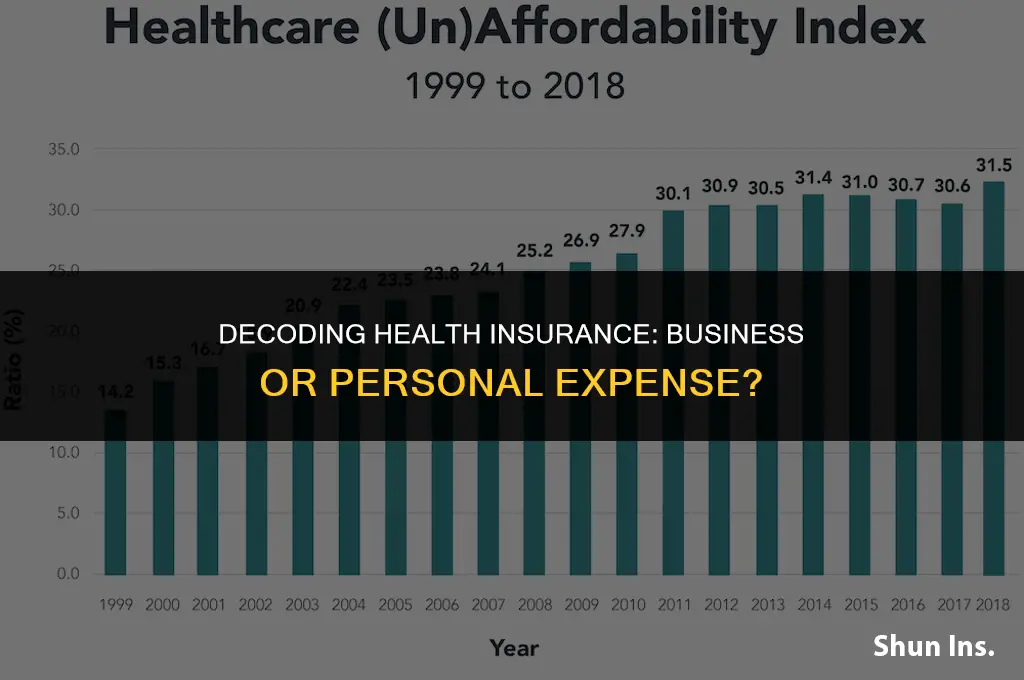

Health insurance is a critical aspect of financial planning that often raises questions about its classification as a business or personal expense. This distinction is important for tax purposes, budgeting, and understanding one's financial responsibilities. In general, health insurance can be considered both a business and a personal expense, depending on the context and the type of insurance policy in question. For individuals who are self-employed or own a business, health insurance premiums may be deductible as a business expense, reducing their taxable income. However, for employees who receive health insurance as part of their employment benefits, it is typically considered a personal expense, as the premiums are often paid with after-tax dollars. Understanding these nuances is essential for making informed decisions about health insurance and managing one's finances effectively.

| Characteristics | Values |

|---|---|

| Classification | Health insurance can be classified as both a business and personal expense, depending on the context. |

| Business Expense | For employers, health insurance premiums paid for employees are considered a business expense. This is because it's a cost incurred in the process of running a business. |

| Personal Expense | For individuals, health insurance premiums are typically considered a personal expense. This is because it's a cost incurred for personal health coverage. |

| Tax Implications | In many jurisdictions, health insurance premiums paid by employers are tax-deductible as a business expense. For individuals, health insurance premiums may be tax-deductible as a medical expense, subject to certain conditions and limits. |

| Accounting Treatment | In business accounting, health insurance premiums paid for employees are recorded as an expense on the income statement. For personal accounting, health insurance premiums are typically recorded as a personal expense. |

| Financial Planning | Health insurance is an important consideration in both business and personal financial planning. Employers need to budget for health insurance premiums as part of their employee benefits package, while individuals need to consider health insurance costs in their personal budget. |

| Regulatory Compliance | Health insurance is subject to various regulations, which can differ depending on whether it's considered a business or personal expense. Employers must comply with regulations related to employee benefits, while individuals must comply with regulations related to personal health insurance. |

| Impact on Cash Flow | Health insurance premiums can have a significant impact on cash flow, both for businesses and individuals. Employers need to ensure they have sufficient cash flow to cover health insurance premiums, while individuals need to budget for health insurance costs as part of their personal financial management. |

| Risk Management | Health insurance is a key component of risk management, both for businesses and individuals. Employers use health insurance to mitigate the risk of employee health-related costs, while individuals use health insurance to protect themselves against unexpected medical expenses. |

| Economic Impact | The cost of health insurance can have a significant economic impact, both on businesses and individuals. High health insurance premiums can increase the cost of doing business and reduce disposable income for individuals. |

Explore related products

What You'll Learn

- Tax Implications: Health insurance premiums can be tax-deductible for businesses, but not for individuals

- Coverage Types: Business health insurance often covers more people and provides broader coverage than personal plans

- Cost Sharing: Employers may share the cost of premiums with employees, reducing individual financial burden

- Regulatory Differences: Business health insurance is subject to different regulations and requirements than personal insurance

- Portability: Personal health insurance is generally more portable, allowing individuals to maintain coverage when changing jobs

![]()

Tax Implications: Health insurance premiums can be tax-deductible for businesses, but not for individuals

Businesses can deduct health insurance premiums as a business expense, reducing their taxable income. This deduction is available for premiums paid for employees, as well as for the business owner and their family if they are covered under a business plan. To qualify for this deduction, the health insurance plan must be established under the business and the premiums must be paid by the business. This can provide significant tax savings for businesses, especially those with a large number of employees.

Individuals, on the other hand, cannot deduct health insurance premiums as a business expense. However, they may be able to deduct these premiums as a medical expense on their personal tax return. To qualify for this deduction, the premiums must be paid out-of-pocket and not reimbursed by an employer or other third party. Additionally, the total medical expenses, including premiums, must exceed a certain percentage of the individual's adjusted gross income.

The distinction between business and personal health insurance expenses can have significant tax implications. For example, if an individual is self-employed and pays for their own health insurance, they may be able to deduct these premiums as a business expense on their tax return. However, if they are an employee and their employer pays for their health insurance, they cannot deduct these premiums as a business expense.

It's important to note that the tax laws surrounding health insurance premiums can be complex and may vary depending on the specific circumstances. Businesses and individuals should consult with a tax professional to determine the best way to structure their health insurance plans to maximize tax savings.

Reporting Health Insurance for Your Partner: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

Coverage Types: Business health insurance often covers more people and provides broader coverage than personal plans

Business health insurance plans are designed to cover multiple employees, offering a more comprehensive range of benefits compared to individual plans. This broader coverage often includes additional services such as dental, vision, and mental health care, which may not be available or may be limited in personal health insurance plans. Moreover, business plans typically provide higher maximum coverage limits, ensuring that employees are better protected against significant medical expenses.

One of the key advantages of business health insurance is the ability to cover dependents of employees, which is usually not an option with personal plans. This can be a significant benefit for employees with families, as it allows them to secure health coverage for their spouses and children under a single plan. Additionally, business plans often offer more flexible options for employees to customize their coverage based on their specific needs, such as choosing between different levels of deductibles and copayments.

From an employer's perspective, offering business health insurance can be a valuable tool for attracting and retaining top talent. Employees often view health insurance as a critical benefit, and companies that provide comprehensive coverage may be seen as more competitive in the job market. Furthermore, business health insurance plans can help employers manage healthcare costs more effectively, as they can negotiate better rates with insurance providers based on the size of their workforce.

However, it is important to note that business health insurance plans also come with certain limitations. For instance, they may require a minimum number of employees to qualify, and the cost of premiums can be higher compared to personal plans. Additionally, employees may have less control over their choice of healthcare providers, as business plans often have narrower networks of in-network doctors and hospitals.

In conclusion, business health insurance offers broader coverage and more comprehensive benefits than personal plans, making it an attractive option for both employers and employees. While there are some limitations to consider, the advantages of business health insurance, such as dependent coverage and cost management, can outweigh these drawbacks for many organizations and their workforce.

Insurance Companies Covering Remicade Infusions: What You Need to Know

You may want to see also

Explore related products

![]()

Cost Sharing: Employers may share the cost of premiums with employees, reducing individual financial burden

Employers sharing the cost of health insurance premiums with employees is a common practice that can significantly reduce the individual financial burden on employees. This cost-sharing model is often seen as a mutually beneficial arrangement, where both parties contribute to the overall expense of maintaining health coverage. By splitting the premiums, employers can attract and retain top talent while ensuring that their workforce has access to necessary medical care. For employees, this arrangement can make health insurance more affordable and accessible, especially for those who might otherwise struggle to pay for coverage on their own.

One unique angle to consider is the impact of cost sharing on employee morale and productivity. When employees feel that their employer is invested in their well-being, they are more likely to feel valued and motivated. This can lead to increased job satisfaction, reduced turnover rates, and ultimately, improved productivity. Furthermore, cost sharing can also encourage employees to take a more active role in their health management, as they have a financial stake in maintaining their coverage.

Another important aspect to explore is the potential tax implications of cost sharing. In many jurisdictions, employer contributions to health insurance premiums are considered tax-deductible business expenses. This can provide significant savings for employers, especially when compared to the cost of providing other forms of compensation. Additionally, employees may also be able to deduct their portion of the premiums, depending on the specific tax laws in their region.

When implementing a cost-sharing model, it is crucial for employers to carefully consider the specific needs and circumstances of their workforce. This may involve conducting surveys or focus groups to gather feedback from employees, as well as analyzing the company's financial situation and long-term goals. Employers should also be aware of any legal or regulatory requirements that may apply to their industry or location, such as minimum contribution levels or eligibility criteria.

In conclusion, cost sharing can be a valuable tool for both employers and employees, offering a range of benefits that extend beyond mere financial savings. By working together to manage the cost of health insurance, companies can foster a more positive and productive work environment, while employees can enjoy greater peace of mind and security.

Understanding Penalties for Being Uninsured: Health Insurance Fine Explained

You may want to see also

Explore related products

![]()

Regulatory Differences: Business health insurance is subject to different regulations and requirements than personal insurance

Business health insurance operates under a distinct regulatory framework compared to personal insurance. This is primarily due to the different nature of the risks involved and the scale at which these insurances are provided. For instance, the Affordable Care Act (ACA) in the United States has specific provisions for employer-sponsored health insurance, which include requirements for minimum essential coverage and the prohibition of pre-existing condition exclusions. These regulations aim to ensure that employees have access to affordable and comprehensive health care.

One of the key regulatory differences is the tax treatment of premiums. For businesses, health insurance premiums are generally tax-deductible as a business expense, which can significantly reduce the overall cost of providing health benefits to employees. In contrast, individuals who purchase personal health insurance may only be able to deduct premiums if they itemize their deductions and meet certain income thresholds. This disparity in tax treatment underscores the importance of understanding the regulatory environment when considering whether health insurance is a business or personal expense.

Another regulatory distinction lies in the oversight and compliance requirements. Business health insurance plans are subject to the Employee Retirement Income Security Act (ERISA), which sets federal standards for employee benefit plans. This includes requirements for plan administration, reporting, and disclosure. Personal health insurance, on the other hand, is primarily regulated by state laws, which can vary significantly from one state to another. This means that businesses must navigate a complex web of federal and state regulations when designing and implementing health insurance plans for their employees.

Furthermore, the regulatory landscape for business health insurance is constantly evolving. Recent changes, such as the introduction of the ACA's employer mandate, have imposed new requirements on businesses to provide health coverage to their employees or face penalties. This has led to a shift in how businesses approach health insurance, with many opting to self-insure or explore alternative funding arrangements to mitigate costs. In contrast, personal health insurance has seen less dramatic regulatory changes in recent years, although individuals must still contend with the complexities of the ACA's individual mandate and the ongoing debate over health care reform.

In conclusion, the regulatory differences between business and personal health insurance are significant and multifaceted. Understanding these differences is crucial for businesses and individuals alike, as they can have a profound impact on the cost, accessibility, and quality of health care. By navigating the complex regulatory environment, businesses can design health insurance plans that meet their unique needs while also complying with federal and state laws.

Exploring the Legality of Dual Health Insurance in California

You may want to see also

Explore related products

![]()

Portability: Personal health insurance is generally more portable, allowing individuals to maintain coverage when changing jobs

Personal health insurance offers a significant advantage in terms of portability, which is a critical factor for many individuals in today's dynamic job market. This portability allows policyholders to maintain their health coverage seamlessly when transitioning between employers, ensuring continuous protection against unforeseen medical expenses. In contrast, employer-sponsored health insurance often requires individuals to start from scratch with a new plan each time they change jobs, which can lead to gaps in coverage and increased administrative hassle.

The portability of personal health insurance is particularly beneficial for professionals who frequently switch jobs or work in industries with high turnover rates. It provides a sense of security and stability, knowing that their health insurance will remain in place regardless of their employment status. Furthermore, personal health insurance plans are often more customizable, allowing individuals to tailor their coverage to their specific needs and preferences, which can be especially important for those with pre-existing conditions or unique health requirements.

Another unique aspect of personal health insurance is that it can be more cost-effective in the long run, especially for individuals who are healthy and do not require extensive medical care. By maintaining a consistent plan, policyholders can avoid the penalties and rate increases that often accompany new employer-sponsored plans. Additionally, personal health insurance can offer more comprehensive coverage options, including dental, vision, and mental health care, which may not be available through employer-sponsored plans.

However, it is important to note that personal health insurance also comes with its own set of challenges. Policyholders are responsible for paying the full premium, which can be a significant financial burden, especially for those with lower incomes. Additionally, personal health insurance plans may have higher deductibles and out-of-pocket costs compared to employer-sponsored plans, which can make them less attractive for individuals who anticipate frequent medical expenses.

In conclusion, the portability of personal health insurance is a valuable feature that can provide individuals with peace of mind and financial security in an ever-changing job market. While there are certainly trade-offs to consider, such as cost and coverage options, the ability to maintain consistent health insurance coverage can be a significant advantage for many people. As such, it is essential for individuals to carefully weigh the pros and cons of personal health insurance when making decisions about their healthcare coverage.

Understanding the One-Month Waiting Period in Health Insurance Policies

You may want to see also

Frequently asked questions

Health insurance can be considered both a business expense and a personal expense, depending on the context. For individuals, health insurance is typically a personal expense. However, for businesses that provide health insurance to their employees, it is considered a business expense.

Yes, businesses can generally deduct health insurance premiums paid for employees as a business expense on their tax return. This deduction helps reduce the overall taxable income of the business.

The Affordable Care Act (ACA) has specific provisions that affect how health insurance expenses are classified. For example, the ACA requires businesses with a certain number of employees to provide health insurance, which would classify the premiums as a business expense. Additionally, the ACA provides subsidies to individuals who purchase health insurance through the marketplace, which can impact the personal expense classification.

Yes, there are differences in tax treatment for health insurance expenses between sole proprietors and incorporated businesses. Sole proprietors can deduct health insurance premiums for themselves and their employees as a business expense. However, incorporated businesses can only deduct health insurance premiums paid for employees, not for the business owners themselves.