When comparing health insurance plans, the terms bronze and silver refer to categories that indicate the level of coverage and cost-sharing between the insured and the insurer. Bronze plans typically have lower premiums but higher out-of-pocket costs, making them suitable for individuals who expect to have few health expenses. On the other hand, silver plans offer a middle ground with moderate premiums and out-of-pocket costs, providing a more balanced approach to coverage. The question of whether bronze is better than silver health insurance depends on an individual's specific healthcare needs, budget, and risk tolerance.

Explore related products

What You'll Learn

- Coverage Comparison: Evaluate the differences in coverage between bronze and silver plans

- Cost Analysis: Compare the premiums, deductibles, and out-of-pocket costs for each plan

- Benefit Limitations: Assess any restrictions or limitations on benefits in bronze versus silver plans

- Eligibility Criteria: Determine who might be more suited for bronze or silver plans based on health needs

- Long-term Value: Consider the potential long-term financial impact of choosing bronze over silver insurance

![]()

Coverage Comparison: Evaluate the differences in coverage between bronze and silver plans

When evaluating the differences in coverage between bronze and silver plans, it's essential to understand the nuances of each plan type. Bronze plans typically offer lower premiums but higher out-of-pocket costs, while silver plans have higher premiums but lower out-of-pocket costs. This trade-off is crucial for individuals to consider when selecting a plan that best fits their healthcare needs and budget.

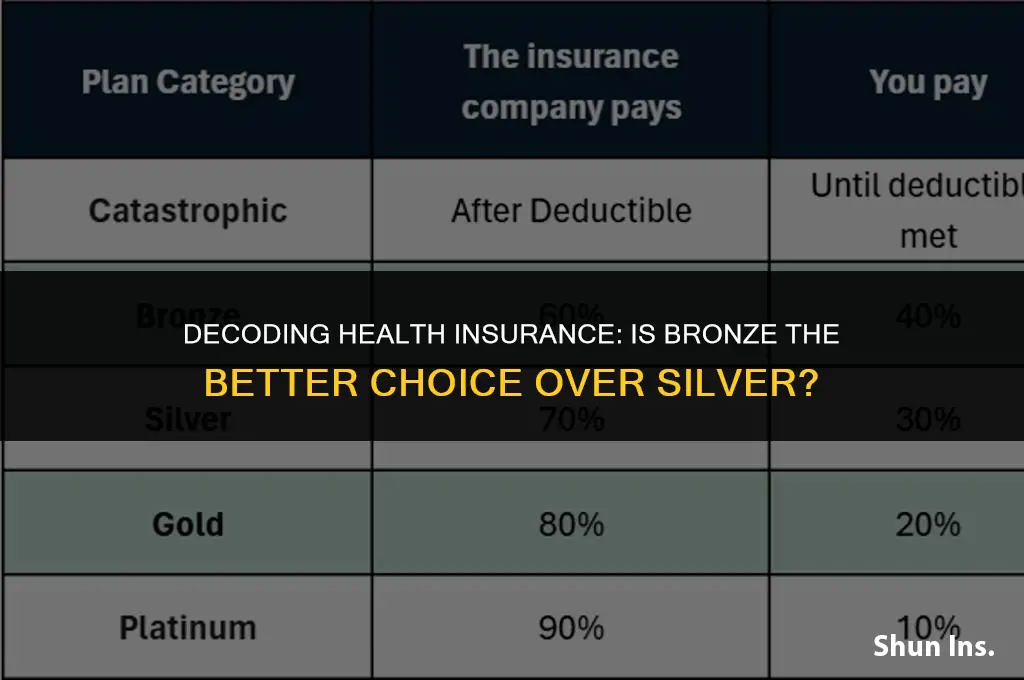

One key aspect to compare is the actuarial value of each plan. Bronze plans generally cover about 60% of healthcare costs, leaving the insured responsible for the remaining 40%. Silver plans, on the other hand, cover approximately 70% of costs, with the insured paying 30%. This difference in actuarial value can significantly impact the overall cost of healthcare for an individual, especially those with chronic conditions or frequent medical needs.

Another important factor to consider is the deductible. Bronze plans often have higher deductibles, which means the insured must pay more out-of-pocket before the plan starts covering costs. Silver plans typically have lower deductibles, providing more immediate coverage. However, the lower deductible on a silver plan is offset by the higher premium cost.

Additionally, the copayments and coinsurance rates differ between bronze and silver plans. Bronze plans usually have higher copayments and coinsurance rates, increasing the insured's out-of-pocket expenses for each medical service. Silver plans offer lower copayments and coinsurance rates, making each visit to a healthcare provider less costly.

In conclusion, when comparing bronze and silver plans, individuals must weigh the trade-offs between premium costs and out-of-pocket expenses. Those who anticipate frequent medical needs may benefit more from a silver plan, despite the higher premiums, due to the lower deductibles and copayments. Conversely, individuals who expect fewer medical expenses might find a bronze plan more cost-effective, given its lower premium cost. Ultimately, the choice between bronze and silver plans depends on an individual's specific healthcare needs and financial situation.

Missed Open Enrollment? Steps to Secure Health Insurance Coverage Now

You may want to see also

Explore related products

![]()

Cost Analysis: Compare the premiums, deductibles, and out-of-pocket costs for each plan

Let's delve into a detailed cost analysis comparing the premiums, deductibles, and out-of-pocket costs for Bronze and Silver health insurance plans. This comparison will help you understand the financial implications of choosing one plan over the other.

Premium Costs:

Bronze plans typically have lower premiums compared to Silver plans. This is because Bronze plans offer less coverage, which means the insurance company takes on less risk. For example, a Bronze plan might cost $200 per month, while a comparable Silver plan could cost $300 per month. This $100 difference in premiums can add up to $1,200 annually, making the Bronze plan more attractive for those looking to save on monthly costs.

Deductible Costs:

However, the lower premium of a Bronze plan comes with a trade-off: higher deductibles. A deductible is the amount you must pay out-of-pocket before your insurance coverage kicks in. Bronze plans often have deductibles ranging from $5,000 to $7,000, while Silver plans typically have deductibles between $2,500 and $4,000. This means that with a Bronze plan, you'll need to pay more upfront for medical expenses before your insurance starts to cover the costs.

Out-of-Pocket Costs:

In addition to deductibles, it's important to consider other out-of-pocket costs, such as copays and coinsurance. Copays are fixed amounts you pay for certain services, like doctor visits or prescriptions, while coinsurance is a percentage of the cost you're responsible for after meeting your deductible. Bronze plans generally have higher copays and coinsurance rates than Silver plans. For instance, a Bronze plan might have a $30 copay for a doctor visit and a 20% coinsurance rate, whereas a Silver plan could have a $20 copay and a 15% coinsurance rate.

Cost Analysis Example:

To illustrate the cost differences, let's consider a scenario where you need medical treatment costing $10,000. With a Bronze plan, you'd pay the $5,000 deductible upfront, then 20% of the remaining $5,000 as coinsurance, totaling $1,000. Your total out-of-pocket cost would be $6,000. In contrast, with a Silver plan, you'd pay a $2,500 deductible and 15% of the remaining $7,500 as coinsurance, totaling $1,125. Your total out-of-pocket cost would be $3,625.

In conclusion, while Bronze plans offer lower premiums, they come with higher deductibles and out-of-pocket costs. Silver plans, on the other hand, have higher premiums but lower deductibles and out-of-pocket costs. When deciding between the two, it's crucial to consider your expected healthcare needs and budget. If you anticipate needing frequent medical care, a Silver plan might be more cost-effective despite the higher premium. Conversely, if you're generally healthy and want to save on monthly costs, a Bronze plan could be the better choice.

Why Life Insurance Companies Face Federal Regulation: Key Insights

You may want to see also

Explore related products

![]()

Benefit Limitations: Assess any restrictions or limitations on benefits in bronze versus silver plans

When evaluating the benefits of bronze versus silver health insurance plans, it's crucial to understand the limitations and restrictions that come with each. Bronze plans, while typically more affordable, often have more stringent limitations on benefits compared to silver plans. One key area to assess is the coverage for pre-existing conditions. Bronze plans may have waiting periods or exclusions for certain pre-existing conditions, whereas silver plans might offer more immediate coverage.

Another important aspect to consider is the prescription drug coverage. Bronze plans may have higher copays or coinsurance rates for medications, potentially making them less suitable for individuals with chronic conditions requiring long-term prescriptions. In contrast, silver plans often provide more comprehensive drug coverage, which can be a significant advantage for those with ongoing medication needs.

Additionally, bronze plans might limit the number of doctor visits or hospital stays covered per year, imposing caps on certain services. Silver plans, on the other hand, tend to offer more generous coverage limits, providing greater peace of mind for policyholders who may require more extensive medical care.

It's also essential to examine the provider networks associated with each plan. Bronze plans may have narrower networks, restricting the choice of healthcare providers and facilities available to policyholders. Silver plans typically offer broader networks, allowing for more flexibility in selecting healthcare providers.

In conclusion, while bronze plans can be more cost-effective, they often come with more significant benefit limitations compared to silver plans. Policyholders should carefully assess their healthcare needs and consider the potential impact of these limitations when choosing between bronze and silver health insurance options.

Exploring Government-Funded Health Insurance Options in Florida

You may want to see also

Explore related products

![A comparison of the costs of major national health insurance proposals by Gordon R. Trapnell Consulting Actuaries. 1976 [Leather Bound]](https://m.media-amazon.com/images/I/81nNKsF6dYL._AC_UY218_.jpg)

![]()

Eligibility Criteria: Determine who might be more suited for bronze or silver plans based on health needs

To determine who might be more suited for bronze or silver plans based on health needs, it's essential to understand the fundamental differences between these two types of health insurance plans. Bronze plans typically have lower premiums but higher out-of-pocket costs, making them suitable for individuals who are generally healthy and don't anticipate frequent medical expenses. On the other hand, silver plans have higher premiums but lower out-of-pocket costs, which can be beneficial for those who require more frequent medical care or have chronic conditions.

When evaluating eligibility for bronze or silver plans, consider the following factors: age, overall health status, frequency of doctor visits, prescription medication needs, and the presence of any chronic health conditions. Younger individuals or those in good health may find bronze plans more cost-effective, while older individuals or those with health issues may benefit more from silver plans due to the reduced out-of-pocket expenses.

Additionally, it's crucial to assess the expected annual healthcare costs. If an individual anticipates high medical expenses, a silver plan may provide better financial protection despite the higher premium. Conversely, if an individual expects low medical costs, a bronze plan could be a more economical choice.

Another important consideration is the plan's actuarial value. Bronze plans generally cover about 60% of healthcare costs, while silver plans cover approximately 70%. This difference can significantly impact the financial burden on the policyholder, especially in the event of unexpected medical emergencies.

In conclusion, determining eligibility for bronze or silver plans based on health needs requires a careful evaluation of various factors, including age, health status, expected medical expenses, and the plan's actuarial value. By considering these aspects, individuals can make informed decisions about which plan best suits their healthcare needs and financial situation.

Adding a Dependent to Your Medical Mutual Insurance Plan

You may want to see also

Explore related products

$34.45 $110

![]()

Long-term Value: Consider the potential long-term financial impact of choosing bronze over silver insurance

When evaluating the long-term financial impact of choosing bronze over silver insurance, it's crucial to consider the trade-offs between lower premiums and higher out-of-pocket costs. Bronze plans typically have lower monthly premiums, which can be appealing for individuals looking to save money in the short term. However, these plans often come with higher deductibles, copays, and coinsurance rates, which can add up significantly over time.

To illustrate this point, let's consider an example. Suppose an individual chooses a bronze plan with a monthly premium of $200 and a deductible of $6,000. Over the course of a year, they would pay $2,400 in premiums. If they require medical care that costs $10,000, they would be responsible for paying the full $6,000 deductible, plus any additional coinsurance or copays. In this scenario, the individual would pay a total of $8,400 out of pocket, in addition to their premiums.

In contrast, a silver plan might have a higher monthly premium of $300, but a lower deductible of $3,000. Over the course of a year, the individual would pay $3,600 in premiums. If they require the same $10,000 medical care, they would be responsible for paying the $3,000 deductible, plus any additional coinsurance or copays. In this scenario, the individual would pay a total of $6,600 out of pocket, in addition to their premiums.

As you can see, the bronze plan may seem more affordable in the short term, but it can actually be more expensive in the long run. This is because the higher out-of-pocket costs can quickly add up, especially if the individual requires frequent or expensive medical care. Therefore, it's important to carefully consider the potential long-term financial impact of choosing bronze over silver insurance before making a decision.

Navigating Healthcare Without Insurance: A Comprehensive Guide

You may want to see also

Frequently asked questions

Bronze plans typically have lower premiums but higher out-of-pocket costs, while silver plans have higher premiums but lower out-of-pocket costs. Bronze plans also generally have a lower actuarial value, covering about 60% of healthcare costs, compared to silver plans, which cover about 70%.

Yes, bronze health insurance might be more cost-effective for individuals who don't visit the doctor frequently, as they can benefit from the lower premiums without incurring high out-of-pocket costs.

The actuarial value represents the percentage of healthcare costs that the insurance plan covers. A bronze plan with a lower actuarial value (around 60%) might be more suitable for those who want to pay less upfront but are willing to cover more costs out-of-pocket. In contrast, a silver plan with a higher actuarial value (around 70%) provides more coverage but comes with higher premiums.

Yes, you can switch from a bronze to a silver health insurance plan during the open enrollment period. This allows you to reassess your healthcare needs and budget, and choose a plan that better suits your requirements for the upcoming year.