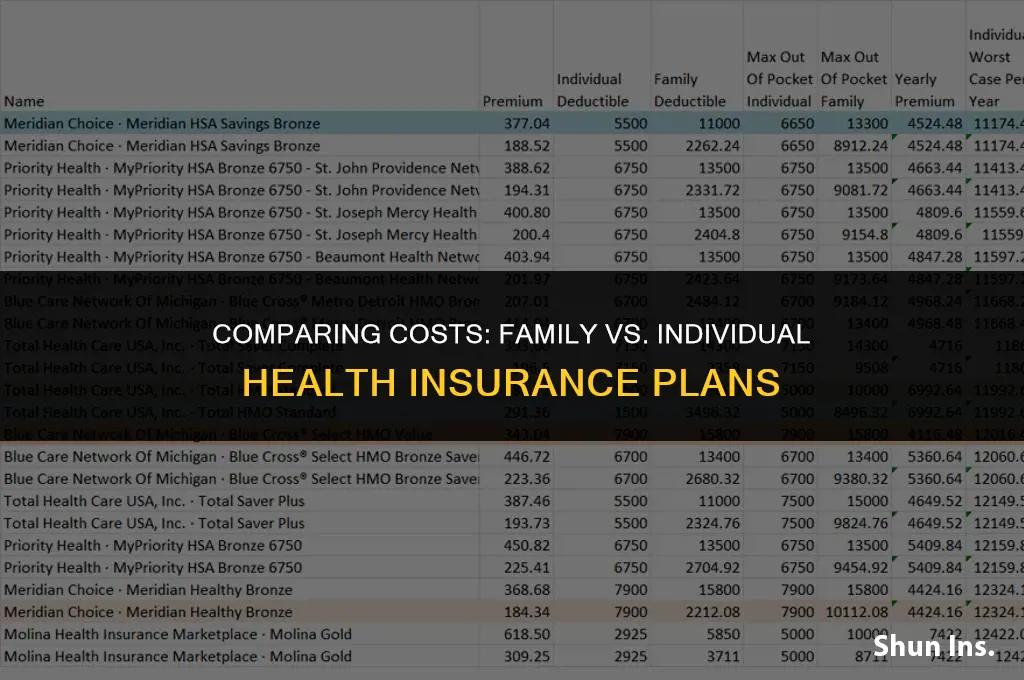

When considering the cost-effectiveness of health insurance, many individuals and families ponder whether opting for a family plan is more economical than purchasing individual policies. The answer to this question can be complex and depends on various factors, including the number of family members, their ages, health statuses, and the specific insurance plans available. Generally, family health insurance plans can offer a lower per-person premium compared to individual plans, especially when insuring multiple family members. However, it's essential to weigh the total cost of a family plan against the combined premiums of individual policies to determine the most cost-efficient option for a particular household. Additionally, factors such as deductible amounts, co-pays, and coverage limits should be carefully evaluated to ensure that the chosen plan meets the family's healthcare needs while providing the best value for money.

Explore related products

What You'll Learn

- Cost Comparison: Evaluate the total cost of family vs. individual plans, including premiums and out-of-pocket expenses

- Coverage Differences: Explore the variations in coverage between family and individual health insurance policies

- Eligibility Criteria: Understand the requirements to qualify for family health insurance versus individual plans

- Benefits Analysis: Assess the advantages and disadvantages of each type of health insurance plan

- Market Trends: Investigate current market trends and how they impact the affordability of family vs. individual health insurance

![]()

Cost Comparison: Evaluate the total cost of family vs. individual plans, including premiums and out-of-pocket expenses

Evaluating the total cost of family versus individual health insurance plans requires a detailed analysis of both premiums and out-of-pocket expenses. Premiums are the monthly or annual payments made to the insurance provider, while out-of-pocket expenses include deductibles, copayments, and coinsurance. To determine which plan is more cost-effective, it's essential to consider the specific needs and circumstances of the individuals involved.

One approach to comparing costs is to calculate the total annual expenditure for each plan. This involves multiplying the monthly premium by 12 and adding the estimated out-of-pocket expenses. For family plans, it's crucial to consider the number of family members and their ages, as these factors can significantly impact the premium cost. Younger family members typically have lower premiums, while older members may have higher premiums due to increased health risks.

Individual plans, on the other hand, are tailored to a single person's needs and may offer more flexibility in terms of coverage options. However, they may also come with higher premiums, especially for older individuals or those with pre-existing health conditions. When comparing costs, it's important to consider the trade-off between premium savings and potential out-of-pocket expenses.

A practical tip for evaluating costs is to use online insurance comparison tools or consult with a licensed insurance agent. These resources can provide personalized quotes and help individuals understand the nuances of different plans. Additionally, it's essential to review the plan's Summary of Benefits and Coverage (SBC) to gain a comprehensive understanding of the covered services and associated costs.

In conclusion, determining whether a family or individual health insurance plan is more cost-effective requires a thorough analysis of premiums and out-of-pocket expenses. By considering the specific needs and circumstances of the individuals involved and utilizing available resources, individuals can make an informed decision that best suits their financial and healthcare needs.

Medical Insurance Abroad: What's Covered and What's Not

You may want to see also

Explore related products

![]()

Coverage Differences: Explore the variations in coverage between family and individual health insurance policies

Family health insurance policies typically offer a broader range of coverage options compared to individual policies. This is because family plans are designed to cater to the diverse needs of multiple family members, often including children, parents, and sometimes even extended family members. As a result, family policies may include additional benefits such as pediatric care, maternity coverage, and dependent care services that are not always available in individual plans.

One significant coverage difference between family and individual health insurance policies is the inclusion of preventive care services. Family plans often emphasize preventive care, offering comprehensive coverage for routine check-ups, vaccinations, and screenings for all family members. This focus on prevention can lead to better overall health outcomes for families and may also result in lower long-term healthcare costs.

Another key variation in coverage is the treatment of pre-existing conditions. Family health insurance policies may provide more comprehensive coverage for pre-existing conditions, as they are designed to accommodate the health needs of multiple individuals, some of whom may have chronic illnesses or disabilities. In contrast, individual policies may have more stringent requirements or exclusions for pre-existing conditions, which can limit coverage options for individuals with ongoing health issues.

Family health insurance policies also tend to offer more flexibility in terms of provider choice. Because family plans are meant to serve the needs of multiple family members, they often have larger provider networks, allowing families to choose from a wider range of healthcare professionals and facilities. This can be particularly important for families with children, as they may need to access specialized pediatric care or services that are only available through certain providers.

In summary, the coverage differences between family and individual health insurance policies are significant and can have a major impact on the healthcare options available to policyholders. Family plans generally offer broader coverage, including additional benefits, a greater emphasis on preventive care, more comprehensive treatment for pre-existing conditions, and increased flexibility in provider choice. These factors can make family health insurance a more attractive option for those looking to ensure the health and well-being of their entire family.

Navigating FAFSA: A Guide to Waiving Health Insurance Requirements

You may want to see also

Explore related products

![]()

Eligibility Criteria: Understand the requirements to qualify for family health insurance versus individual plans

To qualify for family health insurance, you typically need to meet specific eligibility criteria that differ from those for individual plans. Family plans usually require that you have a qualifying relationship with the other individuals you wish to insure, such as being a spouse, parent, or dependent. Additionally, family plans may have age restrictions, often requiring that dependents be under a certain age, typically 26, unless they are disabled or meet other special circumstances.

In contrast, individual health insurance plans do not require you to have a qualifying relationship with anyone else, and they generally do not have age restrictions for dependents. However, individual plans may have different eligibility criteria based on factors such as your employment status, income level, or health condition. For example, some individual plans may only be available to those who are self-employed or who do not have access to employer-sponsored health insurance.

When comparing family and individual health insurance plans, it's important to consider not only the eligibility criteria but also the cost and coverage. Family plans may be more cost-effective if you have multiple dependents, as they often provide a lower premium per person compared to individual plans. However, the total cost of a family plan may still be higher than that of an individual plan, depending on the number of people covered and the specific plan details.

In terms of coverage, family plans typically offer the same benefits to all covered individuals, whereas individual plans may allow for more customization of coverage based on individual needs. For example, an individual plan may offer more options for dental or vision coverage, or it may provide more comprehensive mental health benefits.

Ultimately, the decision between a family and individual health insurance plan depends on your specific circumstances, including your family size, income level, and health needs. It's important to carefully evaluate the eligibility criteria, cost, and coverage of both types of plans before making a decision.

Private Medical Insurance: Pre-Existing Conditions Covered?

You may want to see also

Explore related products

![]()

Benefits Analysis: Assess the advantages and disadvantages of each type of health insurance plan

When evaluating the benefits of different health insurance plans, it's crucial to consider both the advantages and disadvantages of each type. Family health insurance plans often provide comprehensive coverage for all family members under a single policy, which can simplify the insurance process and potentially reduce administrative costs. However, the premiums for family plans are typically higher than those for individual plans, as they cover more people and often include more extensive benefits.

One significant advantage of family health insurance is the convenience it offers. Managing a single policy for the entire family can be less complicated than maintaining separate policies for each member. This can be particularly beneficial for families with children, as it ensures that all dependents are covered under the same plan. Additionally, family plans may offer better value for money, as the cost per person is usually lower compared to purchasing individual policies for each family member.

On the other hand, individual health insurance plans provide more flexibility and customization options. Individuals can choose plans that cater specifically to their health needs and budget constraints. This can be advantageous for young adults or individuals without dependents, as they may not require the same level of coverage as a family. However, the downside of individual plans is that they can be more expensive per person, especially for those with pre-existing health conditions.

Another factor to consider is the potential for cost-sharing within a family plan. Some plans allow family members to share deductibles and out-of-pocket expenses, which can help to reduce the overall financial burden on the family. This cost-sharing feature is not typically available with individual plans, as each policyholder is responsible for their own expenses.

In conclusion, the choice between family and individual health insurance plans depends on various factors, including the size of the family, the health needs of the members, and the budget available for insurance premiums. While family plans offer convenience and potential cost savings, individual plans provide more flexibility and customization options. A thorough benefits analysis is essential to determine which type of plan best suits the specific needs of a family or individual.

Exploring Cigna: Your Guide to Private Health Insurance Options

You may want to see also

Explore related products

$17.99

![]()

Market Trends: Investigate current market trends and how they impact the affordability of family vs. individual health insurance

The current market trends in health insurance reveal a complex landscape that impacts the affordability of family versus individual health insurance in various ways. One significant trend is the increasing cost of healthcare services, which is driven by factors such as inflation, advancements in medical technology, and the rising cost of pharmaceuticals. This trend affects both family and individual health insurance plans, but it can have a more pronounced impact on family plans due to the higher number of beneficiaries.

Another key trend is the shift towards high-deductible health plans (HDHPs), which are becoming increasingly popular among employers and individuals. HDHPs typically have lower premiums but higher out-of-pocket costs, which can make them more affordable for individuals but potentially more costly for families who may need to cover multiple deductibles. Additionally, the growth of the gig economy and the rise of independent contractors have led to an increase in the number of individuals seeking health insurance outside of employer-sponsored plans, further influencing the market dynamics.

The Affordable Care Act (ACA) has also played a significant role in shaping the health insurance market. While the ACA has expanded access to health insurance for many individuals and families, it has also introduced new regulations and requirements that can impact the cost of insurance. For example, the ACA's individual mandate, which requires most individuals to have health insurance or pay a penalty, has been repealed, potentially leading to changes in the risk pool and premium costs.

Furthermore, the increasing use of telemedicine and digital health services is transforming the way healthcare is delivered and paid for. This trend can lead to cost savings for both individuals and families, as it allows for more convenient and often less expensive access to healthcare services. However, the adoption of these technologies can also vary by region and demographic, potentially creating disparities in access and affordability.

In conclusion, the current market trends in health insurance are characterized by rising healthcare costs, the popularity of HDHPs, the impact of the ACA, and the growth of digital health services. These trends can have different implications for the affordability of family versus individual health insurance, highlighting the importance of carefully considering the specific needs and circumstances of each household when selecting a health insurance plan.

Get Medical Insurance in PA: A Step-by-Step Guide

You may want to see also

Frequently asked questions

Family health insurance can be more cost-effective than purchasing individual plans for each family member. Insurance companies often offer discounts for family plans, and having a single plan can simplify administration and potentially reduce overall premiums.

The cost of family health insurance typically depends on the number of family members covered and their ages. While it may be cheaper per person to have a family plan, the total cost will be higher than an individual plan due to the inclusion of multiple people. However, family plans often provide better value, especially when considering the health needs and potential subsidies for children.

When choosing between family health insurance and individual health insurance, consider factors such as the health needs of each family member, the total cost of premiums, potential subsidies or discounts, the convenience of managing a single plan versus multiple plans, and the flexibility of coverage options. It's also important to compare the benefits and limitations of each plan to ensure that all family members' healthcare needs are adequately met.