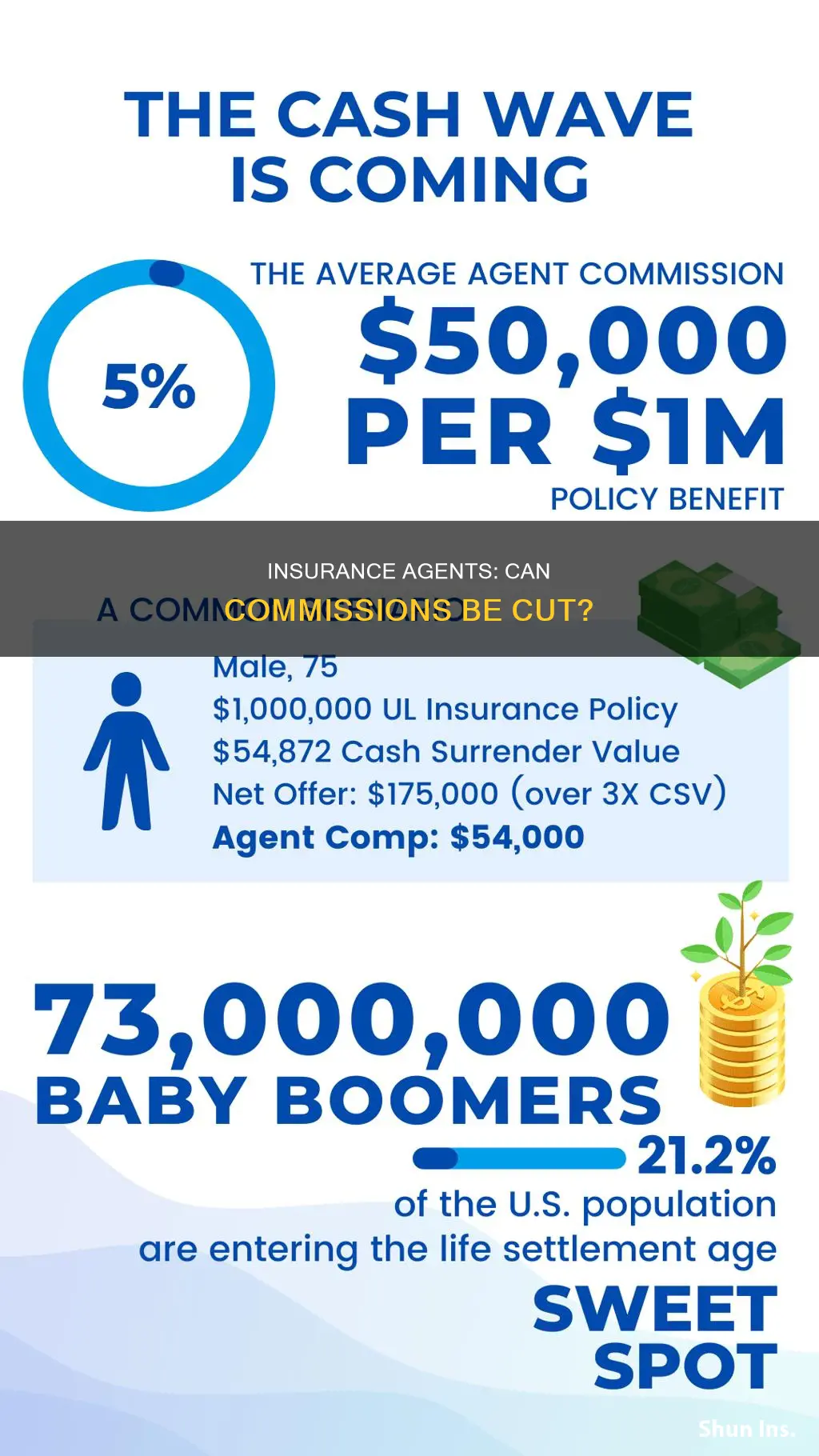

Insurance agents are usually paid a commission on the insurance policy premiums they sell, which incentivizes them to promote policies with higher premiums. While commissions are an important source of income for agents, they can also slow the cash value growth of permanent life insurance policies. Commissions are part of an insurer's expenses, and while the law does not require an insurance agent to collect their earned commission, refusing to do so does not affect the premium charged to the insured. Carriers are permitted to reduce agency commissions, which is controlled by the agency agreement executed between the insurance carrier and the agent or agency. However, there is little law or regulation related to the payment of commission to an insurance agent, and the lack of standardized commission clauses and levels can make it difficult for agents to know their rights.

| Characteristics | Values |

|---|---|

| Legality of cutting insurance agent commissions | Legal, as long as it is outlined in the agency agreement between the insurance carrier and the agent/agency |

| Commission protection | Derived from private contracts, not laws or regulations |

| Notification requirements | Carriers must notify agencies of commission reductions, but this may occur simultaneously with the reduction or without advance notice |

| Commission variability | Commission levels vary depending on the line of business and whether the policy is new or a renewal |

| Commission incentives | Agents may be incentivized to promote policies with higher premiums, such as permanent life insurance, due to higher commission percentages |

| Commission disclosure | In some states, agents must disclose their commission amount if the applicant requests it |

| Commission alternatives | Some insurers have salaried "consultants" instead of commissioned agents |

| Commission clawbacks | Carriers may have the contractual right to take back commissions if a policy is cancelled shortly after purchase or if the agent sold the policy without an active license |

Explore related products

What You'll Learn

![]()

Commission structures and their impact on policyholder interactions

Commission structures play a crucial role in shaping insurance agents' interactions with policyholders. Commissions are a common source of income for agents, and they are typically paid a percentage of the insurance policy premiums as commission. This commission-based structure incentivizes agents to promote policies with higher premiums, as it directly impacts their earnings. For instance, permanent life insurance policies often result in higher commissions for agents due to their higher premiums compared to term life insurance. This may influence agents to recommend permanent policies even if the commission percentage is identical since the total commission earned is higher.

The commission structure also impacts the relationship between insurance agents and policyholders. Residual commissions, or commissions earned on renewal of policies, encourage long-term relationships between agents and policyholders, as client satisfaction becomes a priority for agents. Independent insurance agents, who are not tied to a single provider, may have higher commissions than captive agents, providing them with an incentive to find the most suitable coverage for their clients. This flexibility in carrier representation allows independent agents to better serve their clients' interests while maximizing their earnings.

However, the commission structure can also lead to potential conflicts of interest. Since commissions are tied to premiums, agents may be motivated to recommend policies with higher premiums, even if they may not be the best fit for the policyholder. This could result in policyholders paying higher premiums than necessary. Additionally, agents may be hesitant to disclose their commission rates, as mentioned in some states, they are required to do so upon request. This lack of transparency can create a knowledge gap between the agent and the policyholder, potentially impacting the trust in their relationship.

Furthermore, the insurance industry is undergoing a transition, with carriers facing challenges due to severe weather, rising interest rates, and increasing replacement costs. As a result, carriers are adjusting their underwriting appetites, which can lead to increased premiums or policy cancellations for clients and reduced commission levels for agents. These changes can disrupt the stability of the industry and impact the earnings of insurance agents.

While there is limited regulation regarding commission payments, the existing laws focus on protecting policyholders from excessive charges. For example, in New York, insurance agents are prohibited from charging or demanding rates that deviate from the approved rates and schedules, ensuring that policyholders are not subjected to arbitrary pricing. Additionally, insurance agents who forgo collecting their earned commissions are not allowed to reduce the premium, as it would constitute rebating and violate state laws.

In conclusion, commission structures significantly influence the interactions between insurance agents and policyholders. While commissions incentivize agents to provide suitable coverage and promote long-term relationships, they can also create conflicts of interest and impact the transparency of the insurance-buying process. As the insurance industry navigates a period of change, carriers, agents, and policyholders alike must adapt to new challenges and opportunities.

Becoming an Arizona Insurance Agent: Steps to Success

You may want to see also

Explore related products

![]()

Commission clawbacks and their causes

Commission clawbacks are an unfortunate but common part of the insurance industry. They occur when an insurance agent or variable lines broker receives a commission they didn't or shouldn't have earned. While the insurance landscape is evolving, with carriers offering more personalized experiences, commission clawbacks can negatively impact the individual producer or broker, the agency or brokerage firm, and the carrier.

The most common reason for an insurance carrier to reclaim a commission is because the policyholder stopped paying for or canceled their policy. This can happen for various reasons, including a consumer changing their mind, a change in financial circumstances, or pressure from an insurance agent to buy a product that wasn't suitable. Carriers usually include a clawback clause in their contracts for when a policy is canceled "early," and they typically pay commissions at the start of a policy term, assuming it will be in effect for the entire period. Life insurance commissions, for example, tend to have larger clawbacks if the policy is canceled within the first two years, as carriers expect premium payments for years or decades.

Commission clawbacks can also occur due to licensing issues. For instance, if a policy is sold without an active license, the sale is invalid, and the carrier will reclaim the commission. Similarly, a producer may accidentally sell a policy without the correct carrier appointment in place, which is still considered illegal and results in a commission clawback.

To avoid commission clawbacks, it is essential to stay on top of compliance requirements and maintain an active license. While carriers can educate their producers on preventing clawbacks, neither party has complete control over the policyholder's future behavior. Technology can also play a crucial role in providing an audit trail, automating validation processes, and ensuring compliance to reduce the occurrence of commission clawbacks.

Fleet Insurance: Private Coverage for Your Business Vehicles

You may want to see also

Explore related products

![]()

The legality of commission cuts

The lack of standardisation in commission clauses and levels across different agencies and carriers makes it challenging for agents to know their rights and prove violations. While some contracts may provide vague provisions for carriers to alter commission levels with "notice" or "advance notice", these terms still grant carriers significant latitude to make unilateral and rapid changes. This can result in agents receiving reduced commissions with little to no warning.

In certain situations, insurance agents may choose to forego collecting their earned commissions and instead enter into ""consulting" agreements with insured individuals or businesses, receiving fees directly from them. While this practice may be permissible in some states, it is important to note that refusing to collect commissions cannot affect the premium charged to the insured. Reducing the premium to compensate for foregone commissions may violate insurance laws, as seen in the example of New York State law.

The insurance industry is experiencing a seismic shift in how carriers interact with agents, particularly with the introduction of lower-cost alternatives and the increasing capability of insurance companies to predict losses. Carriers are increasingly focused on cost reduction, which may result in agents facing lower commission levels and more challenging income prospects in the future. This shift also impacts client acquisition strategies, with carriers commoditising their pricing and agents needing to differentiate themselves to remain competitive.

To summarise, while the legality of commission cuts for insurance agents is primarily governed by contractual agreements, the dynamic nature of the insurance industry underscores the importance of agents understanding their rights and staying informed about changes in carrier practices and regulations.

Benefits of Insuring Multiple Accounts at One Bank

You may want to see also

Explore related products

![]()

The impact of market changes on insurance agent commissions

The insurance industry is undergoing a period of transition, with carriers changing their underwriting appetites in response to severe weather events, rising interest rates, and increasing replacement costs. These market changes have had a significant impact on insurance agent commissions.

One of the most notable effects is the disruption faced by insurance agents and their clients. Carriers are reducing commission levels for agents, which is generally permitted by law. This reduction in commissions is driven by carriers' focus on cost reduction, allowing them to maintain profitability even with higher loss ratios. As a result, agents may struggle to maintain their income levels, especially with increasing competition from non-traditional sources in the policy selling business.

Commission structures themselves can also be influenced by market changes. For example, "low-load" insurers are emerging, employing salaried "consultants" instead of commissioned agents. Additionally, the traditional commission-based model may be challenged by a fee-for-service structure, where agents charge a fee for their services rather than earning a commission. This alternative model has been proposed to enhance competition and incentivize agents to provide better value and customer service.

To adapt to these market changes, insurance agents need to focus on client acquisition and retention strategies. Understanding the nuances of commission structures and staying compliant with licensing and carrier appointment requirements are crucial for agents to maximize their earning potential and avoid commission clawbacks.

Understanding Insurance Marketplace: What You Need to Know

You may want to see also

Explore related products

![]()

The future of insurance agency commissions

The insurance industry is undergoing a period of transition, with carriers changing their underwriting appetites in response to severe weather events, rising interest rates, and increasing replacement costs. This transition is disrupting the work of insurance agents and their clients. Carriers are increasingly focused on cost reduction, which may result in agents receiving lower commissions in the future.

While insurance law and regulation have little to say about commission payments, these are controlled by agency agreements between carriers and agents or agencies. Commission clauses in these agreements typically include provisions on commission levels and notification requirements for any changes. Carriers have significant latitude to alter commission levels, and a reduction in commissions is a frequent occurrence that can negatively impact agents' income.

The current system of commissions has been criticised as anti-competitive, providing little incentive for agencies to offer exceptional value or customer service. Some have advocated for deregulation of pricing and the elimination of commissions, allowing agents to differentiate themselves and price their services accordingly. This strategy has been successful in other industries, and it could enhance buyer sophistication and freedom of choice.

However, commissions play a crucial role in incentivising agents to provide suitable coverage options and build long-term relationships with policyholders. Independent agents, in particular, have an incentive to find the most valuable coverage for their clients due to their higher commissions.

Looking ahead, insurance agents may face challenges to their income streams as carriers pursue cost-cutting measures and competition increases from non-traditional sources. Agents will need to adapt to these changing dynamics to ensure their long-term survival and success.

Becoming an Insurance Agent: A Guide for Nigerians

You may want to see also

Frequently asked questions

Yes, insurance carriers are permitted to reduce agency commissions. While there is little law or regulation related to the payment of commission to an insurance agent, commission levels are controlled by the agency agreement executed between the insurance carrier and the agent or agency.

An insurance commission clawback is when an insurance agent has to repay some or all of the commission they earned on a sale to the insurance carrier or financial institution that issued it. This can occur when a policyholder cancels a policy soon after purchasing it or when the agent didn't have the legal authority to sell the policy.

While there is limited law or regulation regarding commission payments, insurance agents are required to disclose the amount they're earning in commission if the applicant requests it in certain states. Additionally, the refusal to collect commission by an insurance agent or broker cannot result in a reduced premium for the insured.