When considering the merits of health savings versus health insurance, it's essential to weigh the benefits and drawbacks of each approach. Health savings accounts (HSAs) and similar savings vehicles offer individuals a way to set aside money for medical expenses on a tax-advantaged basis, providing flexibility and control over healthcare spending. On the other hand, health insurance plans offer protection against high medical costs and often include preventive care benefits. The choice between prioritizing health savings or insurance depends on factors such as one's financial situation, health status, and personal preferences. This discussion will delve into the advantages and disadvantages of each option to help individuals make informed decisions about their healthcare financial planning.

Explore related products

What You'll Learn

- Cost Comparison: Evaluate the long-term costs of health savings accounts versus traditional insurance premiums and out-of-pocket expenses

- Flexibility and Control: Discuss how health savings accounts offer more flexibility in choosing healthcare providers and managing healthcare expenses

- Tax Implications: Explore the tax advantages and disadvantages of health savings accounts compared to insurance, including contributions and withdrawals

- Risk Management: Analyze how health savings accounts and insurance differ in managing healthcare risks, such as chronic conditions or unexpected medical bills

- Long-term Planning: Consider the impact of health savings accounts on long-term financial planning, including retirement and estate planning

![]()

Cost Comparison: Evaluate the long-term costs of health savings accounts versus traditional insurance premiums and out-of-pocket expenses

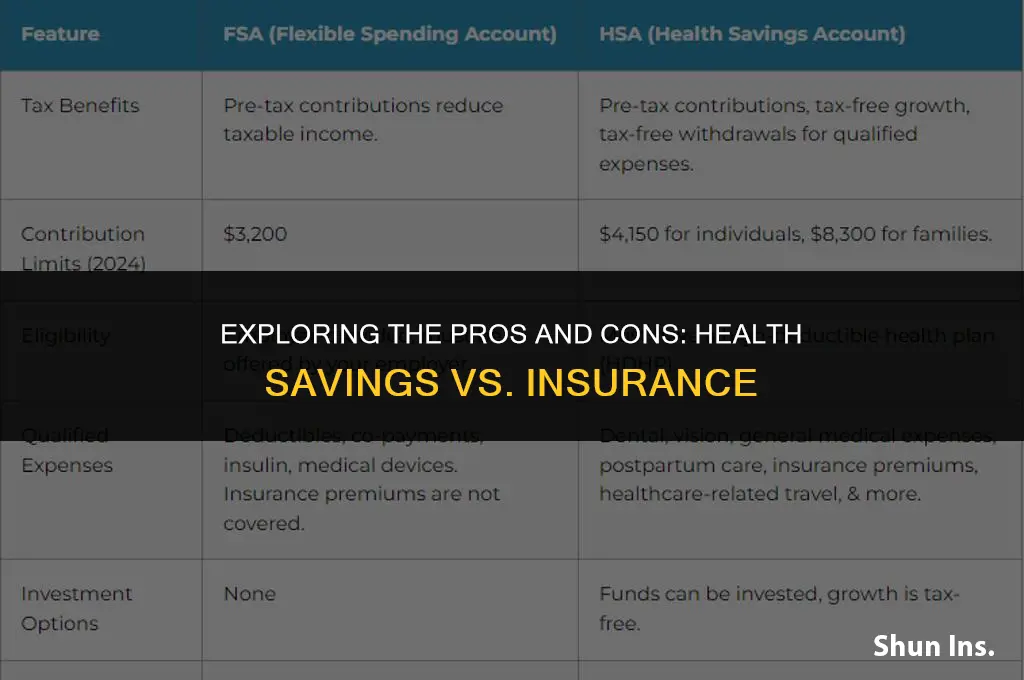

To evaluate the long-term costs of health savings accounts (HSAs) versus traditional insurance premiums and out-of-pocket expenses, it's essential to consider several factors. HSAs are tax-advantaged accounts that allow individuals to save money for qualified medical expenses. They are typically available to those who have a high-deductible health plan (HDHP) and are not enrolled in Medicare. Traditional insurance, on the other hand, involves paying premiums to an insurance company, which then covers a portion of medical expenses based on the policy terms.

One key advantage of HSAs is the potential for tax savings. Contributions to an HSA are tax-deductible, and the funds can be invested, allowing for potential growth over time. This investment aspect can make HSAs a more cost-effective option in the long run, especially for those who are healthy and do not incur many medical expenses. Additionally, HSAs offer flexibility, as the funds can be used for a wide range of qualified medical expenses, including deductibles, copays, and even some over-the-counter medications.

However, traditional insurance may be more suitable for individuals who anticipate high medical costs or have chronic conditions. Insurance plans often have negotiated rates with healthcare providers, which can result in lower out-of-pocket expenses for policyholders. Furthermore, insurance can provide financial protection against catastrophic medical events, which could otherwise lead to significant financial hardship.

When comparing the long-term costs, it's important to consider the individual's health status, the cost of premiums versus HSA contributions, and the potential for investment growth in an HSA. For those who are relatively healthy and can afford to contribute to an HSA, this option may offer significant cost savings over time. Conversely, for those with higher medical needs or who prefer the security of insurance coverage, traditional insurance may be the more cost-effective choice.

In conclusion, the decision between an HSA and traditional insurance depends on various factors, including individual health needs, financial situation, and long-term goals. A careful analysis of the costs and benefits of each option can help individuals make an informed decision that best suits their circumstances.

Does Health Insurance Cover Lactation Consultants? What You Need to Know

You may want to see also

Explore related products

![]()

Flexibility and Control: Discuss how health savings accounts offer more flexibility in choosing healthcare providers and managing healthcare expenses

Health savings accounts (HSAs) provide a unique advantage in the realm of healthcare financing by offering unparalleled flexibility and control to account holders. Unlike traditional health insurance plans that often come with rigid provider networks and predefined coverage limits, HSAs empower individuals to make personalized healthcare decisions based on their specific needs and preferences.

One of the primary ways HSAs offer flexibility is by allowing account holders to choose any qualified healthcare provider, without being restricted to a particular network. This means that individuals can seek care from specialists, primary care physicians, or alternative healthcare practitioners of their choosing, without worrying about whether they are in-network or out-of-network. Additionally, HSAs enable account holders to pay for a wide range of qualified medical expenses, including deductibles, copays, and even some over-the-counter medications, giving them greater control over how they allocate their healthcare funds.

Another significant benefit of HSAs is their ability to help individuals manage their healthcare expenses more effectively. By setting aside pre-tax dollars in an HSA, account holders can reduce their taxable income, which can lead to lower tax liabilities. Furthermore, HSAs often come with investment options, allowing account holders to grow their savings over time, tax-free. This can be particularly advantageous for individuals who are looking to save for future healthcare expenses or who want to have a financial cushion in case of unexpected medical costs.

In conclusion, HSAs offer a level of flexibility and control that is not typically found in traditional health insurance plans. By allowing account holders to choose their own healthcare providers and manage their healthcare expenses more effectively, HSAs can be a valuable tool for individuals looking to take a more proactive approach to their healthcare financing.

Why Insurance Premiums Rise: Understanding Rate Hikes and Their Causes

You may want to see also

Explore related products

![]()

Tax Implications: Explore the tax advantages and disadvantages of health savings accounts compared to insurance, including contributions and withdrawals

Health Savings Accounts (HSAs) offer a unique tax advantage over traditional health insurance. Contributions to an HSA are tax-deductible, reducing your taxable income for the year. This can be particularly beneficial for those in higher tax brackets. Additionally, the funds in an HSA grow tax-free, similar to a retirement account, allowing for significant long-term savings.

However, there are also potential tax disadvantages to consider. If you withdraw funds from an HSA for non-qualified medical expenses, you may face a 20% penalty in addition to paying taxes on the withdrawn amount. This penalty can be waived if you are over 65 or have certain disabilities, but it's a significant consideration for younger account holders.

Compared to health insurance, HSAs offer more control over your healthcare spending. With an HSA, you can choose how much to contribute and how to invest your funds, potentially leading to higher returns than the premiums paid into an insurance plan. However, insurance provides a level of protection against catastrophic medical expenses that an HSA may not cover, especially if you have a high-deductible plan.

When considering the tax implications, it's essential to evaluate your individual financial situation and healthcare needs. If you have a high-deductible health plan and are looking to save for future medical expenses, an HSA can be a valuable tool. However, if you anticipate needing to withdraw funds frequently for non-qualified expenses, the tax penalties may outweigh the benefits.

In conclusion, HSAs offer significant tax advantages, including tax-deductible contributions and tax-free growth. However, they also come with potential tax penalties for non-qualified withdrawals. When deciding whether an HSA is better than insurance, it's crucial to consider your personal financial goals, healthcare needs, and the tax implications of each option.

Post-Obamacare Health Insurance Premium Hikes: Analyzing the Percentage Increase

You may want to see also

Explore related products

![]()

Risk Management: Analyze how health savings accounts and insurance differ in managing healthcare risks, such as chronic conditions or unexpected medical bills

Health savings accounts (HSAs) and insurance are two distinct tools for managing healthcare risks, each with its own strengths and weaknesses. HSAs are tax-advantaged accounts that allow individuals to save money for qualified medical expenses. They are typically used in conjunction with high-deductible health plans (HDHPs), which have lower premiums but higher out-of-pocket costs. Insurance, on the other hand, is a contract between an individual and an insurance company, where the insurer agrees to pay for certain medical expenses in exchange for regular premiums.

One key difference between HSAs and insurance is how they handle chronic conditions. HSAs can be used to pay for ongoing medical expenses, such as prescription medications or regular doctor visits, which can be particularly beneficial for individuals with chronic conditions. Insurance, however, may have limitations on coverage for certain chronic conditions or may require higher premiums for individuals with pre-existing conditions.

Another area where HSAs and insurance differ is in managing unexpected medical bills. HSAs can provide a financial cushion for individuals facing unexpected medical expenses, as the funds can be used to pay for qualified expenses at any time. Insurance, on the other hand, may have deductibles, copays, and coinsurance requirements that can leave individuals with significant out-of-pocket costs in the event of an unexpected medical bill.

When considering which option is better, it's important to evaluate individual needs and circumstances. For some, the flexibility and tax advantages of an HSA may be more beneficial, while others may prefer the predictable coverage and cost-sharing structure of insurance. Ultimately, a combination of both HSAs and insurance may provide the most comprehensive risk management strategy for healthcare expenses.

Does Tufts Health Insurance Cover Cologuard? A Comprehensive Guide

You may want to see also

Explore related products

![]()

Long-term Planning: Consider the impact of health savings accounts on long-term financial planning, including retirement and estate planning

Health savings accounts (HSAs) offer a unique advantage in long-term financial planning, particularly when it comes to retirement and estate planning. Unlike traditional insurance plans, HSAs allow individuals to save money tax-free for qualified medical expenses, which can be a significant benefit in the long run. As people age, healthcare costs tend to increase, and having a dedicated fund for these expenses can help alleviate financial stress during retirement.

One of the key benefits of HSAs is their flexibility. Account holders can use the funds for a wide range of medical expenses, including deductibles, copays, and even long-term care costs. This flexibility can be especially valuable in retirement, when individuals may face a variety of healthcare needs. Additionally, HSAs can be used to pay for health insurance premiums, which can be a significant expense for retirees.

Another important aspect of HSAs is their potential for growth. Unlike traditional savings accounts, HSAs can be invested, allowing the funds to grow over time. This can be a powerful tool for long-term financial planning, as it can help individuals build a substantial nest egg for healthcare expenses. However, it's important to note that investing always carries some level of risk, and account holders should carefully consider their investment options and risk tolerance.

When it comes to estate planning, HSAs can also play a valuable role. Unlike other types of accounts, HSAs are not subject to probate, which means that the funds can be passed directly to beneficiaries without going through the court system. This can be a significant advantage for individuals who want to ensure that their healthcare funds are used as intended after their death. Additionally, HSAs can be used to pay for funeral expenses, which can be a significant burden for families.

In conclusion, health savings accounts offer a unique set of benefits for long-term financial planning, particularly in the areas of retirement and estate planning. By providing a tax-free way to save for healthcare expenses, HSAs can help individuals prepare for the financial challenges of aging and ensure that their healthcare needs are met without placing a burden on their loved ones.

Aetna Health Insurance Coverage for Hernia Repair: What You Need to Know

You may want to see also

Frequently asked questions

A Health Savings Account (HSA) is a tax-advantaged account that allows you to save money for qualified medical expenses. It is typically paired with a high-deductible health plan (HDHP). Traditional health insurance, on the other hand, usually covers a wider range of medical expenses but may come with higher premiums and deductibles. HSAs offer more control over your healthcare spending and can be a more cost-effective option for those with fewer medical needs.

Yes, there are several tax benefits associated with using a Health Savings Account. Contributions to an HSA are tax-deductible, and the earnings on the account grow tax-free. Additionally, withdrawals for qualified medical expenses are also tax-free. This makes an HSA a powerful tool for saving on healthcare costs while also reducing your taxable income.

Generally, you can only use Health Savings Account funds for qualified medical expenses without incurring taxes or penalties. However, after age 65, you can use the funds for any purpose without penalty, although you will still need to pay income tax on the withdrawals. It's important to note that using HSA funds for non-medical expenses before age 65 may result in a 20% penalty in addition to income tax.