Health insurance is a crucial aspect of financial planning and management, and understanding its relationship with net income is essential for individuals and businesses alike. Net income, also known as net earnings or net profit, is the amount of money left over after all expenses, including taxes and operating costs, have been deducted from total revenue. In the context of health insurance, the question arises as to whether the premiums paid for health coverage should be considered an expense that reduces net income. This is a complex issue with various factors to consider, including the type of health insurance plan, the entity paying the premiums, and the tax implications involved.

| Characteristics | Values |

|---|---|

| Definition | Health insurance is a type of insurance coverage that pays for medical and surgical expenses incurred by the insured. Net income refers to the total earnings of an individual or business after deducting all expenses, including taxes and interest. |

| Inclusion in Net Income | Health insurance premiums are generally considered an expense and are deducted from gross income to calculate net income. |

| Tax Implications | In some cases, health insurance premiums may be tax-deductible, which can reduce the taxable income and therefore increase the net income. |

| Employer-Provided Insurance | If an employer provides health insurance as a benefit, the premiums paid by the employer are typically not included in the employee's gross income, thus not affecting their net income. |

| Individual Insurance | For individuals who purchase their own health insurance, premiums are usually paid with after-tax dollars, reducing their net income. |

| Health Savings Accounts (HSAs) | Contributions to HSAs are tax-deductible and can be used to pay for qualified medical expenses, potentially reducing the impact of health insurance costs on net income. |

| Flexible Spending Accounts (FSAs) | Similar to HSAs, FSAs allow individuals to set aside pre-tax dollars for medical expenses, which can help lower the net cost of health insurance. |

| Impact on Business Net Income | For businesses, health insurance premiums paid for employees can be deducted as a business expense, reducing the company's net income. |

| Subsidies and Credits | Government subsidies and tax credits for health insurance can help reduce the net cost of insurance for individuals and businesses. |

| Economic Factors | Changes in healthcare costs, insurance premiums, and tax laws can all impact the relationship between health insurance and net income. |

| Personal Financial Planning | Understanding the relationship between health insurance and net income is crucial for effective personal financial planning and budgeting. |

| Business Financial Planning | Businesses must also consider the impact of health insurance costs on their net income when making financial decisions and planning for the future. |

Explore related products

What You'll Learn

- Definition of Net Income: Understanding net income and its components, including revenues and expenses

- Health Insurance Costs: Exploring how health insurance premiums and out-of-pocket costs impact net income

- Tax Implications: Discussing the tax treatment of health insurance expenses and their effect on net income

- Accounting Practices: Reviewing how health insurance costs are recorded and reported in financial statements

- Economic Impact: Analyzing the broader economic effects of health insurance on individuals and businesses' net income

![]()

Definition of Net Income: Understanding net income and its components, including revenues and expenses

Net income is a fundamental concept in accounting and finance, representing the total earnings of a business after all expenses have been deducted from its revenues. It is often referred to as the "bottom line" because it appears at the bottom of an income statement. Understanding net income is crucial for business owners, investors, and analysts as it provides insight into a company's profitability and financial health.

Revenues are the total amounts earned by a business from its primary activities, such as selling goods or services. Expenses, on the other hand, are the costs incurred by the business to generate these revenues. These can include direct costs like materials and labor, as well as indirect costs like rent, utilities, and administrative expenses. The difference between revenues and expenses is what constitutes net income.

For example, if a company generates $100,000 in revenues and incurs $60,000 in expenses, its net income would be $40,000. This figure can be used to assess the company's performance over a specific period, such as a quarter or a year, and can be compared to previous periods to identify trends and areas for improvement.

Net income is not only important for internal analysis but also for external stakeholders. Investors, for instance, use net income to evaluate the profitability of a company and make informed decisions about whether to invest in it. Lenders may also consider a company's net income when determining its creditworthiness.

In the context of health insurance, it is important to note that health insurance premiums paid by a business are typically considered an expense. This means that they are deducted from revenues when calculating net income. However, the specifics can vary depending on the accounting standards and regulations applicable to the business. For instance, in some cases, health insurance premiums may be partially deductible or may need to be capitalized and amortized over time.

In conclusion, net income is a critical financial metric that provides valuable insights into a company's profitability and financial performance. By understanding the components of net income, including revenues and expenses, business owners and stakeholders can make more informed decisions and develop strategies for growth and improvement.

Who Protects Rental Equipment Companies: Insurance Insights and Coverage Explained

You may want to see also

Explore related products

![]()

Health Insurance Costs: Exploring how health insurance premiums and out-of-pocket costs impact net income

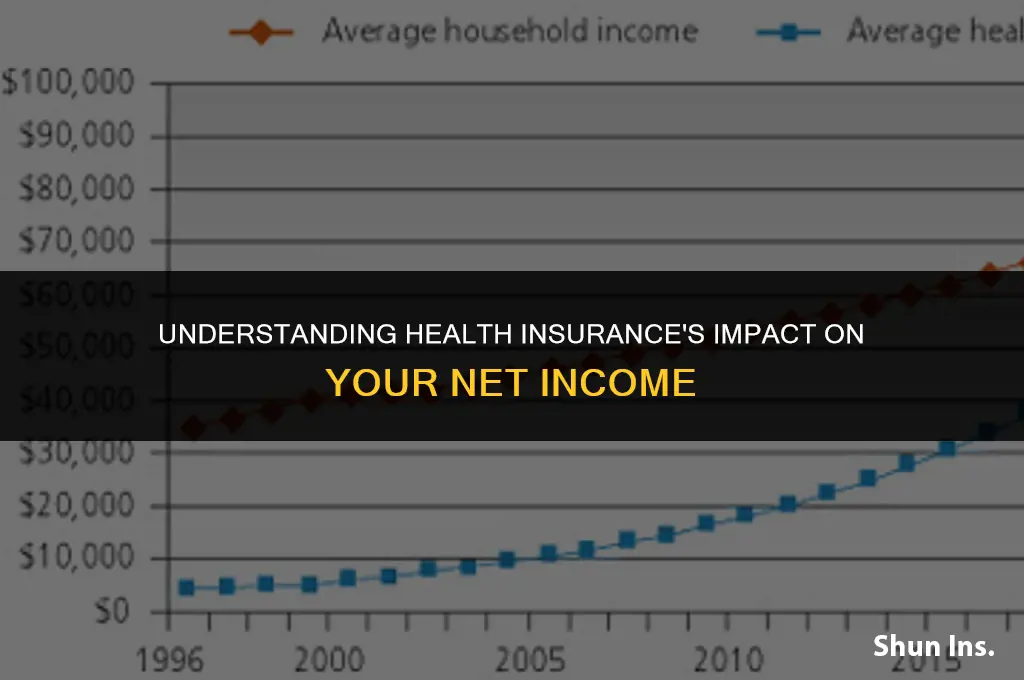

Health insurance costs can significantly impact an individual's net income, as premiums and out-of-pocket expenses can add up quickly. Premiums are the monthly payments made to the insurance company to maintain coverage, while out-of-pocket costs include deductibles, copays, and coinsurance. These costs can vary widely depending on the type of insurance plan, the individual's health status, and the healthcare services utilized.

One way to explore the impact of health insurance costs on net income is to calculate the total annual cost of premiums and out-of-pocket expenses. This can be done by reviewing the insurance plan's summary of benefits and coverage, which outlines the expected costs for different healthcare services. By comparing these costs to the individual's annual income, it is possible to determine the percentage of income that is allocated towards health insurance expenses.

For example, if an individual has a monthly premium of $500 and an annual deductible of $2,000, their total annual health insurance cost would be $8,000 ($500 x 12 + $2,000). If their annual income is $50,000, then 16% of their income is allocated towards health insurance expenses ($8,000 / $50,000).

Another factor to consider is the impact of health insurance costs on retirement savings. As individuals approach retirement age, they may need to allocate a larger portion of their income towards healthcare expenses, which can reduce the amount of money available for retirement savings. This can be particularly challenging for those who are self-employed or do not have access to employer-sponsored health insurance plans.

To mitigate the impact of health insurance costs on net income, individuals can explore various strategies, such as choosing a high-deductible health plan (HDHP) or a health savings account (HSA). HDHPs typically have lower premiums but higher deductibles, which can be beneficial for individuals who are generally healthy and do not require frequent healthcare services. HSAs are tax-advantaged accounts that can be used to save money for healthcare expenses, and they can be particularly useful for those who have a high-deductible health plan.

In conclusion, health insurance costs can have a significant impact on an individual's net income, and it is important to carefully consider these costs when making financial decisions. By calculating the total annual cost of premiums and out-of-pocket expenses, comparing these costs to annual income, and exploring strategies to mitigate these costs, individuals can better manage their healthcare expenses and maintain a healthy financial outlook.

Hawaii Employers: Medical Insurance and ACA Compliance

You may want to see also

Explore related products

![]()

Tax Implications: Discussing the tax treatment of health insurance expenses and their effect on net income

The tax treatment of health insurance expenses can have a significant impact on an individual's net income. In many jurisdictions, health insurance premiums are considered a deductible expense, which means they can be subtracted from taxable income, thereby reducing the amount of tax owed. This can be particularly beneficial for self-employed individuals or those with high medical expenses.

For example, in the United States, individuals who are self-employed can deduct the cost of their health insurance premiums from their taxable income. This deduction is available whether they itemize their deductions or take the standard deduction. However, it's important to note that this deduction is only available for premiums paid for the individual, their spouse, and their dependents.

In addition to the deduction for health insurance premiums, some jurisdictions also offer tax credits for health insurance expenses. A tax credit is a dollar-for-dollar reduction in the amount of tax owed, which can be even more valuable than a deduction. For instance, the Affordable Care Act in the United States provides a tax credit to help make health insurance more affordable for low- and middle-income individuals.

The impact of these tax benefits on net income can be substantial. By reducing taxable income, individuals can potentially move into a lower tax bracket, which can result in even greater savings. Furthermore, the ability to deduct or receive a credit for health insurance expenses can make it more feasible for individuals to afford comprehensive coverage, which can lead to better health outcomes and reduced out-of-pocket expenses in the long run.

It's important to consult with a tax professional to understand the specific tax implications of health insurance expenses in your jurisdiction. They can help you navigate the complex rules and regulations surrounding health insurance and taxes, and ensure that you are taking advantage of all available deductions and credits.

Will Health Insurers Mandate COVID-19 Vaccination for Coverage?

You may want to see also

Explore related products

![]()

Accounting Practices: Reviewing how health insurance costs are recorded and reported in financial statements

In the realm of financial reporting, the treatment of health insurance costs is a critical aspect that demands meticulous attention. These costs are typically recorded as expenses on the income statement, reducing the net income of the entity. However, the specific accounting practices can vary depending on the nature of the health insurance plan and the regulatory framework governing the entity.

For instance, if an entity offers a self-insured health plan, it would need to record the costs of providing health care services to employees as expenses when incurred. This could include premiums paid to insurance carriers, administrative costs, and the costs of health care services provided to employees. On the other hand, if an entity purchases health insurance from a third-party insurer, it would typically record the premiums paid as expenses when incurred.

It's also important to consider the timing of when these costs are recorded. In some cases, health insurance costs may be accrued over time, rather than being expensed immediately. This could be the case if an entity has a health insurance plan that covers multiple years or if it has a self-insured plan that pays out claims over time.

In addition to the timing of when health insurance costs are recorded, entities must also consider how these costs are reported in their financial statements. For example, health insurance costs may be reported as a separate line item on the income statement, or they may be included in a broader category of employee benefits. The specific reporting requirements can vary depending on the accounting standards and regulatory requirements that govern the entity.

Ultimately, the accurate recording and reporting of health insurance costs is essential for ensuring the financial statements of an entity are accurate and reliable. This requires a thorough understanding of the specific accounting practices and regulatory requirements that apply to the entity's health insurance plans. By carefully considering these factors, entities can ensure their financial statements accurately reflect the costs associated with providing health insurance to their employees.

Do C Corps Have to Provide Health Insurance? Key Insights

You may want to see also

Explore related products

![]()

Economic Impact: Analyzing the broader economic effects of health insurance on individuals and businesses' net income

The economic impact of health insurance on individuals and businesses is multifaceted, influencing both net income and broader financial stability. For individuals, health insurance can significantly reduce out-of-pocket medical expenses, thereby increasing disposable income and potentially boosting savings or investments. Conversely, high premiums or deductibles can strain household budgets, reducing net income and limiting financial flexibility.

For businesses, the provision of health insurance to employees can be a substantial expense, affecting net income through increased operational costs. However, offering health benefits can also enhance employee retention and productivity, indirectly contributing to revenue growth and profitability. Moreover, businesses may benefit from tax deductions related to health insurance premiums, mitigating some of the financial burden.

Analyzing the broader economic effects, health insurance plays a crucial role in risk management, protecting individuals and businesses from catastrophic medical expenses. This risk mitigation can lead to increased financial security and stability, fostering economic growth and resilience. Additionally, the health insurance industry itself is a significant sector, generating employment and contributing to GDP.

In conclusion, the economic impact of health insurance is complex, with both positive and negative effects on net income and financial well-being. Understanding these dynamics is essential for individuals and businesses to make informed decisions about health insurance coverage and for policymakers to develop effective healthcare strategies.

Denied Insurance Claim? Understanding Common Reasons and Your Next Steps

You may want to see also

Frequently asked questions

Health insurance is generally not considered part of net income. Net income is the amount of money you earn after taxes and other deductions, while health insurance is typically a benefit provided by employers or purchased individually to cover medical expenses.

Health insurance can affect net income indirectly. For example, if your employer provides health insurance as part of your compensation package, it may reduce your taxable income, which in turn can increase your net income. However, if you pay for health insurance out-of-pocket, it may decrease your net income due to the additional expense.

Health insurance premiums can be tax-deductible if you itemize your deductions on your tax return. However, if you have employer-sponsored health insurance, the premiums are typically not deductible because they are considered a tax-free benefit.

Health insurance is often related to gross income because it is typically provided as a benefit by employers. Your gross income includes your wages, salary, tips, and other earnings before taxes and deductions. If your employer provides health insurance, it may be included as part of your gross income, but it is not considered taxable income.

The Affordable Care Act (ACA) has several provisions that can impact health insurance and net income. For example, the ACA requires employers to provide health insurance to full-time employees or pay a penalty. This can increase the cost of health insurance for employers, which may be passed on to employees through higher premiums or reduced wages. Additionally, the ACA provides subsidies to individuals who purchase health insurance through the health insurance marketplace, which can help reduce the cost of health insurance and increase net income for those who qualify.