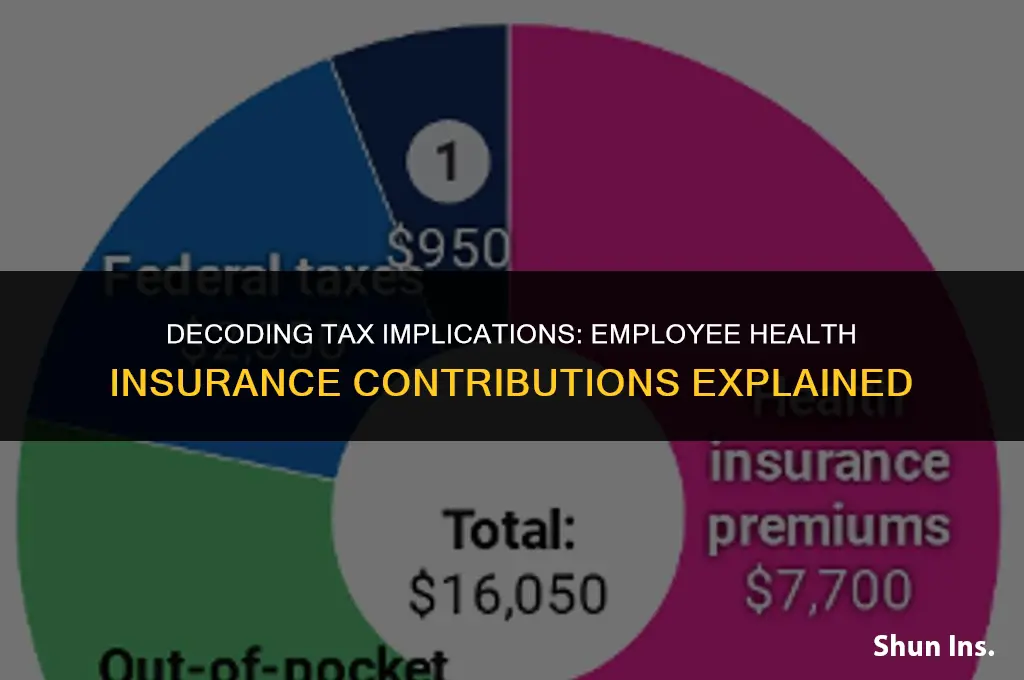

Employee contributions to health insurance are a common aspect of employment benefits, but understanding their tax implications can be complex. In many jurisdictions, such contributions are considered taxable income, subject to payroll taxes and income tax withholding. However, there are often specific rules and exceptions that can apply, such as the treatment of contributions under cafeteria plans or health savings accounts. Employers and employees alike must navigate these regulations to ensure compliance and optimize their tax situations. This paragraph will delve into the intricacies of employee health insurance contributions and their tax consequences, providing a comprehensive overview for those seeking to understand this important aspect of employee benefits.

| Characteristics | Values |

|---|---|

| Taxability | Generally taxable as income |

| Exceptions | Certain conditions may apply, such as employer-provided health insurance |

| Tax Code Reference | Internal Revenue Code (IRC) Section 106 |

| Employee Contribution Types | Premiums, co-pays, deductibles |

| Employer Contribution Types | Premiums, health savings accounts (HSAs) |

| Tax Implications for Employer | May be tax-deductible as a business expense |

| Tax Implications for Employee | Included in gross income, potentially affecting tax brackets |

| Health Insurance Types | Traditional, high-deductible health plans (HDHPs), health maintenance organizations (HMOs) |

| Impact on Employee Benefits | May reduce take-home pay, but provides health coverage |

| Impact on Employer Costs | Increases overall compensation costs, but may be offset by tax deductions |

| Legal Requirements | Compliance with Affordable Care Act (ACA) and other federal/state regulations |

| Recordkeeping | Employers must maintain records of contributions for tax reporting purposes |

| Reporting | Contributions reported on employee's W-2 form |

| State-Specific Rules | Some states may have additional or different tax rules regarding health insurance contributions |

| Changes in Tax Law | Recent tax reforms may have altered the taxability of certain health insurance contributions |

| Consultation | Employees and employers should consult tax professionals for specific guidance |

Explore related products

What You'll Learn

- General Taxability: Employee contributions to health insurance are generally not taxable as they're considered tax-free benefits

- Conditions for Tax-Free Status: Contributions must meet specific IRS conditions, such as being part of a qualified health plan

- Taxable Exceptions: Certain situations may render contributions taxable, like if the plan is not IRS-qualified or exceeds contribution limits

- Reporting Requirements: Employers must report health insurance contributions on employees' W-2 forms, even if they're tax-free

- State Tax Considerations: While federal tax rules apply, state tax laws may differ, and employees should check their state's regulations

![]()

General Taxability: Employee contributions to health insurance are generally not taxable as they're considered tax-free benefits

Employee contributions to health insurance are generally not taxable because they are considered tax-free benefits. This means that the money you pay towards your health insurance premiums is not subject to federal income tax, and in most cases, state income tax as well. This is a significant advantage for employees, as it reduces their overall tax burden and allows them to allocate more of their income towards other expenses or savings.

However, it's important to note that this tax-free status applies only to contributions made through a qualified employer-sponsored health plan. If you purchase health insurance independently, your contributions may not be tax-deductible. Additionally, if your employer provides you with a stipend or reimbursement for health insurance premiums, this may be considered taxable income.

There are also some exceptions to the general rule of tax-free contributions. For example, if you are a highly compensated employee, your contributions may be subject to taxation if they exceed a certain threshold. Furthermore, if you receive a subsidy from the government to help pay for your health insurance premiums, this subsidy may be taxable.

In conclusion, while employee contributions to health insurance are generally not taxable, there are some important exceptions and nuances to be aware of. It's always a good idea to consult with a tax professional or your employer's benefits administrator to ensure that you understand the specific tax implications of your health insurance contributions.

Insurance: Beyond Accidents, a Safety Net for Life

You may want to see also

Explore related products

![]()

Conditions for Tax-Free Status: Contributions must meet specific IRS conditions, such as being part of a qualified health plan

To qualify for tax-free status, employee contributions to health insurance must adhere to specific conditions set forth by the Internal Revenue Service (IRS). One of the primary requirements is that the contributions must be part of a qualified health plan. This typically includes plans that are sponsored by an employer and meet certain criteria regarding coverage, cost-sharing, and eligibility.

In addition to being part of a qualified health plan, the contributions must also be used to pay for medical expenses that are considered eligible under the plan. This may include premiums, deductibles, copayments, and coinsurance, but not expenses that are covered by other insurance policies or paid out-of-pocket.

Another important condition is that the contributions must be made on a pre-tax basis, meaning that they are deducted from the employee's gross income before taxes are calculated. This is often done through payroll deductions, where the employee elects to have a certain amount withheld from their paycheck each pay period.

It's also worth noting that there are limits to the amount of tax-free contributions an employee can make each year. These limits are set by the IRS and are adjusted annually for inflation. For example, in 2023, the maximum tax-free contribution for an individual is $3,650, while the maximum for a family is $7,300.

Finally, employees should be aware that if they receive a refund or reimbursement for their health insurance contributions, this amount may be considered taxable income. This is because the refund or reimbursement is essentially a return of previously tax-free funds, and therefore must be reported as income on the employee's tax return.

In summary, employee contributions to health insurance can be tax-free if they meet specific IRS conditions, such as being part of a qualified health plan, used for eligible medical expenses, made on a pre-tax basis, and within the annual contribution limits. However, employees should be cautious of refunds or reimbursements, as these may be considered taxable income.

Understanding Medical Co-Insurance: Your Costs and Coverage Explained

You may want to see also

Explore related products

![]()

Taxable Exceptions: Certain situations may render contributions taxable, like if the plan is not IRS-qualified or exceeds contribution limits

Contributions to health insurance plans are generally considered taxable if they do not meet specific IRS criteria. One key exception is when the plan is not IRS-qualified. In such cases, the contributions may be subject to taxation because they do not adhere to the strict guidelines set forth by the IRS. This can include plans that do not provide adequate coverage, fail to meet actuarial standards, or do not comply with reporting requirements.

Another situation that may render contributions taxable is when they exceed the contribution limits set by the IRS. These limits are in place to ensure that individuals do not over-contribute to their health insurance plans and thereby reduce their taxable income. Exceeding these limits can result in the excess contributions being taxed as ordinary income.

It is important to note that these taxable exceptions apply to both employer and employee contributions. Employers who contribute to non-IRS-qualified plans or exceed contribution limits may be subject to penalties and taxes. Employees who make contributions to such plans may also be taxed on the excess contributions.

To avoid these taxable exceptions, it is crucial for employers and employees to carefully review their health insurance plans and ensure that they meet IRS criteria. This includes verifying that the plan is IRS-qualified and that contributions do not exceed the established limits. By doing so, individuals can minimize their tax liability and ensure that their health insurance contributions are used effectively.

In conclusion, taxable exceptions for health insurance contributions can be avoided by ensuring that plans are IRS-qualified and that contributions do not exceed established limits. By understanding these exceptions and taking appropriate precautions, employers and employees can make informed decisions about their health insurance plans and minimize their tax liability.

Understanding Health Insurance Providers: Your Guide to Choosing the Right One

You may want to see also

Explore related products

![]()

Reporting Requirements: Employers must report health insurance contributions on employees' W-2 forms, even if they're tax-free

Employers are required to report health insurance contributions on employees' W-2 forms, regardless of whether these contributions are tax-free. This reporting requirement is crucial for both employers and employees to ensure compliance with tax regulations and to accurately reflect the compensation provided.

The W-2 form is an annual tax document that employers must send to their employees and the Internal Revenue Service (IRS) at the end of the year. It reports an employee's annual wages and the amount of taxes withheld from their paycheck. In addition to wages, the W-2 form also includes information about employer-provided benefits, such as health insurance.

Even if the employer's contributions to the employee's health insurance plan are tax-free, they must still be reported on the W-2 form. This is because the IRS considers these contributions as part of the employee's total compensation. By reporting these contributions, employers provide employees with a complete picture of their earnings and benefits, which is essential for filing their own tax returns accurately.

Failure to report health insurance contributions on the W-2 form can result in penalties for both employers and employees. Employers may face fines for non-compliance with tax reporting requirements, while employees may encounter issues when filing their tax returns or applying for government benefits that rely on their reported income.

To ensure proper reporting, employers should carefully review the instructions for completing the W-2 form and consult with a tax professional if needed. Employees should also verify the accuracy of the information reported on their W-2 forms and contact their employer if they notice any discrepancies.

In summary, reporting health insurance contributions on employees' W-2 forms is a critical aspect of tax compliance for both employers and employees. It ensures that all parties have a clear understanding of the compensation provided and helps to avoid potential tax-related issues down the line.

Why Insurance Companies Demand Letters of Credit: A Comprehensive Guide

You may want to see also

Explore related products

![]()

State Tax Considerations: While federal tax rules apply, state tax laws may differ, and employees should check their state's regulations

While federal tax rules provide a broad framework for determining the taxability of employee contributions to health insurance, state tax laws can introduce significant variations. It's crucial for employees to understand that the tax implications of their health insurance contributions may differ depending on their state of residence. For instance, some states may exempt certain types of health insurance premiums from state income tax, while others may have specific deductions or credits available.

To navigate these differences effectively, employees should consult their state's tax regulations or seek guidance from a tax professional familiar with state-specific rules. This is particularly important for individuals who work in multiple states or have complex tax situations. By doing so, they can ensure they are taking advantage of any available tax benefits and are in compliance with state tax laws.

Moreover, employees should be aware that state tax laws can change over time, potentially affecting the taxability of their health insurance contributions. Staying informed about these changes is essential to avoid unexpected tax liabilities or missed opportunities for tax savings. Regularly reviewing state tax updates and consulting with a tax advisor can help employees adapt to these changes and make informed decisions about their health insurance contributions.

In conclusion, while federal tax rules set the baseline for the taxability of employee contributions to health insurance, state tax laws can significantly impact the overall tax picture. Employees must be proactive in understanding and complying with their state's tax regulations to optimize their tax situation and avoid potential penalties.

Strategies to Drop UB Medical Insurance Coverage

You may want to see also

Frequently asked questions

Generally, employee contributions to health insurance are not taxable if they are made on a pre-tax basis through a cafeteria plan or other qualified arrangement.

If the employee contributions are made post-tax, they may be tax-deductible as a medical expense on the employee's individual tax return, subject to certain limits and conditions.

Yes, there are some exceptions. For example, if the employee is a highly compensated individual or if the plan is not properly structured, the contributions may be taxable.

The ACA does not directly impact the taxability of employee health insurance contributions. However, it does impose certain requirements on health plans, which may affect the structure of employee contributions.

Yes, employees should consult a tax professional to understand the tax implications of their health insurance contributions based on their individual circumstances and the specific plan they are enrolled in.