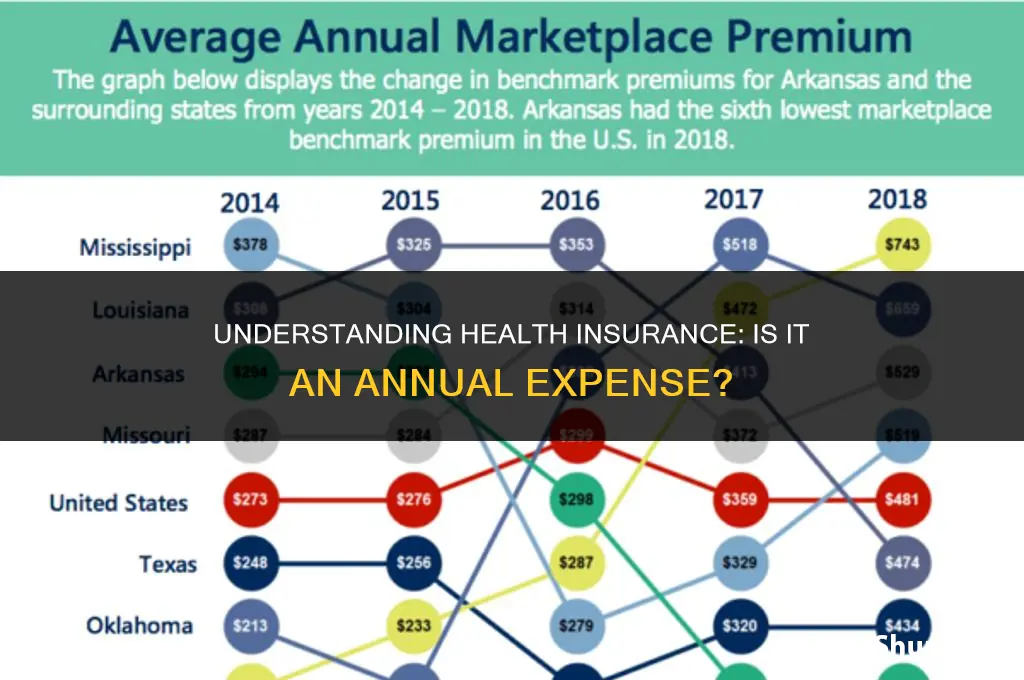

Health insurance is a crucial aspect of financial planning, and understanding its cost structure is essential for individuals and families alike. One common question that arises is whether health insurance is an annual expense. The answer to this question can have significant implications for budgeting and financial forecasting. In this article, we will delve into the details of health insurance premiums, exploring the factors that influence their frequency and amount. By the end, readers will have a clear understanding of whether health insurance is an annual expense and how to best manage this important financial commitment.

Explore related products

What You'll Learn

- Premiums: Regular payments made to maintain health insurance coverage throughout the year

- Deductibles: Amounts paid out-of-pocket before insurance benefits kick in, typically annual

- Coverage Period: Most health insurance policies renew annually, ensuring continuous coverage

- Tax Implications: Health insurance premiums can be tax-deductible, reducing annual taxable income

- Policy Changes: Insurers may update policy terms, coverage, and costs at the end of each policy year

![]()

Premiums: Regular payments made to maintain health insurance coverage throughout the year

Health insurance premiums are a critical component of maintaining coverage throughout the year. These regular payments ensure that your health insurance policy remains active, providing you with the necessary financial protection against medical expenses. Premiums are typically paid monthly, quarterly, or annually, depending on the policy and the insurer's requirements.

The amount of your premium is determined by several factors, including your age, health status, the type of coverage you choose, and your location. Younger individuals generally pay lower premiums, as they are considered to be at lower risk for health issues. Conversely, older individuals may face higher premiums due to the increased likelihood of requiring medical care. Additionally, the type of coverage you select—whether it's a basic plan or a more comprehensive one—will also impact your premium amount.

It's important to note that premiums are not the only cost associated with health insurance. Policyholders may also be responsible for deductibles, copayments, and coinsurance, which are additional expenses that come into play when receiving medical care. However, premiums are a fixed cost that you can budget for in advance, unlike other health-related expenses that may arise unexpectedly.

To make the most of your health insurance, it's essential to understand your policy's terms and conditions, including the premium payment schedule. This will help you avoid any lapses in coverage due to missed payments. Additionally, it's a good idea to review your policy annually to ensure that it still meets your healthcare needs and budget constraints. By staying informed and proactive, you can effectively manage your health insurance premiums and maintain the financial security they provide.

Should You Avoid Health Insurance? Pros, Cons, and Risks Explained

You may want to see also

Explore related products

![]()

Deductibles: Amounts paid out-of-pocket before insurance benefits kick in, typically annual

In the realm of health insurance, deductibles represent the initial financial hurdle that policyholders must clear before their insurance coverage begins to take effect. This out-of-pocket expense is typically an annual requirement, meaning that insured individuals must pay this amount each year before their insurance benefits kick in. Understanding the nature and implications of deductibles is crucial for anyone seeking to navigate the complex landscape of health insurance.

One key aspect of deductibles is that they can vary significantly depending on the specific insurance plan. Some plans may have relatively low deductibles, making them more accessible for individuals who may not have substantial savings to cover upfront costs. Conversely, plans with higher deductibles may offer lower monthly premiums, presenting a trade-off between immediate out-of-pocket expenses and long-term financial commitments. Policyholders must carefully consider their financial situations and health care needs when selecting a plan with a deductible that aligns with their budget and expectations.

Moreover, it is essential to recognize that deductibles are just one component of the overall cost of health insurance. In addition to the deductible, insured individuals may also be responsible for copayments, coinsurance, and other out-of-pocket expenses. These additional costs can accumulate quickly, particularly for those with chronic health conditions or who require frequent medical attention. As such, it is important for policyholders to have a comprehensive understanding of all the potential costs associated with their insurance plan, including the deductible, to avoid unexpected financial burdens.

Furthermore, the concept of deductibles intersects with the broader question of whether health insurance is an annual expense. While deductibles are indeed typically an annual requirement, the overall cost of health insurance can be influenced by a variety of factors, including changes in health status, shifts in employment, or alterations to insurance plan offerings. Policyholders must remain vigilant and adapt their insurance coverage as needed to ensure that they are adequately protected against unforeseen health care costs.

In conclusion, deductibles play a significant role in the structure and financial implications of health insurance plans. By understanding the nature of deductibles and their impact on overall health care costs, insured individuals can make informed decisions about their insurance coverage and better prepare for the financial responsibilities that come with maintaining their health and well-being.

Navigating Medical Insurance Options Outside of Special Enrollment Periods

You may want to see also

Explore related products

![]()

Coverage Period: Most health insurance policies renew annually, ensuring continuous coverage

Most health insurance policies are designed to renew annually, which ensures that policyholders have continuous coverage without any gaps. This annual renewal process is a critical aspect of maintaining health insurance, as it allows individuals to keep their protection up-to-date and adapt to any changes in their health status or insurance needs.

The coverage period typically starts on the date of the policy's effective date and ends on the renewal date the following year. During this time, the policyholder is responsible for paying premiums to keep the coverage active. If premiums are not paid, the policy may lapse, resulting in a loss of coverage.

Annual renewals also provide an opportunity for policyholders to review their coverage and make any necessary changes. This could include updating personal information, adjusting coverage levels, or switching to a different insurance provider. It's essential to carefully review the terms and conditions of the policy during the renewal process to ensure that it still meets the individual's needs.

One of the benefits of annual renewals is that they allow insurance companies to reassess the policyholder's risk profile and adjust premiums accordingly. This means that individuals who have had a change in their health status, such as a new diagnosis or a significant improvement in their condition, may see their premiums increase or decrease as a result.

In some cases, policyholders may be able to renew their coverage for a shorter period, such as six months, if they are unable to commit to a full year. However, this may result in higher premiums or less comprehensive coverage. It's important to weigh the pros and cons of different renewal options before making a decision.

Overall, the annual renewal process is a crucial part of maintaining health insurance coverage. By understanding the coverage period and the renewal process, policyholders can ensure that they have continuous protection and can make informed decisions about their health insurance needs.

HSA Contributions: Medical Insurance Expense or Not?

You may want to see also

Explore related products

![]()

Tax Implications: Health insurance premiums can be tax-deductible, reducing annual taxable income

Health insurance premiums can indeed be tax-deductible, which can significantly reduce your annual taxable income. This deduction is particularly valuable for individuals who pay for their own health insurance, rather than receiving it through an employer-sponsored plan. To qualify for this deduction, you must itemize your deductions on Schedule A of your tax return, and the total amount of your medical expenses, including health insurance premiums, must exceed a certain percentage of your adjusted gross income (AGI). As of the latest tax laws, this threshold is typically around 7.5% of your AGI, though it can vary depending on your age and other factors.

One important consideration is that you cannot deduct health insurance premiums if you are eligible for a subsidy through the Affordable Care Act (ACA) marketplace. If you receive a subsidy, it is considered advance payment of the premium tax credit, and you must reconcile this on your tax return. Additionally, if you are self-employed, you may be able to deduct health insurance premiums as a business expense, which can further reduce your taxable income. This deduction is available whether or not you itemize your personal deductions.

It's also worth noting that some states offer their own tax deductions or credits for health insurance premiums, which can provide additional savings. These state-specific benefits can vary widely, so it's important to check with your state's tax department for details. Furthermore, if you have a Health Savings Account (HSA) or a Flexible Spending Account (FSA), you may be able to use pre-tax dollars to pay for health insurance premiums, which can also reduce your taxable income.

In summary, while health insurance premiums can be a significant annual expense, the tax implications can provide substantial relief. By understanding and taking advantage of these deductions and credits, you can potentially reduce your tax burden and make health insurance more affordable. It's always a good idea to consult with a tax professional to ensure you are maximizing all available benefits.

Exploring the Myths: Is South African Health Insurance Really Free?

You may want to see also

Explore related products

![]()

Policy Changes: Insurers may update policy terms, coverage, and costs at the end of each policy year

Insurers have the discretion to update policy terms, coverage, and costs at the end of each policy year, which can significantly impact policyholders. These changes may be driven by various factors, including shifts in healthcare costs, regulatory requirements, or the insurer's business strategy. Policyholders should be aware that their coverage may not remain static and should review their policies annually to ensure they still meet their needs.

One of the key reasons insurers update policy terms is to reflect changes in healthcare costs. As medical expenses continue to rise, insurers may need to adjust premiums or coverage limits to maintain profitability. Additionally, regulatory changes can force insurers to modify their policies to comply with new laws or guidelines. For example, changes in the Affordable Care Act (ACA) may require insurers to cover additional services or alter their underwriting practices.

Policyholders should pay close attention to any notifications from their insurers regarding policy changes. These notifications typically include a summary of the changes, the effective date, and any actions the policyholder needs to take. It's essential to review these documents carefully, as they may contain important information about how the changes will affect coverage and costs.

To mitigate the impact of policy changes, policyholders can take several steps. First, they should shop around for alternative policies if they are dissatisfied with the changes. Comparing quotes from different insurers can help identify more affordable or comprehensive options. Second, policyholders can consider adjusting their coverage levels or deductibles to better align with their healthcare needs and budget. Finally, maintaining a good understanding of their policy terms and conditions can help policyholders make informed decisions about their healthcare coverage.

In conclusion, policy changes are a common occurrence in the health insurance industry, and policyholders must be proactive in reviewing and understanding these changes. By staying informed and taking appropriate actions, policyholders can ensure they have the coverage they need at a price they can afford.

Evaluating Cigna: Is It the Right Health Insurance Choice for You?

You may want to see also

Frequently asked questions

Yes, health insurance is typically an annual expense. Most health insurance plans require policyholders to pay premiums on a yearly basis, although some plans may offer monthly or quarterly payment options.

While many health insurance plans are structured as annual expenses, some insurers do offer monthly or quarterly payment plans. It's important to check with your insurance provider to see if such options are available.

Some health insurance plans, particularly those offered through employers or government programs, may provide coverage for multiple years. However, these plans often require annual renewals and may involve changes in premiums or coverage levels.

Estimating annual health insurance costs involves considering several factors, including premiums, deductibles, copays, and coinsurance. You can use online calculators or consult with an insurance agent to get a better understanding of your potential costs based on your specific needs and circumstances.