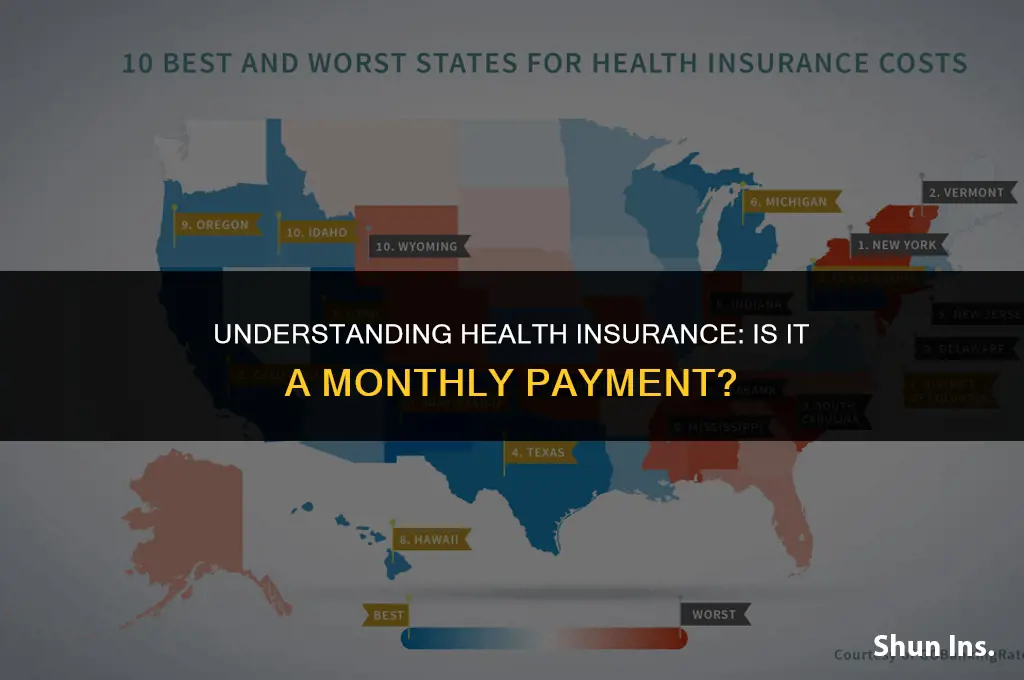

Health insurance is a crucial aspect of financial planning, and understanding its payment structure is essential for many individuals and families. One common question that arises is whether health insurance requires a monthly payment. The answer to this question can vary depending on several factors, including the type of health insurance plan, the insurance provider, and the individual's employment status. In general, health insurance can be paid for on a monthly basis, but there are also options for annual or quarterly payments. Additionally, some employers may offer health insurance as a benefit, in which case the payment structure may be different. It's important to carefully review the terms of any health insurance plan to understand the payment requirements and ensure that it fits within one's budget and financial goals.

Explore related products

What You'll Learn

- Types of Health Insurance Plans: Explore different plans like HMO, PPO, EPO, and POS

- Factors Affecting Premiums: Understand how age, health status, and location impact monthly payments

- Coverage and Benefits: Review what services and treatments are included in various insurance plans

- Out-of-Pocket Costs: Learn about deductibles, copays, and coinsurance in addition to premiums

- Subsidies and Financial Aid: Discover options for reducing costs through subsidies, tax credits, or Medicaid

![]()

Types of Health Insurance Plans: Explore different plans like HMO, PPO, EPO, and POS

Health insurance plans can be categorized into several types, each with its own set of benefits and limitations. Understanding these differences is crucial when deciding which plan is right for you. Here's a breakdown of the most common types of health insurance plans:

Health Maintenance Organizations (HMOs) are one of the most popular types of health insurance plans. They typically offer lower premiums and out-of-pocket costs in exchange for a more limited network of providers. With an HMO, you'll need to choose a primary care physician (PCP) who will coordinate your care and refer you to specialists within the network when necessary. HMOs often require pre-authorization for certain procedures and may not cover out-of-network care except in emergencies.

Preferred Provider Organizations (PPOs) offer more flexibility than HMOs. They have a network of preferred providers, but you can also see out-of-network providers at a higher cost. PPOs typically have higher premiums than HMOs, but they also offer more comprehensive coverage. Unlike HMOs, PPOs do not require you to choose a PCP, and you can see specialists without a referral. However, you'll need to meet a deductible before your coverage kicks in, and you may need to pay a coinsurance for certain procedures.

Exclusive Provider Organizations (EPOs) are similar to HMOs in that they offer lower premiums and out-of-pocket costs in exchange for a limited network of providers. However, EPOs do not require you to choose a PCP, and you can see specialists without a referral. EPOs often have a deductible and coinsurance, but they may also cover some out-of-network care.

Point of Service (POS) plans are a hybrid of HMOs and PPOs. They offer lower premiums and out-of-pocket costs like HMOs, but they also allow you to see out-of-network providers at a higher cost like PPOs. With a POS plan, you'll need to choose a PCP who will coordinate your care and refer you to specialists within the network when necessary. However, you can also see out-of-network specialists without a referral, although you'll pay more for this care.

When choosing a health insurance plan, it's important to consider your individual needs and preferences. If you're looking for lower premiums and don't mind a more limited network of providers, an HMO or EPO may be a good choice. If you need more flexibility and are willing to pay higher premiums, a PPO or POS plan may be a better fit. Be sure to carefully review the details of each plan, including the network of providers, deductibles, coinsurance, and out-of-pocket maximums, before making a decision.

Maryland's Free Health Insurance: A Step-by-Step Application Guide

You may want to see also

Explore related products

![]()

Factors Affecting Premiums: Understand how age, health status, and location impact monthly payments

Age is a significant factor in determining health insurance premiums. Younger individuals typically have lower premiums due to their generally better health and lower risk of chronic conditions. As people age, their premiums tend to increase as the likelihood of health issues rises. For example, a 25-year-old might pay significantly less per month compared to a 55-year-old for the same coverage.

Health status also plays a crucial role in premium calculations. Individuals with pre-existing conditions, such as diabetes, heart disease, or cancer, may face higher premiums due to the increased cost of their care. Insurance companies often require medical underwriting, which involves assessing an applicant's health history to determine their risk profile. The higher the risk, the higher the premium.

Location is another key factor affecting health insurance premiums. The cost of healthcare varies significantly from one region to another, influenced by factors such as the local economy, healthcare provider fees, and the overall health of the population. For instance, someone living in a major city with high healthcare costs might pay more per month than someone living in a rural area with lower costs.

Understanding these factors can help individuals make informed decisions when choosing health insurance. By recognizing how age, health status, and location impact premiums, one can better navigate the complex landscape of health insurance and find a plan that fits their needs and budget.

Anxiety and Travel Insurance: What's Covered Medically?

You may want to see also

Explore related products

![]()

Coverage and Benefits: Review what services and treatments are included in various insurance plans

Health insurance plans can vary significantly in terms of coverage and benefits. It's essential to review what services and treatments are included in various insurance plans to ensure you're getting the best value for your monthly payments. Some plans may cover preventive care, such as annual check-ups and vaccinations, while others may not. Additionally, the coverage for prescription medications, mental health services, and specialized treatments can differ greatly between plans.

When reviewing insurance plans, it's important to consider your individual health needs and those of your dependents. For example, if you have a chronic condition that requires ongoing treatment, you'll want to ensure that the plan covers the necessary medications and therapies. Similarly, if you're planning to start a family, you'll want to look for a plan that includes maternity and newborn care.

Another factor to consider is the cost-sharing structure of the plan. This includes the deductible, copayments, and coinsurance. A plan with a lower monthly premium may have higher out-of-pocket costs, while a plan with a higher premium may cover more of your healthcare expenses. It's important to weigh the costs and benefits of each plan to determine which one is the most cost-effective for your situation.

When comparing insurance plans, it's also important to consider the provider network. Some plans may have a limited network of healthcare providers, while others may offer a wider range of options. If you have a preferred doctor or hospital, you'll want to ensure that they're included in the plan's network. Additionally, if you travel frequently, you may want to consider a plan that offers coverage for out-of-network care.

Finally, it's important to review the plan's exclusions and limitations. Some plans may exclude certain treatments or services, such as cosmetic surgery or alternative therapies. Others may have limits on the number of visits or treatments covered per year. By understanding these exclusions and limitations, you can avoid unexpected costs and ensure that you're getting the most out of your health insurance plan.

Decoding the H&R Block Query on Health Insurance: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Out-of-Pocket Costs: Learn about deductibles, copays, and coinsurance in addition to premiums

Understanding out-of-pocket costs is crucial when navigating the complexities of health insurance. These costs, which include deductibles, copays, and coinsurance, can significantly impact your financial well-being if not managed properly. Let's delve into each of these components to provide a comprehensive overview.

Deductibles are the amount you must pay out of pocket before your insurance coverage kicks in. For instance, if you have a deductible of $1,000, you will need to pay the first $1,000 of your medical expenses before your insurance starts covering the costs. Deductibles can vary widely depending on your insurance plan, and it's essential to choose a plan with a deductible that aligns with your financial capabilities.

Copays, on the other hand, are fixed amounts you pay for specific services or medications, regardless of the total cost. For example, you might have a copay of $20 for a doctor's visit or $10 for a prescription medication. Copays are typically lower for in-network providers and can be significantly higher for out-of-network services. Understanding your copay structure can help you make informed decisions about where to seek care.

Coinsurance is the percentage of the cost of a covered service that you are responsible for paying after you've met your deductible. For example, if your coinsurance is 20%, you will pay 20% of the cost of a service, and your insurance will cover the remaining 80%. Coinsurance rates can vary depending on the type of service and your insurance plan. It's important to note that coinsurance can add up quickly, especially for expensive medical procedures.

In addition to these out-of-pocket costs, premiums are the monthly payments you make to maintain your health insurance coverage. Premiums can vary based on factors such as your age, health status, and the level of coverage you choose. While premiums are a significant aspect of health insurance, they are not the only cost you need to consider.

To effectively manage your health insurance costs, it's essential to consider all these factors together. By understanding deductibles, copays, coinsurance, and premiums, you can make informed decisions about your healthcare and choose a plan that best fits your needs and budget. Remember, health insurance is not just a monthly payment; it's a comprehensive financial strategy that requires careful consideration of all potential costs.

Understanding Obamacare: Is It Health Insurance or Something Else?

You may want to see also

Explore related products

![]()

Subsidies and Financial Aid: Discover options for reducing costs through subsidies, tax credits, or Medicaid

Navigating the complex landscape of health insurance costs can be daunting, but there are several strategies to mitigate expenses. One such approach is to explore subsidies and financial aid options, which can significantly reduce the financial burden of health coverage. Subsidies are monetary assistance provided by the government or private organizations to help individuals afford health insurance premiums. These subsidies can come in various forms, including tax credits, which reduce the amount of taxes owed, and direct payments to insurance providers.

Medicaid is another crucial avenue for financial assistance, particularly for low-income individuals and families. This government program provides free or low-cost health coverage to eligible recipients, ensuring that those with limited financial resources have access to essential healthcare services. To qualify for Medicaid, individuals must meet specific income and asset criteria, which vary by state.

When seeking subsidies or financial aid, it's essential to understand the eligibility requirements and application processes. For instance, tax credits are often available to those who purchase insurance through a health insurance exchange and meet certain income thresholds. Applicants must fill out the necessary forms and provide documentation to verify their income and other relevant information.

Moreover, it's important to be aware of the potential pitfalls and common mistakes when applying for financial aid. For example, failing to report all sources of income or incorrectly estimating future earnings can lead to ineligibility or the need to repay received assistance. To avoid such issues, applicants should carefully review the application instructions and seek guidance from healthcare professionals or financial advisors if needed.

In conclusion, subsidies and financial aid can play a vital role in making health insurance more affordable. By understanding the available options and navigating the application process effectively, individuals can reduce their healthcare costs and ensure they have access to the care they need.

Finding Medical Insurance Information: A Step-by-Step Guide

You may want to see also

Frequently asked questions

Yes, health insurance premiums are commonly paid on a monthly basis. This regular payment structure helps spread out the cost over the year, making it more manageable for policyholders.

It depends on the insurance provider and the specific plan. Some insurers offer the option to pay premiums annually, which can sometimes result in a discount compared to monthly payments.

Missing a monthly health insurance payment can lead to a lapse in coverage. It's important to make timely payments to ensure continuous protection. If you miss a payment, contact your insurer immediately to discuss options for reinstating coverage.

Some health insurance providers may offer alternative payment frequencies like quarterly or semi-annually. However, this is not as common as monthly payments, and availability varies by insurer and plan.