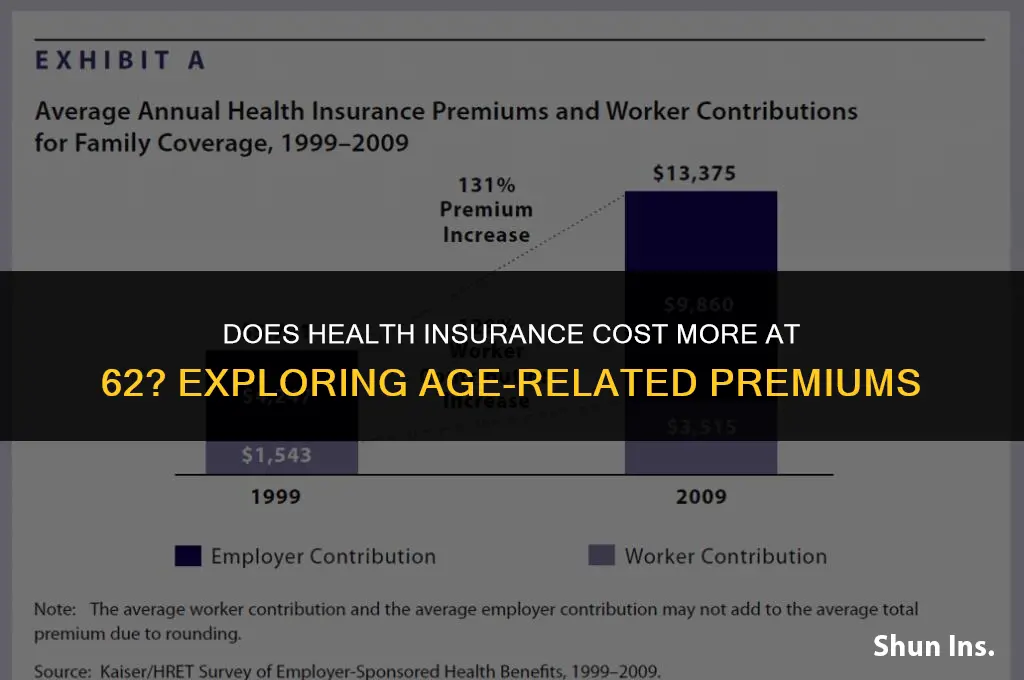

Health insurance costs can vary significantly based on several factors, including age. As individuals approach 62 years old, they may notice changes in their health insurance premiums. This is often due to the increased likelihood of health issues and the need for more comprehensive coverage as one ages. In many countries, health insurance providers adjust their rates according to age brackets, with older individuals typically facing higher premiums. Additionally, the type of health insurance plan, the individual's health history, and the region they live in can all influence the cost of coverage. Understanding these factors can help individuals make informed decisions about their health insurance options as they approach 62 years old.

Explore related products

What You'll Learn

- Age-Related Premiums: Health insurance costs often rise with age due to increased health risks

- Medicare Eligibility: At 62, individuals may be nearing Medicare eligibility, affecting insurance options and costs

- Pre-Existing Conditions: Older adults may have more pre-existing conditions, potentially increasing insurance premiums

- Marketplace Plans: Premiums for marketplace plans can vary significantly based on age and location

- Employer Coverage: Retirees may lose employer-sponsored insurance, leading to higher costs for individual plans

![]()

Age-Related Premiums: Health insurance costs often rise with age due to increased health risks

As individuals approach the age of 62, they often encounter a significant increase in their health insurance premiums. This rise is primarily due to the heightened health risks associated with aging. Insurance companies assess risk based on actuarial tables, which statistically predict the likelihood of health issues and the associated costs. As people age, the probability of developing chronic conditions, requiring more frequent medical attention, and incurring higher healthcare expenses generally increases. Consequently, insurers adjust premiums to reflect these elevated risks.

The impact of age on health insurance costs can be substantial. For instance, a healthy 62-year-old might pay significantly more for a policy than a younger individual with similar health status. This is because the insurer anticipates that the older policyholder will utilize more healthcare services and incur greater expenses over time. Additionally, the Affordable Care Act (ACA) allows insurers to charge older adults up to three times more than younger adults for the same coverage, further exacerbating the cost disparity.

To mitigate these rising costs, individuals nearing 62 may consider several strategies. One approach is to maintain a high level of physical fitness and health, as this can help reduce the likelihood of developing age-related health issues. Preventive healthcare measures, such as regular check-ups and screenings, can also help identify and manage potential health problems early on, potentially lowering long-term healthcare costs. Furthermore, exploring different insurance providers and plans can help individuals find more affordable coverage options that better suit their needs and budget.

Another important consideration for those approaching 62 is the potential impact of retirement on their health insurance situation. Employer-sponsored health insurance often ends upon retirement, forcing individuals to seek alternative coverage. This transition can be complex, as retirees must navigate the intricacies of Medicare, Medicaid, and private insurance options. Understanding the nuances of these programs and selecting the most appropriate coverage can help retirees manage their healthcare costs more effectively.

In conclusion, the increase in health insurance premiums at age 62 is a significant concern for many individuals. By understanding the factors contributing to these rising costs and exploring strategies to mitigate them, older adults can better navigate the complex landscape of health insurance and maintain their financial well-being.

Accessible Healthcare: Exploring Insurance Options for Low-Income Families

You may want to see also

Explore related products

![]()

Medicare Eligibility: At 62, individuals may be nearing Medicare eligibility, affecting insurance options and costs

As individuals approach the age of 62, they enter a critical phase in their healthcare journey. This age marks the beginning of Medicare eligibility, which can significantly impact their insurance options and costs. Understanding the nuances of Medicare eligibility is crucial for making informed decisions about health coverage.

Medicare, a federal health insurance program, primarily serves individuals aged 65 and older, as well as certain younger people with disabilities. However, the eligibility rules for Medicare are complex and can vary based on individual circumstances. For instance, some people may be eligible for Medicare before turning 65 if they have a disability or end-stage renal disease. Conversely, others may need to wait until they reach full retirement age to enroll in Medicare without facing penalties.

One of the key factors affecting Medicare eligibility is the individual's work history. To qualify for Medicare, a person must have paid Medicare taxes for at least 10 years. This requirement ensures that the program is funded through payroll taxes and that beneficiaries have contributed to the system over time. Additionally, the age at which an individual can enroll in Medicare without facing penalties depends on their birth year. For those born before 1938, the full retirement age is 65. However, for those born after 1937, the full retirement age increases gradually, reaching 67 for individuals born in 1960 or later.

The intersection of Medicare eligibility and health insurance costs is particularly important for individuals aged 62. At this age, many people are still working and may have employer-sponsored health insurance. However, as they approach Medicare eligibility, they may need to consider transitioning to Medicare or supplementing their employer-sponsored coverage with Medicare. This transition can be complex and may involve coordinating benefits between multiple insurance providers.

Moreover, the cost of health insurance for individuals aged 62 can vary significantly depending on their circumstances. For those who are still working and have employer-sponsored coverage, the cost of insurance may be relatively stable. However, for those who are retired or have limited income, the cost of Medicare premiums and out-of-pocket expenses can be a significant burden. Understanding the different parts of Medicare, such as Part A (hospital insurance), Part B (medical insurance), and Part D (prescription drug coverage), is essential for navigating the cost landscape.

In conclusion, Medicare eligibility at age 62 is a critical juncture that can have a profound impact on an individual's health insurance options and costs. By understanding the eligibility rules, work history requirements, and cost implications, individuals can make informed decisions about their healthcare coverage and ensure a smooth transition into the Medicare system.

Medical Insurance Costs for Married Couples: How Much?

You may want to see also

Explore related products

![]()

Pre-Existing Conditions: Older adults may have more pre-existing conditions, potentially increasing insurance premiums

As individuals age, the likelihood of developing chronic health conditions increases. These pre-existing conditions can range from manageable illnesses like hypertension and diabetes to more severe conditions such as heart disease or cancer. When it comes to health insurance, these pre-existing conditions can significantly impact the cost of premiums. Insurance companies often view older adults with multiple pre-existing conditions as higher risk, which can lead to increased premium rates.

The Affordable Care Act (ACA) has implemented measures to protect individuals with pre-existing conditions from being denied coverage or charged exorbitant rates. However, these protections do not entirely eliminate the impact of pre-existing conditions on insurance premiums. Older adults may still face higher costs due to their health status, even if they are not explicitly charged more because of their conditions.

One way that older adults can mitigate the impact of pre-existing conditions on their insurance premiums is by maintaining a healthy lifestyle and actively managing their health. This can include regular exercise, a balanced diet, and adherence to prescribed treatment plans. Additionally, older adults may benefit from working with a healthcare provider to develop a comprehensive care plan that addresses their specific health needs and helps to prevent the development of new conditions.

Another strategy for older adults is to carefully compare insurance plans and providers to find the most affordable options that meet their healthcare needs. This may involve considering factors such as deductible amounts, co-pays, and out-of-pocket maximums, as well as the specific coverage provided for their pre-existing conditions. Older adults may also want to explore options such as Medicare or Medicaid, which can provide more affordable coverage for those with limited incomes or significant health needs.

In conclusion, while pre-existing conditions can increase the cost of health insurance for older adults, there are steps that can be taken to manage these costs. By maintaining a healthy lifestyle, actively managing their health, and carefully comparing insurance options, older adults can find more affordable coverage that meets their needs.

Understanding Your Medical Insurance Coverage: What's Included?

You may want to see also

Explore related products

![]()

Marketplace Plans: Premiums for marketplace plans can vary significantly based on age and location

Premiums for marketplace plans can indeed vary significantly based on age and location. This variability is a key factor to consider when evaluating the cost of health insurance, particularly for individuals nearing or at the age of 62. As age increases, the likelihood of requiring medical attention also rises, which can lead to higher premiums. Additionally, healthcare costs can differ greatly from one state to another, influenced by factors such as the cost of living, state healthcare regulations, and the overall health of the population.

For instance, a 62-year-old individual living in a state with high healthcare costs, such as New York or California, may face substantially higher premiums compared to someone of the same age living in a state with lower healthcare costs, like Wyoming or Utah. Furthermore, the type of plan chosen can also impact the premium cost. Plans with lower deductibles and more comprehensive coverage typically come with higher premiums, while plans with higher deductibles and less coverage may have lower premiums but could result in higher out-of-pocket costs.

It's also important to note that subsidies may be available to help offset the cost of premiums for individuals who meet certain income criteria. These subsidies can significantly reduce the financial burden of health insurance for older adults. Additionally, individuals who are nearing Medicare eligibility may want to consider their options carefully, as the transition to Medicare can involve changes in coverage and costs.

In conclusion, the cost of health insurance for individuals aged 62 can vary widely depending on a number of factors, including age, location, and the type of plan chosen. By carefully evaluating these factors and considering available subsidies, older adults can make informed decisions about their health insurance coverage.

Group vs. Individual Health Insurance: Which Option Saves You More?

You may want to see also

Explore related products

![]()

Employer Coverage: Retirees may lose employer-sponsored insurance, leading to higher costs for individual plans

Retirees often face a significant shift in their health insurance landscape upon leaving the workforce. Employer-sponsored insurance, which is typically more affordable due to group rates and employer subsidies, is no longer available. This transition can lead to a substantial increase in health insurance costs for individuals who must then seek coverage through private insurers or government programs like Medicare.

The loss of employer coverage can be particularly challenging for early retirees, those retiring before the age of 65, as they may not yet be eligible for Medicare. This gap period can result in higher premiums for individual plans, as insurers often charge more for older adults who are not part of a larger, employer-sponsored group. Furthermore, individual plans may not offer the same level of coverage or network access as employer-sponsored plans, potentially leading to additional out-of-pocket expenses for retirees.

To mitigate these costs, retirees may consider several strategies. One approach is to explore COBRA (Consolidated Omnibus Budget Reconciliation Act) coverage, which allows individuals to continue their employer-sponsored health insurance for a limited time after retirement, albeit at a higher cost. Another option is to look into health savings accounts (HSAs) or flexible spending accounts (FSAs) to help cover medical expenses. Additionally, retirees may benefit from consulting with a health insurance advisor to navigate the complexities of individual plan selection and identify potential cost-saving opportunities.

In conclusion, the transition from employer-sponsored insurance to individual coverage can be a significant financial hurdle for retirees. By understanding the implications of this shift and exploring available options, retirees can better manage their health insurance costs and ensure they have adequate coverage in their post-work life.

Choosing the Right Health Insurance Provider: A Comprehensive Guide

You may want to see also

Frequently asked questions

Yes, health insurance premiums tend to increase with age, including at 62. This is because older individuals generally have higher healthcare costs due to a greater likelihood of chronic conditions and more frequent medical care.

Health insurance costs more as you get older because older adults are statistically more likely to require medical attention. This increased risk of health issues leads to higher premiums to cover the anticipated costs.

Yes, seniors can explore several options to reduce health insurance costs. These include enrolling in Medicare, considering supplemental insurance plans, maintaining a healthy lifestyle to potentially qualify for lower premiums, and comparing plans from different providers to find the most cost-effective option.

Medicare is a federal health insurance program primarily for individuals aged 65 and older, but it also covers certain younger people with disabilities and those with End-Stage Renal Disease. At 62, you are not yet eligible for Medicare based on age alone. However, if you have a disability or specific medical condition, you might qualify for Medicare regardless of your age. Otherwise, you would need to wait until you turn 65 to enroll in Medicare.