The question of whether health insurance is worthless is a complex and multifaceted one, influenced by various factors including personal health needs, financial circumstances, and the quality of available healthcare services. Health insurance is designed to provide financial protection against medical expenses, but its value can be perceived differently by individuals based on their unique situations. For some, health insurance may be invaluable, offering peace of mind and access to necessary medical care without incurring substantial out-of-pocket costs. For others, it might seem like an unnecessary expense, especially if they are generally healthy and seldom require medical attention. The debate surrounding the worthiness of health insurance often centers around issues such as premiums, deductibles, coverage limitations, and the overall efficiency of the healthcare system. Ultimately, determining whether health insurance is worthwhile requires a careful consideration of these factors and how they align with an individual's priorities and circumstances.

Explore related products

What You'll Learn

- High Premiums vs. Limited Coverage: Exploring the balance between the cost of insurance and the benefits provided

- Deductibles and Out-of-Pocket Costs: Discussing how high deductibles and additional costs impact the affordability of healthcare

- Network Restrictions: Examining the limitations imposed by insurance networks on healthcare provider choices

- Pre-Existing Conditions: Addressing how insurance companies handle coverage for individuals with pre-existing health issues

- Preventive Care and Wellness Programs: Evaluating the effectiveness of insurance-sponsored programs in promoting health and preventing illness

![]()

High Premiums vs. Limited Coverage: Exploring the balance between the cost of insurance and the benefits provided

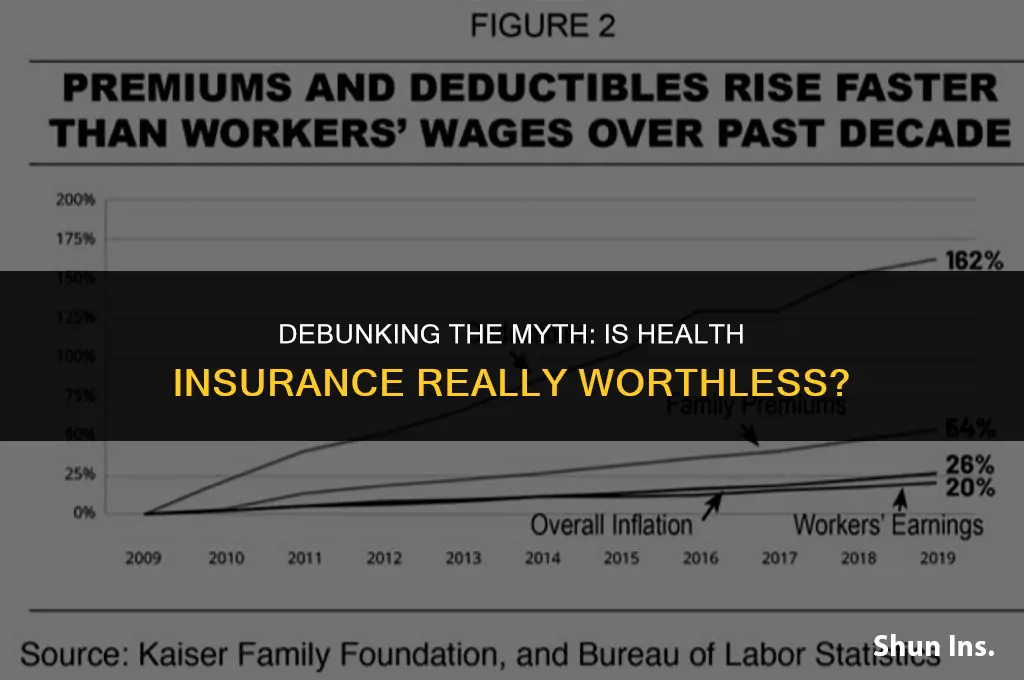

The debate over health insurance often centers on the tension between high premiums and limited coverage. On one hand, insurance companies argue that high premiums are necessary to cover the costs of providing comprehensive care. On the other hand, consumers may feel that they are paying too much for coverage that does not adequately meet their needs. This section will explore the balance between the cost of insurance and the benefits provided, examining the factors that contribute to high premiums and limited coverage, as well as potential solutions to this dilemma.

One of the primary drivers of high premiums is the cost of healthcare itself. As medical expenses continue to rise, insurance companies must increase their premiums to keep up. Additionally, the Affordable Care Act (ACA) has imposed new regulations on insurance companies, which have also contributed to higher premiums. For example, the ACA requires insurers to cover pre-existing conditions, which can be costly. Furthermore, the ACA's individual mandate, which requires most Americans to have health insurance or pay a penalty, has led to an increase in the number of people purchasing insurance, which has also driven up premiums.

Limited coverage is often a result of insurance companies trying to control costs. By offering plans with higher deductibles, copays, and coinsurance, insurers can reduce their out-of-pocket expenses, which in turn allows them to offer lower premiums. However, this can also lead to consumers feeling that they are not getting adequate coverage. For example, a plan with a high deductible may not provide much benefit to someone who does not have many medical expenses. Additionally, some plans may not cover certain services or treatments, which can leave consumers feeling unprotected.

There are several potential solutions to the problem of high premiums and limited coverage. One approach is to increase competition in the insurance market. By allowing insurance companies to compete across state lines, consumers may have more options to choose from, which could lead to lower premiums and better coverage. Another solution is to implement cost-saving measures, such as promoting preventive care and reducing administrative costs. Finally, policymakers could consider implementing a public option, which would provide consumers with an alternative to private insurance.

In conclusion, the balance between high premiums and limited coverage is a complex issue that requires careful consideration. While there are no easy solutions, it is important to continue exploring ways to make health insurance more affordable and accessible to all Americans.

AARP Life Insurance: Medical Questions Answered

You may want to see also

Explore related products

![]()

Deductibles and Out-of-Pocket Costs: Discussing how high deductibles and additional costs impact the affordability of healthcare

High deductibles and out-of-pocket costs are significant factors contributing to the perception that health insurance may be worthless. When individuals face substantial financial burdens before their insurance coverage kicks in, it can create a sense of frustration and hopelessness. For many, the promise of health insurance is tarnished by the reality of high upfront costs, making it difficult to afford necessary medical care.

One of the primary issues with high deductibles is that they can deter people from seeking preventive care or early treatment for health issues. When faced with the prospect of paying a large sum out of pocket before insurance coverage begins, individuals may delay or forgo medical attention altogether. This can lead to worsening health conditions, ultimately resulting in more expensive treatments and potentially poorer health outcomes.

Furthermore, out-of-pocket costs, such as copays and coinsurance, can add up quickly, especially for those with chronic conditions or requiring ongoing medical care. These additional expenses can strain household budgets, forcing individuals to make difficult choices between their health and other financial obligations. The cumulative effect of these costs can make health insurance feel more like a financial burden than a safety net.

It is also important to consider the impact of high deductibles and out-of-pocket costs on vulnerable populations, such as low-income individuals and families. For these groups, the financial barriers to accessing healthcare can be particularly insurmountable, exacerbating existing health disparities and contributing to a cycle of poverty and poor health.

In conclusion, the issue of high deductibles and out-of-pocket costs is a critical aspect of the debate surrounding the value of health insurance. Addressing these financial barriers is essential to ensuring that health insurance truly serves its purpose of providing accessible and affordable healthcare to all.

Understanding the Value of Silver 2300 Select Health Insurance Plan

You may want to see also

Explore related products

![]()

Network Restrictions: Examining the limitations imposed by insurance networks on healthcare provider choices

Insurance networks significantly limit the choices available to healthcare providers, often dictating which doctors and facilities are considered "in-network" and therefore eligible for reimbursement. This can result in patients being forced to choose from a restricted list of providers, potentially compromising the quality of care they receive. For example, a patient with a complex medical condition may find that the specialists they need are not included in their insurance network, leaving them with limited options for treatment.

Furthermore, these network restrictions can lead to higher out-of-pocket costs for patients, as they may be required to pay more for services rendered by out-of-network providers. This can be particularly burdensome for individuals with chronic conditions or those requiring ongoing medical care. In some cases, patients may even be denied coverage altogether if they seek treatment from a provider outside of their insurance network.

The limitations imposed by insurance networks also extend to healthcare providers themselves. Doctors and facilities may be incentivized to join insurance networks in order to attract more patients, but this can come at the cost of reduced autonomy and control over their practice. Providers may be subject to strict guidelines and protocols set by the insurance company, which can limit their ability to provide personalized care to their patients.

In addition, network restrictions can contribute to healthcare disparities, as patients in underserved areas may have even fewer options for in-network providers. This can exacerbate existing inequalities in access to healthcare, particularly for low-income and minority populations. For instance, a study by the Commonwealth Fund found that 40% of adults in low-income households reported difficulty finding a primary care provider within their insurance network.

Ultimately, the limitations imposed by insurance networks on healthcare provider choices can have far-reaching consequences for both patients and providers. While insurance networks may help to control costs and streamline administrative processes, they also have the potential to compromise the quality and accessibility of healthcare services. As such, it is important to carefully consider the trade-offs associated with network restrictions and to explore alternative models for healthcare delivery that prioritize patient choice and provider autonomy.

Travel Medical Insurance: Top Companies for Your Trip

You may want to see also

Explore related products

![]()

Pre-Existing Conditions: Addressing how insurance companies handle coverage for individuals with pre-existing health issues

Individuals with pre-existing health conditions often face significant challenges when seeking health insurance coverage. Insurance companies may deny coverage, charge higher premiums, or impose waiting periods before covering pre-existing conditions. This can leave individuals with pre-existing conditions vulnerable to financial hardship and inadequate healthcare.

The Affordable Care Act (ACA) aimed to address these issues by prohibiting insurance companies from denying coverage or charging higher premiums based on pre-existing conditions. However, the ACA's effectiveness in addressing these issues has been limited by factors such as state-level resistance, legal challenges, and the Trump administration's efforts to undermine the law.

One potential solution to the problem of pre-existing conditions is the creation of high-risk pools. High-risk pools are insurance programs designed specifically for individuals with pre-existing conditions. These programs can help to spread the cost of healthcare among a larger group of individuals, making it more affordable for those with pre-existing conditions.

Another potential solution is the implementation of guaranteed issue policies. Guaranteed issue policies require insurance companies to offer coverage to all individuals, regardless of their health status. This can help to ensure that individuals with pre-existing conditions have access to affordable healthcare.

Ultimately, addressing the issue of pre-existing conditions requires a multifaceted approach that includes policy changes, increased awareness, and advocacy efforts. By working together, we can help to ensure that all individuals have access to affordable, quality healthcare, regardless of their health status.

Medical Insurance Claims: Which Lawyer to Call?

You may want to see also

![]()

Preventive Care and Wellness Programs: Evaluating the effectiveness of insurance-sponsored programs in promoting health and preventing illness

Insurance-sponsored preventive care and wellness programs aim to promote health and prevent illness, potentially reducing healthcare costs in the long run. However, evaluating their effectiveness is crucial to determine if these programs truly deliver on their promises. Studies have shown that such programs can lead to improved health outcomes, such as reduced blood pressure, cholesterol levels, and smoking rates. Additionally, they may increase the use of preventive services like vaccinations and cancer screenings.

One unique angle to consider is the impact of these programs on mental health. With the rising awareness of mental health issues, insurance companies are increasingly incorporating mental wellness initiatives into their preventive care offerings. These programs may include stress management workshops, mindfulness training, and access to mental health professionals. Evaluating the effectiveness of these mental wellness programs is essential to understand their role in overall health promotion.

Another aspect to explore is the accessibility and utilization of preventive care services among different demographic groups. Research has shown that disparities exist in the use of preventive services, with certain populations, such as low-income individuals and racial minorities, being less likely to access these services. Insurance-sponsored programs may help bridge these gaps by providing targeted outreach and incentives for preventive care.

When analyzing the effectiveness of these programs, it is important to consider the return on investment (ROI) for insurance companies. While preventive care may lead to improved health outcomes, it may also result in increased upfront costs for insurers. A thorough evaluation should assess whether the long-term benefits of preventive care outweigh the initial expenses.

In conclusion, preventive care and wellness programs sponsored by insurance companies have the potential to promote health and prevent illness. However, a nuanced evaluation is necessary to understand their true effectiveness, particularly in addressing mental health and reducing healthcare disparities. By examining the ROI and accessibility of these programs, we can determine if they are a valuable component of health insurance or if they fall short of their intended goals.

Insurance Records: Past Medications Accessible to Doctors?

You may want to see also

Frequently asked questions

Health insurance isn't necessarily worthless if you're young and healthy. While you may not need extensive medical care now, having insurance can protect you from unexpected illnesses or accidents. Plus, many policies offer preventive care benefits that can help you maintain your health.

If you can't afford health insurance premiums, it's important to explore your options. You may qualify for subsidies or financial assistance to help make insurance more affordable. Additionally, some policies offer lower premiums with higher deductibles, which can make them more budget-friendly.

Health insurance can be especially important if you have a pre-existing condition. Many policies cover treatment for pre-existing conditions, and having insurance can help you manage your health and avoid costly medical bills.

Health insurance is often crucial for retirees, as it can help cover the costs of medical care that may increase with age. Medicare and other retiree health insurance options can provide valuable coverage and peace of mind.

As a self-employed individual, you may not have access to employer-sponsored health insurance, but that doesn't mean you should go without coverage. There are many individual health insurance plans available that can provide you with the protection you need.