Disability insurance is a type of insurance that provides income to a worker who is unable to work due to a disability. It is intended to replace some of the worker's lost income, covering the opportunity cost of the now-disabled worker. It is different from medical insurance, which covers treatment for injuries or illnesses. Medical insurance can be private or provided through employers, while disability insurance can be either government-sponsored or private.

Explore related products

What You'll Learn

- Disability insurance provides income replacement if a worker is unable to work due to disability

- It is available through public and private programs

- Qualification depends on the severity of the disability and its impact on work

- The cost depends on the plan's terms, benefit period, and definition of disability

- Riders can be added to the policy to enable continued benefits if the insured returns to work part-time

![]()

Disability insurance provides income replacement if a worker is unable to work due to disability

Disability insurance is designed to replace a portion of a worker's income when they are unable to work due to a disability. It is a form of income protection that ensures individuals can continue to receive a wage despite being unable to work. This type of insurance is particularly relevant for those in the private sector, where there is no federal requirement for employers to provide paid sick leave.

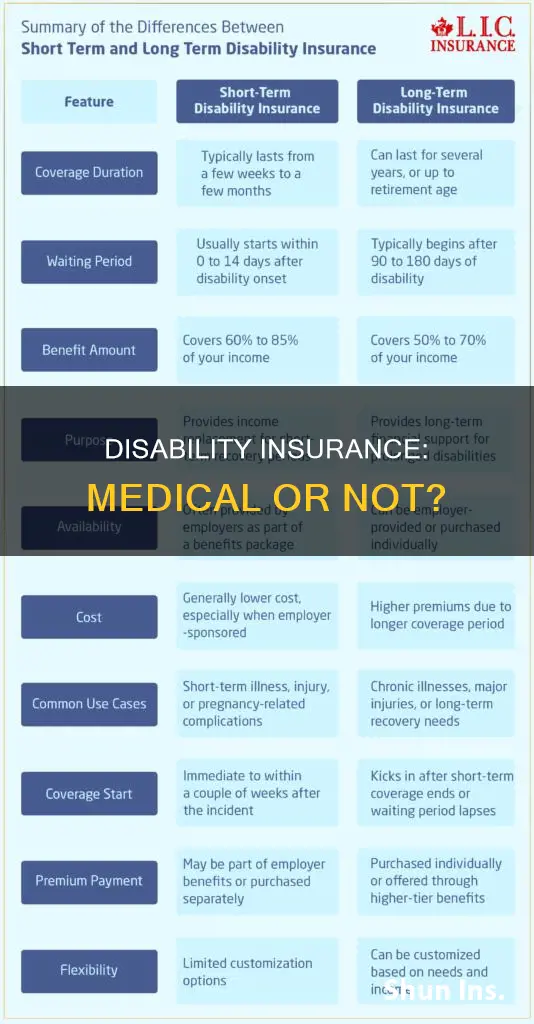

Disability insurance can be short-term or long-term, and the benefits are paid directly to the employee by the insurance company. Short-term disability insurance provides a percentage of pre-disability earnings on a weekly basis when employees are out of work due to a disability claim. This typically covers off-the-job accidents and illnesses that workers' compensation would not include. Short-term disability benefits can range from $50 to $1,681 per week for up to 52 weeks, depending on the employee's previous wages and the state in which they live. Some policies also allow employees to work part-time while receiving these benefits, although there may be income limitations, and employees may be required to pay back some of the benefits if they exceed these limits.

Some insurance providers also permit employees to work a different job while on short-term disability, as long as the job duties are significantly different from their primary occupation. However, if an employee's income from an alternate job exceeds a certain limit, the insurance provider may reduce, pause, or terminate the benefits. It is important to note that disability insurance does not provide job protection. While disability insurance can help protect an employee's income, it does not guarantee that their job will be held or available to return to.

Musicians' Health: Getting Medical Insurance as a Band

You may want to see also

Explore related products

![]()

It is available through public and private programs

Disability insurance is intended to replace some of a working person's lost income when a disability prevents them from working. It is available through public and private programs.

Public Programs

Social Security Disability Insurance (SSDI) is funded by taxes, so only adults with a work history who have earned enough work credits are eligible. The average SSDI payment for a disabled worker and their family is $1,892/month (as of 2012), which is generally far less than the worker earned when fully employed. Supplemental Security Income (SSI) is a program designed to assist low-income individuals who may have never worked or who haven't worked enough to earn sufficient work credits for SSDI.

Private Programs

Private disability insurance programs are paid for by an individual or offered as part of an employer's benefits package through monthly premiums. They are administered by large commercial insurers, who sell many types of plans with different eligibility requirements, limitations, and payouts. Private disability companies will often allow coverage for partial disability, whereas Social Security Disability requires that a person be totally disabled.

State-Sponsored Programs

Some states have state-sponsored disability plans that are funded by mandatory employee contributions. These include California, Hawaii, New Jersey, New York, and Rhode Island. Each state has different eligibility guidelines and details regarding how their programs are administered, including the length of time one must have been disabled before applying for benefits and what percentage of one's salary is payable.

Family Medical Insurance: Understanding the Cost and Coverage

You may want to see also

Explore related products

![]()

Qualification depends on the severity of the disability and its impact on work

Qualification for disability insurance depends on the severity of the disability and its impact on the policyholder's ability to work. The definition of "disability" varies across insurance providers, and this impacts how claims for benefits are judged. For instance, some providers define disability as the inability to perform any type of meaningful work, while others define it as the inability to perform the duties of one's own medical specialty. Still, others define it as the inability to perform the material and substantial duties of one's occupation, regardless of whether the insured decides to transition into another occupation.

The Social Security System, for example, requires applicants to demonstrate that their disability is expected to last for at least 12 months or result in death. Private plans, on the other hand, may only require applicants to demonstrate that they can no longer continue in the same line of work they were previously engaged in. The strictness of these requirements can impact the cost of the insurance plan, with more favourable terms typically resulting in higher insurance premiums.

To qualify for disability benefits, applicants must typically provide medical certification of their disability and meet certain income requirements. For example, they may need to demonstrate a certain level of income loss compared to their pre-disability earnings. Additionally, there may be an elimination period, which is the length of time the applicant must wait after becoming disabled before they can begin receiving benefits, as well as a benefit period that outlines how long those benefits will continue to be paid.

It is important to carefully review the terms and conditions of disability insurance plans, as the specific provisions can vary significantly. For physicians, in particular, there are unique considerations when assessing disability insurance options, such as the cost, definitions, and riders associated with the policy. By understanding the specific requirements and limitations of their disability insurance plan, individuals can ensure they have the necessary protection in the event of a disability.

Major Medical Insurance: AARP's Group Coverage Explained

You may want to see also

Explore related products

![]()

The cost depends on the plan's terms, benefit period, and definition of disability

The cost of disability insurance is influenced by several factors, including the plan's terms, benefit period, and definition of disability.

The plan's terms refer to the specific conditions and provisions outlined in the disability insurance policy. These terms can include various options and riders that enhance the coverage, such as cost-of-living adjustments or recovery benefits. The more comprehensive the plan's terms, the higher the cost is likely to be.

The benefit period is the length of time during which the policyholder can receive benefits. Disability insurance policies typically offer short-term or long-term coverage. Short-term disability insurance, often known as STD, provides income replacement for a shorter period, usually a few months to a year. On the other hand, long-term disability insurance can offer benefits until retirement age or until the individual recovers from their disability. The longer the benefit period, the higher the cost of the policy, as the insurer's risk increases.

The definition of disability also plays a role in determining the cost of disability insurance. The stricter the definition of disability, the higher the likelihood of an individual qualifying for benefits. A strict definition, such as the ADL standards, considers an individual disabled if they are unable to perform daily activities independently. This narrow definition increases the risk for the insurer, leading to potentially higher costs.

Additionally, the cost of disability insurance can be influenced by factors such as the individual's age, occupation, and medical history. The insurance company will assess these factors to determine the policy's price, taking into account the potential risks involved.

It is important to carefully review the terms, benefit period, and definition of disability when considering disability insurance to ensure that the coverage meets your specific needs and budget.

Becoming a Medicate Supplemental Insurance Provider: A Guide

You may want to see also

Explore related products

![]()

Riders can be added to the policy to enable continued benefits if the insured returns to work part-time

Disability insurance is intended to replace some of a working person's income when a disability prevents them from working. In the US, disability insurance does not provide job protection. However, job protection may be provided through other federal or state laws, such as the Family and Medical Leave Act (FMLA) or the California Family Rights Act (CFRA).

Riders, also known as addendums, can be added to insurance policies to provide additional coverage or benefits. They are a way to customise a policy to better suit an individual's needs. While not all insurance companies offer the same riders, and some are only available with certain types of policies, they can be a valuable way to ensure you are covered in a variety of circumstances.

One type of rider is the waiver of premium rider, which waives insurance premium payments if the policyholder becomes critically ill or physically impaired. This can be useful if an injury or illness prevents the policyholder from working in their traditional capacity. In the context of disability insurance, a waiver of premium rider could enable continued benefits if the insured returns to work part-time, as they may not be able to work to their full capacity and could still be incurring significant expenses for palliative care, personal finances, and living expenses.

Another type of rider is the accidental death rider, which provides a double benefit to take care of a surviving family's expenses. This type of rider can be ideal for the sole provider of a family, as it can cover the loss of income that would result from the policyholder's death.

It is important to note that riders typically come with additional costs and may have restrictions based on age, health, and pre-existing conditions. When considering adding a rider to an insurance policy, it is essential to understand the specific terms and conditions offered by the insurer.

Marketplace Insurance and Medicaid: Can You Have Both?

You may want to see also

Frequently asked questions

Disability insurance is a type of insurance that provides income if a worker is unable to work due to a disability.

Disability insurance compensates the policyholder for lost income due to a disability. The policyholder must satisfy certain conditions to receive these payments.

To qualify for government-sponsored disability insurance, applicants must prove that their disability is severe enough to prevent them from engaging in any meaningful work. Private plans may only require applicants to demonstrate that they can no longer work in their previous line of work.

The cost of disability insurance depends on factors such as the length of the elimination period, the benefit period, the definition of "disability", the amount of income to be replaced, and the medical history of the policyholder.

Disability insurance focuses on compensating lost income due to a disability, while medical insurance typically covers the costs of medical treatment and care services.