Health insurance costs can vary significantly depending on where you live, and California is no exception. Residents of the Golden State may wonder if they can find more affordable health insurance options outside of California. The answer to this question is not straightforward, as it depends on various factors such as age, income, health status, and the type of coverage desired. While some neighboring states may offer lower premiums, others may have higher costs or different coverage requirements. Additionally, California has its own unique health insurance marketplace and Medicaid expansion, which can impact the affordability of coverage for its residents. To determine if health insurance is less expensive outside of California, it's essential to compare quotes and coverage options across state lines while considering all relevant factors.

Explore related products

$15.67 $30

What You'll Learn

- State-by-State Comparison: Analyze health insurance costs across different states to identify more affordable options

- Factors Influencing Costs: Explore reasons why health insurance might be cheaper in some states, such as lower healthcare costs or different regulations

- Types of Insurance Plans: Compare the costs of various insurance plans (e.g., HMO, PPO) available in different states

- Eligibility and Subsidies: Investigate how eligibility for subsidies and tax credits varies by state, impacting overall costs

- Moving Out of State: Consider the implications of relocating to a state with lower health insurance premiums, including potential changes in coverage and quality of care

![]()

State-by-State Comparison: Analyze health insurance costs across different states to identify more affordable options

Analyzing health insurance costs across different states reveals significant variations that can impact the affordability of coverage. For instance, states like California often have higher premiums due to a combination of factors such as the cost of living, state regulations, and the overall health of the population. In contrast, states like Wyoming or West Virginia may offer lower premiums due to lower costs of living and different regulatory environments.

To conduct a thorough state-by-state comparison, one should consider several key factors:

- Premium Costs: This is the most obvious factor but also the most critical. Compare the average monthly premiums for similar plans across different states.

- Deductibles and Co-pays: Lower premiums might come with higher deductibles or co-pays, which can affect the overall affordability of care.

- State Regulations: Some states have more stringent regulations on insurance providers, which can drive up costs. Others may have more relaxed regulations, potentially leading to lower premiums.

- Healthcare Costs: The cost of healthcare services in a state directly impacts insurance premiums. States with higher healthcare costs will generally have higher insurance premiums.

- Subsidies and Assistance Programs: Some states offer additional subsidies or assistance programs that can help reduce the cost of insurance for low-income individuals or families.

Using online tools or working with an insurance broker can facilitate this comparison process. These resources can provide detailed breakdowns of costs and help identify more affordable options based on individual needs and circumstances.

Ultimately, while it may be tempting to seek out states with lower premiums, it's essential to consider the broader implications. Factors such as the quality of healthcare providers, the availability of specialized care, and the overall health of the population should also be taken into account when making a decision about health insurance.

Understanding Non-Marketplace Health Insurance: Benefits, Options, and How It Works

You may want to see also

Explore related products

$19.86 $21.99

![]()

Factors Influencing Costs: Explore reasons why health insurance might be cheaper in some states, such as lower healthcare costs or different regulations

Several factors contribute to the variation in health insurance costs across different states. One primary reason is the difference in healthcare costs themselves. States with lower costs of living often have lower healthcare costs, which in turn can lead to cheaper health insurance premiums. For instance, states in the Midwest and South generally have lower healthcare costs compared to states on the East and West coasts.

Another significant factor is the regulatory environment. States have different regulations regarding health insurance, which can impact the cost of premiums. Some states have more stringent regulations that require insurance companies to cover more services or have higher standards for coverage, which can increase costs. Conversely, states with more relaxed regulations may have lower premiums.

The competitive landscape of insurance providers within a state also plays a role. States with more insurance companies competing for business may have lower premiums as companies try to attract customers with better rates. On the other hand, states with fewer providers may have higher premiums due to less competition.

Additionally, the health of the population in a state can influence insurance costs. States with healthier populations may have lower premiums because there is less demand for healthcare services. Conversely, states with higher rates of chronic diseases or other health issues may have higher premiums to account for the increased demand for healthcare.

Lastly, state-specific programs and initiatives can also impact health insurance costs. Some states have programs that help subsidize health insurance for low-income residents or provide additional benefits, which can increase costs. However, these programs can also help make health insurance more affordable for certain segments of the population.

In conclusion, the cost of health insurance can vary significantly from state to state due to a combination of factors including healthcare costs, regulations, competition, population health, and state-specific programs. Understanding these factors can help individuals make informed decisions about their health insurance options.

Sam's Club Enters the Medical Insurance Arena

You may want to see also

Explore related products

$14.01 $20.95

$14.51 $19.95

![]()

Types of Insurance Plans: Compare the costs of various insurance plans (e.g., HMO, PPO) available in different states

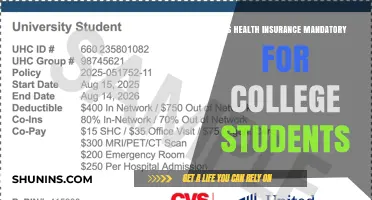

Health insurance costs can vary significantly depending on the type of plan you choose. Two common types of plans are Health Maintenance Organizations (HMOs) and Preferred Provider Organizations (PPOs). HMOs typically have lower premiums but higher out-of-pocket costs, while PPOs have higher premiums but lower out-of-pocket costs. When comparing the costs of these plans across different states, it's important to consider factors such as the cost of living, healthcare provider fees, and state regulations.

For example, in California, the average monthly premium for an HMO plan is around $400, while in Texas, it's closer to $300. However, the out-of-pocket costs for an HMO plan in Texas may be higher than in California due to differences in healthcare provider fees. On the other hand, PPO plans in California may have higher premiums than in Texas, but the out-of-pocket costs may be lower.

When choosing a health insurance plan, it's important to consider your individual needs and budget. If you have a chronic condition or require frequent medical care, a PPO plan may be a better option for you, even if it has a higher premium. However, if you are generally healthy and don't require much medical care, an HMO plan may be a more cost-effective option.

It's also important to consider the network of healthcare providers available through each plan. HMOs typically have a more limited network of providers, while PPOs offer more flexibility in choosing providers. If you have a preferred healthcare provider, make sure they are included in the plan's network before enrolling.

In conclusion, when comparing the costs of different health insurance plans across states, it's important to consider factors such as premiums, out-of-pocket costs, cost of living, healthcare provider fees, and state regulations. By carefully evaluating these factors, you can choose a plan that meets your individual needs and budget.

Does Health Insurance Cover Pap Smears? What You Need to Know

You may want to see also

![]()

Eligibility and Subsidies: Investigate how eligibility for subsidies and tax credits varies by state, impacting overall costs

Eligibility for subsidies and tax credits is a critical factor in determining the affordability of health insurance, and this varies significantly from state to state. For instance, some states have expanded Medicaid under the Affordable Care Act (ACA), providing low-cost coverage to a larger portion of the population, while others have not. This expansion can drastically reduce the cost of health insurance for eligible individuals.

Subsidies for private insurance plans also differ by state. The ACA provides federal subsidies to help reduce premiums and out-of-pocket costs for those purchasing plans through the health insurance marketplace. However, the amount and availability of these subsidies can vary based on state-specific rules and the income levels of the insured. Some states offer additional subsidies or have implemented their own reinsurance programs to stabilize the market and reduce costs.

Tax credits are another important aspect to consider. States may offer tax credits to individuals or businesses that purchase health insurance, further reducing the overall cost. These credits can be particularly beneficial for small business owners or self-employed individuals who may not have access to employer-sponsored plans.

Navigating these varying eligibility requirements and subsidy options can be complex. It's essential for individuals to understand their state's specific rules and programs to maximize their savings and ensure they are getting the most affordable coverage possible. Consulting with a healthcare professional or using online resources can help in making informed decisions.

In conclusion, the impact of eligibility for subsidies and tax credits on health insurance costs cannot be overstated. By investigating and understanding these variations, individuals can potentially save a significant amount of money on their health insurance premiums and out-of-pocket expenses.

Medical Insurance: Opting Out and the Risks Involved

You may want to see also

![]()

Moving Out of State: Consider the implications of relocating to a state with lower health insurance premiums, including potential changes in coverage and quality of care

Relocating to a state with lower health insurance premiums can be an attractive option for many, especially those looking to reduce their monthly expenses. However, it's crucial to consider the potential implications on your health coverage and quality of care. While lower premiums may seem like a financial boon, they could also indicate differences in the healthcare services provided or the insurance policies' comprehensiveness.

One of the primary considerations when moving to a state with lower health insurance costs is the possibility of changes in coverage. Insurance policies can vary significantly from state to state, with some offering more extensive coverage than others. It's essential to review the specific details of the policies available in the new state to ensure they meet your healthcare needs. This includes examining the types of services covered, the presence of any pre-existing condition exclusions, and the overall scope of the insurance plan.

Another factor to consider is the quality of healthcare providers in the new state. Lower insurance premiums might be a result of reduced reimbursement rates for healthcare services, which could impact the quality of care received. Researching the healthcare system in the new state, including the availability of specialists, hospitals, and other medical facilities, can provide valuable insights into the potential quality of care.

Additionally, it's important to consider the long-term financial implications of moving to a state with lower health insurance premiums. While the immediate cost savings may be appealing, it's necessary to evaluate how these savings might be offset by other factors, such as changes in income, cost of living, or future healthcare needs. A thorough financial analysis can help determine whether the move is truly beneficial in the long run.

In conclusion, while moving to a state with lower health insurance premiums can offer financial advantages, it's essential to carefully consider the potential impact on your health coverage and quality of care. By conducting thorough research and analysis, you can make an informed decision that best aligns with your healthcare needs and financial goals.

When Does Health Insurance Coverage End for Young Adults?

You may want to see also

Frequently asked questions

Health insurance costs can vary significantly by state due to differences in healthcare costs, state regulations, and the health risk profiles of populations. While California tends to have higher healthcare costs, which can lead to more expensive insurance premiums, it's not universally true that health insurance is less expensive outside of California. Costs can be lower in some states but higher in others.

Several factors influence the cost of health insurance across different states, including:

- Healthcare costs: The cost of medical services and procedures varies by state.

- State regulations: Insurance regulations, including the types of plans allowed and coverage requirements, differ from state to state.

- Health risk profiles: States with populations that have higher health risks may have higher insurance premiums.

- Competition: The number of insurance providers in a state can affect prices; more competition often leads to lower costs.

- Subsidies: States may offer different levels of subsidies for health insurance, impacting the final cost to consumers.

To compare health insurance costs between California and other states, one can:

- Use online insurance comparison tools that allow you to input your information and receive quotes from multiple providers.

- Consult with a licensed insurance agent who can provide personalized advice and comparisons.

- Review data from state insurance departments or healthcare exchanges, which often publish information on average premium costs.

- Consider factors such as deductible amounts, co-pays, and coverage limits in addition to premium costs to get a comprehensive understanding of the total cost of insurance.