Health insurance is a crucial aspect of financial planning, and understanding what qualifies as a health insurance expense is essential for making informed decisions. In general, health insurance premiums, deductibles, copays, and coinsurance are considered qualified expenses. These costs can be substantial, and knowing how to manage them effectively can help individuals and families save money and ensure they have access to the care they need. Additionally, it's important to be aware of any tax implications or employer-provided benefits that may impact the qualification of health insurance expenses. By taking the time to educate oneself on these matters, individuals can make the most of their health insurance coverage and minimize their out-of-pocket costs.

| Characteristics | Values |

|---|---|

| Definition | An expense that qualifies under the IRS rules for health insurance deductibility |

| Eligibility | Must be a medical expense paid during the tax year for the taxpayer, spouse, or dependents |

| Coverage | Includes premiums for health insurance, long-term care insurance, and Medicare |

| Exclusions | Does not include expenses for cosmetic surgery, except for certain reconstructive procedures |

| Limitations | Subject to a threshold of 7.5% of adjusted gross income (AGI) for taxpayers under 65 |

| Threshold | For those over 65, the threshold is 5% of AGI |

| Documentation | Requires itemization of deductions on Schedule A of Form 1040 |

| Impact on Taxes | Reduces taxable income, potentially lowering the tax bracket |

| Interaction with HSA | Can be used in conjunction with Health Savings Accounts (HSAs) for additional tax benefits |

| Changes Over Time | Tax laws and thresholds may change from year to year, affecting the qualification criteria |

| State Variations | Some states may have different rules or additional benefits for health insurance expenses |

| Dependents | Expenses for dependents can be included if they meet the IRS definition of a dependent |

| Self-Employed | Self-employed individuals may have different rules and limitations for deducting health insurance premiums |

| Military | Military personnel may have special rules and exclusions for health insurance expenses |

| Veterans | Veterans may be eligible for additional benefits or deductions related to health insurance |

| Disabled | Individuals with disabilities may have different thresholds or additional deductions available |

Explore related products

What You'll Learn

- IRS Guidelines: Understanding what the IRS considers a qualified health expense for tax deductions

- Medical Necessity: Determining if health insurance covers treatments deemed medically necessary

- Out-of-Pocket Costs: Exploring how out-of-pocket medical expenses factor into qualified health expenses

- Preventive Care: Investigating if health insurance includes preventive care as a qualified expense

- State-Specific Rules: Examining how state laws influence the definition of qualified health expenses

![]()

IRS Guidelines: Understanding what the IRS considers a qualified health expense for tax deductions

The IRS has specific guidelines regarding what constitutes a qualified health expense for tax deduction purposes. These guidelines are crucial for taxpayers looking to maximize their deductions and minimize their taxable income. A qualified health expense is generally defined as an expense that is incurred for the diagnosis, cure, mitigation, treatment, or prevention of a disease, or for the purpose of affecting any bodily function.

One important aspect of these guidelines is the distinction between qualified health expenses and expenses that are considered personal in nature. For example, expenses for cosmetic surgery are typically not deductible unless they are medically necessary. Similarly, expenses for health club memberships or spa treatments are generally not deductible, as they are considered personal expenses rather than medical expenses.

The IRS also has specific rules regarding the documentation required to substantiate qualified health expenses. Taxpayers must keep records of their medical expenses, including receipts, invoices, and explanations of benefits from their health insurance provider. These records must be maintained for at least three years from the date the tax return is filed.

Another key consideration is the impact of the Affordable Care Act (ACA) on qualified health expenses. The ACA introduced new rules and regulations regarding health insurance coverage and tax deductions. For example, the ACA limits the amount of medical expenses that can be deducted from taxable income for individuals under the age of 65.

In addition to these general guidelines, there are specific rules for certain types of health expenses. For example, the IRS has rules regarding the deductibility of long-term care expenses, which are expenses incurred for the care of individuals who are unable to perform certain activities of daily living. There are also rules regarding the deductibility of health insurance premiums, which can be complex and vary depending on the taxpayer's situation.

Understanding these IRS guidelines is essential for taxpayers looking to take advantage of tax deductions for qualified health expenses. By keeping accurate records and staying informed about the latest rules and regulations, taxpayers can ensure that they are maximizing their deductions and minimizing their taxable income.

Adding Your Parents to Your Medical Insurance: Is it Possible?

You may want to see also

Explore related products

![Life and Health Insurance License Study Cards: Life Health Insurance Exam Prep with Practice Test Questions [Full Color]](https://m.media-amazon.com/images/I/51Pox87Z5lL._AC_UY218_.jpg)

$43.99 $55.99

![]()

Medical Necessity: Determining if health insurance covers treatments deemed medically necessary

Determining whether a treatment is medically necessary is a critical aspect of understanding what health insurance covers. Medical necessity is often defined as a treatment or service that is essential for the diagnosis, treatment, or management of a medical condition, and is consistent with generally accepted medical practice. Insurance companies typically require that treatments meet this criterion to be considered covered expenses.

To navigate this determination, it's important to understand the process. First, a healthcare provider must evaluate the patient's condition and recommend a treatment plan. This plan should be based on the provider's professional judgment and should align with established medical guidelines. The insurance company will then review the treatment plan to determine if it meets their criteria for medical necessity. This review may involve consulting with medical experts or using evidence-based guidelines to assess the appropriateness of the treatment.

One of the challenges in determining medical necessity is the subjective nature of the evaluation. Different insurance companies may have different criteria, and even within the same company, different reviewers may come to different conclusions. This can lead to disputes between patients, providers, and insurers. To mitigate these disputes, many insurance companies have established clear guidelines and protocols for reviewing medical necessity, and some may even have an appeals process for patients who disagree with the initial decision.

Patients can also play a role in ensuring that their treatments are deemed medically necessary. By working closely with their healthcare providers and insurance companies, patients can help to ensure that their treatment plans are well-documented and meet the necessary criteria. This may involve providing detailed information about their medical history, current condition, and the impact of their symptoms on their daily lives.

In conclusion, determining medical necessity is a complex process that involves careful evaluation by healthcare providers and insurance companies. By understanding the criteria and process involved, patients can better navigate the system and ensure that they receive the treatments they need.

Uninsured Veterans: Addressing the Gap in Healthcare Coverage for Heroes

You may want to see also

Explore related products

![]()

Out-of-Pocket Costs: Exploring how out-of-pocket medical expenses factor into qualified health expenses

Out-of-pocket medical expenses are a critical component of qualified health expenses, and understanding how they factor into your overall healthcare costs is essential for making informed financial decisions. These expenses include any payments you make directly to healthcare providers or for medical supplies that are not covered by your health insurance plan. They can encompass a wide range of costs, from copayments and coinsurance to deductibles and the full cost of services not included in your plan's network.

One of the key considerations when evaluating out-of-pocket costs is the impact they can have on your ability to afford necessary medical care. High out-of-pocket expenses can deter individuals from seeking timely treatment, leading to potential health complications and increased costs in the long run. To mitigate these risks, it's important to carefully review your health insurance plan's coverage details and understand what expenses you may be responsible for.

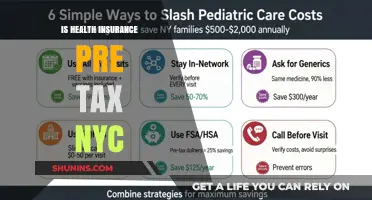

When exploring how out-of-pocket medical expenses factor into qualified health expenses, it's also crucial to consider the tax implications. In many cases, out-of-pocket medical expenses can be deducted from your taxable income, reducing your overall tax liability. However, to qualify for these deductions, expenses must meet certain criteria, such as being medically necessary and exceeding a specific percentage of your adjusted gross income.

To effectively manage out-of-pocket costs, it's advisable to maintain detailed records of all medical expenses, including receipts, invoices, and explanations of benefits. This documentation can be invaluable when filing tax returns or appealing insurance claims. Additionally, individuals may want to consider setting aside funds in a health savings account (HSA) or flexible spending account (FSA) to cover out-of-pocket expenses, as these accounts offer tax advantages and can help mitigate the financial burden of unexpected medical costs.

In conclusion, out-of-pocket medical expenses play a significant role in determining the overall affordability of healthcare. By understanding how these costs factor into qualified health expenses and taking proactive steps to manage them, individuals can make more informed decisions about their healthcare and financial well-being.

Capital One Post-Retirement Health Insurance: What You Need to Know

You may want to see also

Explore related products

$17.78 $19.99

![]()

Preventive Care: Investigating if health insurance includes preventive care as a qualified expense

Preventive care is a crucial aspect of maintaining good health, and it's essential to understand whether your health insurance covers these services. Many health insurance plans include preventive care as a qualified expense, but the specifics can vary widely depending on the policy and the insurance provider.

To determine if your health insurance covers preventive care, you should start by reviewing your policy documents or contacting your insurance provider directly. Look for specific mentions of preventive care services, such as annual check-ups, vaccinations, or screenings for various health conditions. Some policies may cover these services in full, while others may require a copay or deductible.

It's also important to understand what types of preventive care services are covered. For example, some policies may cover routine dental cleanings or eye exams, while others may not. Additionally, some policies may have age or gender-specific preventive care recommendations, such as mammograms for women or prostate screenings for men.

When investigating your coverage, be sure to ask about any limitations or exclusions. For instance, some policies may only cover preventive care services if they are performed by in-network providers or if they are deemed medically necessary. Understanding these nuances can help you make informed decisions about your healthcare and avoid unexpected costs.

In conclusion, preventive care is an essential component of maintaining good health, and it's crucial to understand whether your health insurance covers these services. By reviewing your policy documents, contacting your insurance provider, and asking about specific preventive care services, you can ensure that you are making the most of your health insurance coverage and taking proactive steps to protect your health.

Top UAE Insurance Companies: A Comprehensive Guide to the Best

You may want to see also

Explore related products

![]()

State-Specific Rules: Examining how state laws influence the definition of qualified health expenses

The definition of qualified health expenses can vary significantly from state to state, as each state has its own set of laws and regulations governing health insurance. For example, some states may consider certain medical procedures or treatments as qualified expenses, while others may not. Additionally, the amount of coverage provided for qualified expenses can also differ between states.

One key factor influencing the definition of qualified health expenses is the state's adoption of the Affordable Care Act (ACA). States that have expanded Medicaid under the ACA may have a broader definition of qualified expenses, as they are required to cover a wider range of health services. On the other hand, states that have not expanded Medicaid may have a more limited definition of qualified expenses.

Another factor to consider is the state's insurance regulations. Some states may have stricter regulations on what health insurance plans must cover, which can impact the definition of qualified expenses. For instance, a state may require insurance plans to cover certain preventive care services or mental health treatments, which would then be considered qualified expenses.

Furthermore, state laws may also dictate the process for determining whether a health expense is qualified. This could include requirements for prior authorization or utilization review, which can affect how quickly and easily an expense is deemed qualified.

In conclusion, the definition of qualified health expenses is not uniform across states, and can be influenced by a variety of factors including the state's adoption of the ACA, insurance regulations, and laws governing the determination of qualified expenses. It is important for individuals to understand their state's specific rules when it comes to health insurance coverage.

Who Insures Fracking Companies: Unveiling the Risky Business Coverage

You may want to see also

Frequently asked questions

A qualified health expense is a medical expense that is eligible for tax-free treatment under a health savings account (HSA), health reimbursement arrangement (HRA), or flexible spending account (FSA). These expenses typically include costs for medical care, dental care, vision care, and prescription medications, as well as other health-related expenses such as acupuncture, chiropractic care, and physical therapy.

To determine if your health insurance covers qualified expenses, you should review your plan's summary of benefits and coverage or contact your insurance provider directly. Your plan may have specific requirements or limitations for certain types of medical expenses, so it's important to understand what is covered and what is not.

Generally, you cannot use your HSA, HRA, or FSA to pay for health insurance premiums. However, there are some exceptions, such as if you are self-employed or if your employer offers a qualified small employer health reimbursement arrangement (QSEHRA). It's important to check with your plan administrator or tax advisor to determine if you are eligible to use your account to pay for health insurance premiums.

If you use your HSA, HRA, or FSA to pay for a non-qualified expense, you may be subject to taxes and penalties. For HSAs, you may have to pay a 20% penalty on the amount withdrawn for non-qualified expenses, in addition to any taxes owed. For HRAs and FSAs, you may have to repay the amount withdrawn for non-qualified expenses to your employer or plan administrator. It's important to carefully review your plan's rules and regulations to avoid any unexpected taxes or penalties.