaluation, as policymakers seek to balance the need for coverage with the potential negative impacts of penalizing non-enrollment.

Best Insurance Options for Your Medical Billing Business

You may want to see also

Frequently asked questions

As of my last update in June 2024, the individual mandate penalty for not having health insurance, which was a key provision of the ACA, has been repealed. The Tax Cuts and Jobs Act of 2017 eliminated the penalty starting from the 2019 tax year.

The repeal of the individual mandate means that individuals are no longer required by federal law to maintain health insurance coverage or pay a penalty. However, some states have implemented their own individual mandates to encourage residents to maintain health insurance coverage.

Yes, there have been several changes to the ACA over the years. For example, the Tax Cuts and Jobs Act of 2017 also eliminated the cost-sharing reductions that helped lower out-of-pocket costs for some individuals. Additionally, there have been changes to the subsidies available for health insurance premiums. It's important to stay informed about these changes as they can impact your health insurance options and costs.

To find out if your state has its own individual mandate for health insurance, you can check with your state's insurance department or visit their official website. You can also consult with a health insurance professional or navigator who can provide you with information about your state's specific requirements and options for health insurance coverage.