Health Savings Accounts (HSAs) are a popular way for individuals to save money for medical expenses while also reducing their taxable income. However, there is often confusion about whether the money in an HSA is taxable. The short answer is that, generally, withdrawals from an HSA for qualified medical expenses are tax-free. But, if you withdraw funds for non-qualified expenses, you may be subject to taxes and potentially a penalty. It's important to understand the rules surrounding HSA withdrawals to ensure you're making the most of this tax-advantaged savings tool while avoiding any unexpected tax liabilities.

Explore related products

What You'll Learn

- HSA Basics: Understand what a Health Savings Account (HSA) is and how it works

- Tax-Free Contributions: Learn about the tax advantages of contributing to an HSA

- Qualified Expenses: Discover what types of health expenses are eligible for tax-free withdrawals

- Investment Options: Explore how you can invest the funds in your HSA to grow your savings

- Withdrawal Rules: Understand the rules and potential penalties for withdrawing funds from your HSA

![]()

HSA Basics: Understand what a Health Savings Account (HSA) is and how it works

A Health Savings Account (HSA) is a tax-advantaged account available to individuals who have a high-deductible health plan (HDHP) and are not enrolled in Medicare. HSAs are designed to help individuals save money on healthcare costs by allowing them to set aside pre-tax dollars for qualified medical expenses. Contributions to an HSA are tax-deductible, and the funds can be used tax-free for eligible healthcare costs, such as deductibles, copayments, and prescriptions.

One of the key benefits of an HSA is its flexibility. Unlike other types of health accounts, such as Flexible Spending Accounts (FSAs) or Health Reimbursement Accounts (HRAs), HSAs are not tied to a specific employer or health plan. This means that individuals can keep their HSA even if they change jobs or health insurance providers. Additionally, HSAs have no "use it or lose it" rule, which allows individuals to carry over unused funds from year to year.

To be eligible for an HSA, individuals must meet certain criteria. They must have a high-deductible health plan with a minimum deductible amount, and they cannot be enrolled in Medicare. Additionally, individuals cannot be claimed as a dependent on someone else's tax return. Once an individual opens an HSA, they can contribute to the account throughout the year, up to the annual contribution limit.

When it comes to using HSA funds, it's important to understand what qualifies as an eligible expense. Generally, HSA funds can be used for any qualified medical expense, including deductibles, copayments, prescriptions, and other healthcare costs. However, there are some exceptions. For example, HSA funds cannot be used for cosmetic procedures, except in certain circumstances where the procedure is deemed medically necessary.

One of the most common questions about HSAs is whether the funds are taxable. The good news is that HSA funds are generally not taxable when used for qualified medical expenses. However, if HSA funds are used for non-qualified expenses, they may be subject to income tax and a 20% penalty. It's important to keep track of HSA expenses and ensure that they are all eligible to avoid any potential tax implications.

In conclusion, HSAs can be a valuable tool for individuals looking to save money on healthcare costs. By understanding the basics of how HSAs work, including eligibility criteria, contribution limits, and qualified expenses, individuals can make the most of this tax-advantaged account and potentially reduce their overall healthcare expenses.

Navigating Medical Insurance Coverage for LASIK Surgery

You may want to see also

Explore related products

![]()

Tax-Free Contributions: Learn about the tax advantages of contributing to an HSA

Contributing to a Health Savings Account (HSA) offers significant tax advantages that can enhance your financial well-being. One of the primary benefits is the ability to make tax-free contributions. This means that the money you deposit into your HSA is not subject to federal income tax, reducing your taxable income for the year.

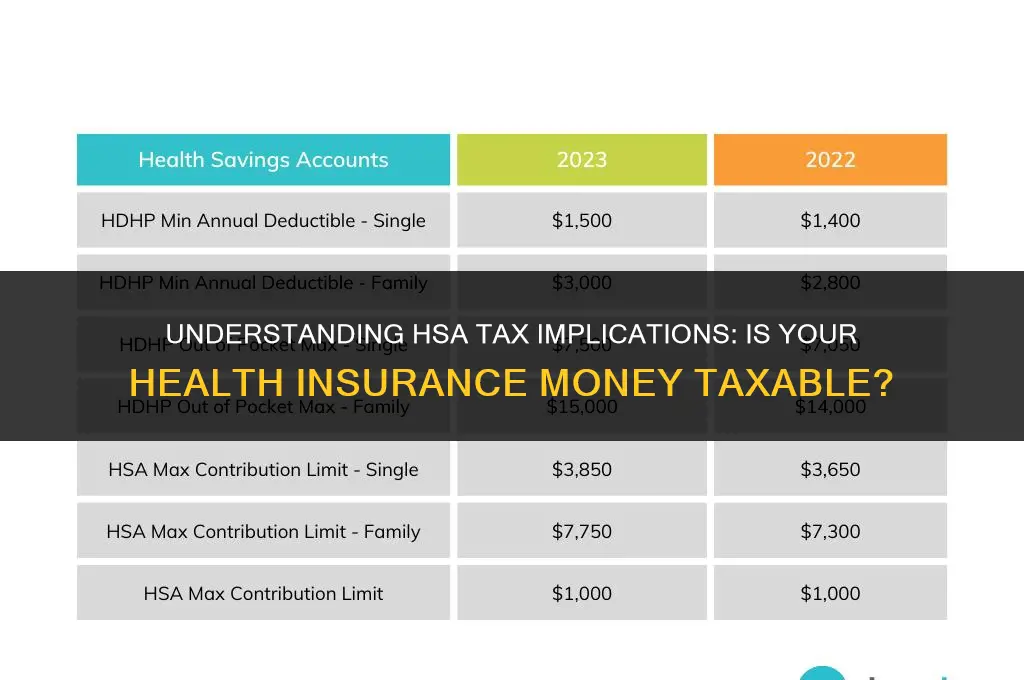

To maximize these tax benefits, it's essential to understand the contribution limits. For 2023, individuals can contribute up to $3,850, while families can contribute up to $7,750. These limits are subject to change, so it's crucial to stay informed about any adjustments made by the IRS.

Another advantage of HSAs is the ability to carry over unused funds from one year to the next. Unlike Flexible Spending Accounts (FSAs), which have a "use it or lose it" policy, HSAs allow you to build up a balance over time. This feature can be particularly beneficial for individuals who have lower healthcare expenses in some years and higher expenses in others.

When it comes to withdrawals, HSAs offer flexibility. You can withdraw funds tax-free at any time for qualified medical expenses. This includes a wide range of healthcare costs, such as doctor visits, prescription medications, and even certain over-the-counter items. However, it's important to note that non-qualified withdrawals may be subject to taxes and penalties.

In addition to the tax benefits, HSAs can also serve as a valuable tool for retirement savings. If you're able to contribute the maximum amount each year and invest your funds wisely, you can accumulate a substantial balance over time. This can provide a tax-advantaged source of income to cover healthcare expenses in retirement.

Overall, understanding the tax advantages of contributing to an HSA can help you make informed decisions about your healthcare and financial planning. By taking advantage of these benefits, you can potentially reduce your tax burden, build a nest egg for future healthcare expenses, and enjoy greater financial security.

Adding a Dependent to Health Insurance: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

Qualified Expenses: Discover what types of health expenses are eligible for tax-free withdrawals

To determine if health insurance money in your Health Savings Account (HSA) is taxable, it's crucial to understand the concept of qualified expenses. Qualified expenses are health-related costs that are eligible for tax-free withdrawals from your HSA. These expenses can include medical services, prescription medications, and other health care costs that are not covered by your health insurance plan.

One of the key benefits of an HSA is the ability to withdraw funds tax-free for qualified medical expenses. This means that if you use your HSA funds to pay for eligible health care costs, you won't have to pay taxes on the withdrawals. However, it's important to note that not all health-related expenses qualify for tax-free withdrawals. For example, health insurance premiums are generally not considered qualified expenses, unless you are self-employed or have a high-deductible health plan (HDHP).

To ensure that you are using your HSA funds for qualified expenses, it's a good idea to keep track of your medical expenses and receipts. This will help you to accurately report your qualified expenses on your tax return and avoid any potential penalties or taxes on non-qualified withdrawals. Additionally, it's important to be aware of any changes to the tax laws or regulations that may affect the types of expenses that are eligible for tax-free withdrawals from your HSA.

In summary, understanding qualified expenses is essential for maximizing the tax benefits of your HSA. By using your HSA funds for eligible health care costs, you can avoid paying taxes on your withdrawals and make the most of this valuable savings tool.

Does Massage Envy Offer Health Insurance? Benefits Explained

You may want to see also

Explore related products

![]()

Investment Options: Explore how you can invest the funds in your HSA to grow your savings

One of the key benefits of a Health Savings Account (HSA) is the ability to invest the funds you've saved, allowing your money to grow over time. This investment feature sets HSAs apart from other types of health savings accounts, like Flexible Spending Accounts (FSAs) or Health Reimbursement Accounts (HRAs), which typically do not offer investment options. By investing your HSA funds wisely, you can potentially increase your savings significantly, which can be particularly beneficial for covering future medical expenses or even supplementing your retirement income.

When considering investment options for your HSA, it's important to understand the different types of investments available and their associated risks and rewards. Common investment choices include stocks, bonds, mutual funds, and exchange-traded funds (ETFs). Stocks offer the potential for high returns but come with higher risk, while bonds are generally considered safer but offer lower returns. Mutual funds and ETFs provide a way to diversify your investments across multiple stocks or bonds, reducing risk while still offering the potential for growth.

Before investing your HSA funds, it's crucial to assess your risk tolerance and investment goals. Are you looking for aggressive growth, or do you prefer a more conservative approach? Consider factors such as your age, financial situation, and the time horizon for when you'll need to use the funds. If you're unsure about how to proceed, consulting with a financial advisor can be a wise decision. They can help you create a personalized investment strategy that aligns with your goals and risk tolerance.

Another important aspect to consider is the fees associated with investing your HSA funds. Some HSA providers may charge additional fees for investment accounts, which can eat into your returns over time. Be sure to compare fees among different providers and choose one that offers low-cost investment options. Additionally, keep in mind that while investing can grow your HSA funds, it's also possible to lose money if your investments don't perform well. Therefore, it's essential to monitor your investments regularly and make adjustments as needed.

In conclusion, investing your HSA funds can be a smart way to grow your savings and prepare for future medical expenses or retirement. By understanding the different investment options, assessing your risk tolerance, and being mindful of fees, you can make informed decisions that help you achieve your financial goals. Remember, the key to successful investing is patience and a long-term perspective.

Building a Health Insurance Exchange: A Comprehensive Step-by-Step Guide

You may want to see also

Explore related products

![]()

Withdrawal Rules: Understand the rules and potential penalties for withdrawing funds from your HSA

Withdrawing funds from your Health Savings Account (HSA) involves specific rules and potential penalties that you must understand to avoid unnecessary taxes and fees. Generally, HSA funds can be withdrawn tax-free if used for qualified medical expenses, but there are important stipulations to consider.

First, it's crucial to note that HSA withdrawals for non-qualified expenses will be subject to income tax and a 20% penalty. This penalty is particularly steep and underscores the importance of using HSA funds solely for their intended purpose. However, there are some exceptions to this penalty, such as using the funds for health insurance premiums while you're unemployed or for long-term care expenses.

To avoid penalties, you should keep detailed records of all medical expenses and ensure that you're only withdrawing the exact amount needed. It's also advisable to consult with a tax professional or financial advisor to ensure that your withdrawals comply with IRS regulations.

Another key aspect of HSA withdrawal rules is the age requirement. If you withdraw funds before age 65 for non-qualified expenses, you'll face the 20% penalty in addition to income tax. However, once you reach age 65, you can withdraw funds for any reason without penalty, although you'll still need to pay income tax on non-qualified withdrawals.

In summary, understanding the rules and potential penalties for withdrawing funds from your HSA is essential for maximizing the tax advantages and avoiding unnecessary financial burdens. By using your HSA funds wisely and staying informed about the regulations, you can make the most of this valuable financial tool.

Understanding Health Insurance Costs: A Monthly Bill Breakdown

You may want to see also

Frequently asked questions

No, the money you contribute to your HSA is not taxable. Contributions are made on a pre-tax basis, which means they are deducted from your gross income before taxes are calculated.

No, the interest or investment gains in your HSA are tax-free as long as they remain in the account. You only pay taxes when you withdraw the funds, and if used for qualified medical expenses, the withdrawals are also tax-free.

If you withdraw money from your HSA for non-medical expenses, the withdrawn amount is taxable as ordinary income. Additionally, you may have to pay a 20% penalty tax on the withdrawal, unless you are 65 years old or older, or if you are disabled.