The Affordable Care Act (ACA), commonly known as Obamacare, has been a subject of intense debate since its inception, particularly regarding its impact on health insurance costs. One of the primary goals of the ACA was to increase access to affordable health care for millions of Americans. However, opinions on whether it has successfully achieved this goal are sharply divided. Supporters argue that the ACA has led to significant improvements in health care accessibility and affordability, while critics contend that it has resulted in higher premiums and out-of-pocket costs for many individuals. This paragraph will delve into the complexities of the ACA's effects on health insurance expenses, examining both the positive and negative implications for consumers.

Explore related products

$11.49 $19.99

What You'll Learn

- Premium increases: Many Americans saw higher premiums after the Affordable Care Act's implementation

- Coverage changes: Some plans became more comprehensive, while others saw reduced coverage options

- Subsidy eligibility: Income thresholds for subsidies affected the affordability of insurance for some individuals

- Market competition: The number of insurers in certain areas decreased, potentially driving up costs

- Healthcare costs: Overall healthcare expenses continued to rise, impacting insurance prices

![]()

Premium increases: Many Americans saw higher premiums after the Affordable Care Act's implementation

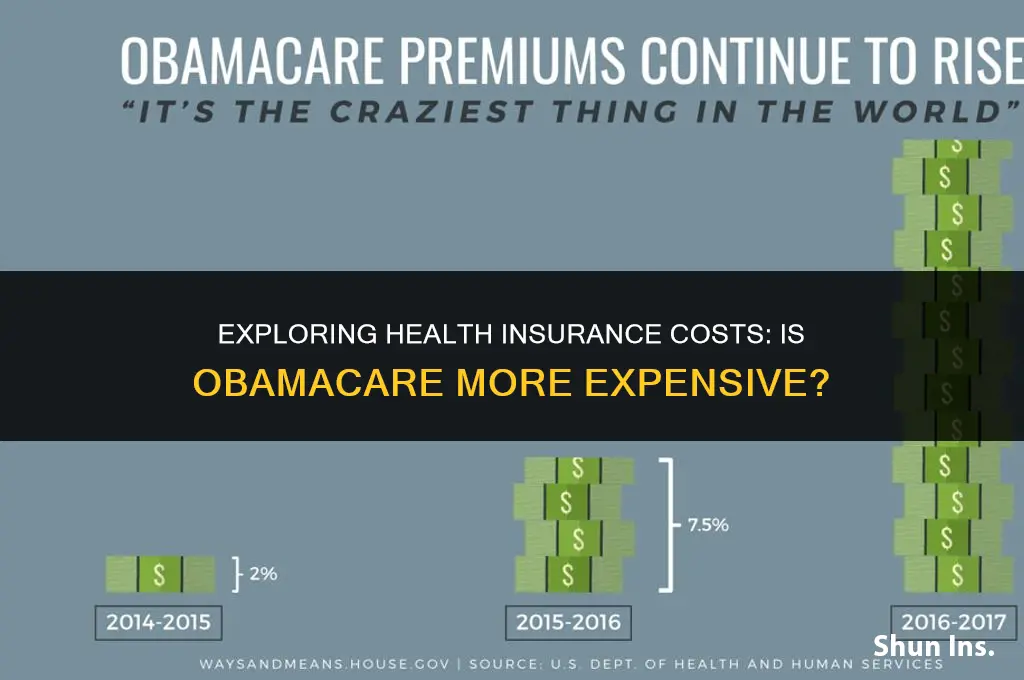

The implementation of the Affordable Care Act (ACA), commonly known as Obamacare, brought about significant changes to the health insurance landscape in the United States. One of the most notable impacts was the increase in premiums for many Americans. This phenomenon can be attributed to several factors, including the expansion of coverage to previously uninsured individuals, the introduction of new benefits and protections, and the changes in the risk pool composition.

Prior to the ACA, insurance companies could deny coverage or charge higher premiums to individuals with pre-existing conditions. The ACA prohibited these practices, leading to an influx of new enrollees who were previously unable to obtain insurance. This increased demand, coupled with the requirement for insurers to cover more benefits, such as preventive care and prescription drugs, contributed to the rise in premiums.

Furthermore, the ACA's individual mandate, which required most Americans to have health insurance or face a penalty, led to an increase in the number of young and healthy individuals purchasing insurance. This demographic shift resulted in a change in the risk pool composition, as insurers had to balance the costs of covering older and sicker individuals with the premiums collected from younger and healthier enrollees. Consequently, premiums increased for many Americans, particularly those in the individual market.

It is important to note that the impact of the ACA on premiums varied across different states and regions. Some states experienced more significant premium increases than others, depending on factors such as the local healthcare market, the level of competition among insurers, and the state's specific implementation of the ACA. Additionally, the premium increases were not uniform across all age groups, with younger individuals generally experiencing larger percentage increases in their premiums compared to older adults.

In conclusion, the premium increases observed after the implementation of the Affordable Care Act were a complex phenomenon resulting from a combination of factors, including the expansion of coverage, the introduction of new benefits, and the changes in the risk pool composition. While the ACA aimed to make healthcare more accessible and affordable for all Americans, the unintended consequence of higher premiums for some individuals highlights the ongoing challenges in achieving these goals.

Health Insurance's Hidden Costs: How Coverage Hurts American Families

You may want to see also

Explore related products

![]()

Coverage changes: Some plans became more comprehensive, while others saw reduced coverage options

Under the Affordable Care Act (ACA), commonly known as Obamacare, the landscape of health insurance coverage in the United States underwent significant changes. One of the most notable impacts was the alteration in the comprehensiveness of health plans available to consumers. While some plans became more comprehensive, offering a wider range of benefits and protections, others saw a reduction in coverage options, leaving policyholders with fewer choices and potentially higher out-of-pocket costs.

The ACA introduced new standards for health insurance plans, including the requirement that they cover essential health benefits such as preventive care, prescription drugs, and mental health services. This led to an increase in the comprehensiveness of many plans, as insurers were mandated to provide more extensive coverage to meet these standards. Additionally, the ACA prohibited insurers from denying coverage based on pre-existing conditions, which further enhanced the accessibility and comprehensiveness of health plans for many Americans.

However, the ACA also led to a reduction in coverage options for some individuals. Prior to the implementation of the ACA, consumers had a wider variety of plans to choose from, including high-deductible, low-premium plans that offered limited coverage. While these plans may not have provided comprehensive benefits, they were often more affordable for individuals who did not require extensive medical care. Under the ACA, these types of plans became less common, as they did not meet the new standards for essential health benefits. As a result, some consumers found themselves with fewer options for affordable, albeit less comprehensive, health insurance.

The changes in coverage options under the ACA had significant implications for the cost of health insurance. While the increased comprehensiveness of plans led to higher premiums for some policyholders, the reduction in coverage options also meant that individuals who previously had access to lower-cost, limited-coverage plans may have faced higher costs under the new system. This highlights the complex trade-offs involved in health care reform, where efforts to improve the quality and accessibility of care can also lead to increased costs for some consumers.

In conclusion, the ACA brought about a mixed bag of changes in terms of health insurance coverage. While it led to more comprehensive plans for many Americans, it also resulted in reduced coverage options for others. This underscores the importance of carefully considering the impact of health care policies on different segments of the population and the need for ongoing efforts to balance the goals of affordability, accessibility, and comprehensiveness in health insurance.

Medicare and Medical Insurance: What's the Difference?

You may want to see also

Explore related products

![]()

Subsidy eligibility: Income thresholds for subsidies affected the affordability of insurance for some individuals

The Affordable Care Act (ACA), commonly known as Obamacare, introduced significant changes to the healthcare system in the United States, including the provision of subsidies to make health insurance more affordable for lower-income individuals. However, the eligibility for these subsidies is determined by specific income thresholds, which have been a subject of debate and analysis.

One of the key aspects of the ACA's subsidy structure is that it is designed to assist those who earn between 100% and 400% of the Federal Poverty Level (FPL). This means that individuals with incomes slightly above the poverty line can receive substantial financial assistance to help cover the cost of their health insurance premiums. However, those who earn just above 400% of the FPL may find themselves in a situation where they are no longer eligible for subsidies, potentially leading to a significant increase in their insurance costs.

The impact of these income thresholds on the affordability of health insurance can be illustrated through various scenarios. For instance, a family of four earning $90,000 per year would be just below the 400% FPL threshold and could qualify for subsidies. However, if their income increased to $91,000, they would exceed the threshold and lose their subsidy eligibility, resulting in a substantial increase in their out-of-pocket insurance expenses.

Critics of the ACA argue that these income thresholds create a "cliff effect," where individuals are discouraged from earning more income due to the fear of losing their subsidies. This can lead to a situation where people may choose to work fewer hours or take lower-paying jobs to maintain their subsidy eligibility, potentially affecting their overall economic well-being.

On the other hand, proponents of the ACA argue that the subsidy structure is designed to target assistance to those who need it most. They point out that the majority of Americans do not earn close to the FPL and therefore would not be affected by these thresholds. Additionally, they argue that the ACA has helped millions of people gain access to affordable health insurance, which has had a positive impact on public health and the economy.

In conclusion, the income thresholds for subsidies under the ACA have had a significant impact on the affordability of health insurance for some individuals. While the subsidies have helped many lower-income Americans access healthcare, the cliff effect created by the income thresholds has also led to concerns about disincentivizing work and economic growth. As policymakers continue to debate the future of healthcare reform, the subsidy eligibility rules are likely to remain a key point of discussion.

Adding Your Fiancé to Health Insurance: A Step-by-Step Guide

You may want to see also

Explore related products

![Life and Health Insurance License Study Cards: Life Health Insurance Exam Prep with Practice Test Questions [Full Color]](https://m.media-amazon.com/images/I/51Pox87Z5lL._AC_UY218_.jpg)

![]()

Market competition: The number of insurers in certain areas decreased, potentially driving up costs

The reduction in the number of insurers in certain areas has led to a significant decrease in market competition, which is a key factor in driving up health insurance costs. When there are fewer insurers competing for customers, they have less incentive to keep prices low, leading to higher premiums for consumers. This phenomenon is particularly evident in rural areas, where the lack of competition has resulted in some of the highest insurance rates in the country.

One of the main reasons for the decrease in the number of insurers is the consolidation of the health insurance industry. Over the past few decades, there has been a wave of mergers and acquisitions among insurers, leading to a significant reduction in the number of players in the market. This consolidation has been driven by a number of factors, including the increasing cost of providing health care, the need for economies of scale, and the desire to expand market share.

Another factor contributing to the decrease in competition is the regulatory environment. The Affordable Care Act (ACA), also known as Obamacare, has imposed a number of regulations on the health insurance industry, which has made it more difficult for new insurers to enter the market. These regulations include requirements for insurers to cover certain essential health benefits, limits on the amount of profit insurers can make, and restrictions on the ability of insurers to discriminate against customers with pre-existing conditions.

The lack of competition has also led to a decrease in the quality of health insurance plans available to consumers. When there are fewer insurers competing for customers, they have less incentive to offer high-quality plans that meet the needs of consumers. This has resulted in a proliferation of low-quality plans that offer limited coverage and high out-of-pocket costs.

To address the issue of decreased competition, policymakers have proposed a number of solutions, including increasing the number of insurers in the market, relaxing regulations on the health insurance industry, and promoting greater transparency in the pricing of health insurance plans. However, these solutions are not without their challenges, and it remains to be seen whether they will be effective in reducing health insurance costs and improving the quality of care for consumers.

Understanding Home Insurance: Medical Coverage and Your Options

You may want to see also

Explore related products

![]()

Healthcare costs: Overall healthcare expenses continued to rise, impacting insurance prices

The relentless upward trajectory of healthcare costs has been a persistent challenge, exerting significant pressure on insurance prices. This trend is multifaceted, driven by a combination of factors including the increasing cost of medical services, pharmaceuticals, and administrative expenses. As healthcare providers face rising operational costs, these expenses are often passed on to insurers, who in turn must adjust their premiums to maintain financial viability.

One of the key contributors to escalating healthcare costs is the growing demand for specialized care and advanced medical technologies. As the population ages and chronic diseases become more prevalent, the need for sophisticated treatments and long-term care increases. This heightened demand, coupled with a shortage of healthcare professionals in certain specialties, drives up the cost of care. Additionally, the development and implementation of new medical technologies, while often improving patient outcomes, come with hefty price tags that further inflate healthcare expenses.

Pharmaceutical costs also play a significant role in the rising healthcare expenditures. The prices of prescription drugs have been increasing steadily, with some medications experiencing dramatic price hikes. This trend is partly due to the high cost of drug development and the need for pharmaceutical companies to recoup their investments. Furthermore, the lack of price regulation and the complex dynamics of the drug supply chain contribute to the upward spiral of medication costs.

Administrative expenses, though often overlooked, are another substantial component of healthcare costs. The complexity of the healthcare system, with its myriad of billing codes, compliance requirements, and administrative tasks, necessitates a significant investment in administrative infrastructure. These costs, which include everything from staffing and training to software and facilities, are ultimately borne by insurers and contribute to higher premiums.

In conclusion, the rising tide of healthcare costs is a complex issue with far-reaching implications for insurance prices. Addressing this challenge requires a multifaceted approach that targets the various drivers of cost inflation, from medical services and pharmaceuticals to administrative expenses. By understanding the underlying factors contributing to this trend, stakeholders can work towards developing effective strategies to mitigate its impact and ensure the sustainability of the healthcare system.

Does Health Insurance Cover Vasectomies? Understanding Coverage and Costs

You may want to see also

Frequently asked questions

The Affordable Care Act (ACA), commonly known as Obamacare, has had varying impacts on health insurance premiums. For some individuals, particularly those with pre-existing conditions or those who were previously uninsured, the ACA has made health insurance more affordable. However, for others, especially younger and healthier individuals, premiums may have increased due to the requirement to cover essential health benefits and the prohibition on denying coverage based on health status.

Several factors influence the cost of health insurance under the ACA. These include the essential health benefits that must be covered, such as preventive care, prescription drugs, and maternity care. Additionally, the ACA's requirement for insurers to accept all applicants regardless of health status can lead to higher premiums to offset the costs of covering individuals with pre-existing conditions. The age of the insured individual also plays a role, as older individuals tend to have higher healthcare costs.

The ACA includes provisions aimed at making health insurance more affordable for low-income individuals. These include Medicaid expansion, which provides coverage to eligible low-income adults, and the availability of premium tax credits and cost-sharing reductions for those purchasing insurance through the health insurance marketplace. These subsidies can significantly reduce the out-of-pocket costs for low-income individuals, making health insurance more accessible and affordable.