Homeowners in Louisiana face unique challenges due to the state's vulnerability to hurricanes, storms, and flooding. As a result, homeowners insurance is a critical consideration for residents. While it is not mandatory, Louisiana's propensity for unpredictable weather events underscores the necessity for comprehensive coverage to protect homes and belongings. The state's insurance market has undergone legislative changes, with the recent repeal of the three-year rule, which restricted insurers' ability to cancel policies, and efforts to curb legal system abuse driving up insurance costs. Understanding the scope of coverage and rights as a policyholder is essential for Louisiana homeowners to make informed decisions about their protection in the event of natural disasters.

| Characteristics | Values |

|---|---|

| Homeowner's insurance required in Louisiana | Not explicitly mentioned, but it is highly recommended due to the state's vulnerability to unpredictable weather events and natural calamities like hurricanes, storms, and floods |

| Coverage | Physical structure, furniture, appliances, electronics, clothing, valuables (depending on the policy's terms and limits), liability component for medical/legal expenses |

| Additional coverages | Loss of Use Coverage (additional living expenses), Personal Liability Coverage, Medical Payments Coverage |

| Rights of homeowners | Right to a comprehensive coverage explanation, right to information and transparency from insurance providers |

| Insurance rate regulation | Recent legislative changes and tort reform bills passed to address high insurance rates and curb legal system abuse |

| House Bill 611 | Repealed Louisiana's three-year rule, allowing insurance companies more flexibility in managing risk and cancelling policies |

Explore related products

What You'll Learn

![]()

Louisiana homeowners insurance covers damage from hurricanes and floods

In Louisiana, homeowners insurance does not typically cover flood damage. Flood insurance is a separate policy that covers buildings, the contents within a building, or both. The National Flood Insurance Program (NFIP) provides flood insurance to property owners, renters, and businesses, helping them recover from flood damage. As of 2011, there were nearly 500,000 flood insurance policies in effect in Louisiana, with the NFIP assisting in defraying the cost of flood insurance.

Although homeowners insurance does not usually cover flood damage, it can provide coverage for hurricane damage. However, it is important to note that purchasing hurricane damage insurance does not guarantee that your claim will be accepted. Insurance companies may deny claims for various reasons, including insufficient coverage or disputes over whether the damage was directly caused by the hurricane. It is essential to carefully review your existing policies and consult with a hurricane damage lawyer to understand your coverage and rights in the event of a claim denial.

During hurricane season in Louisiana, it becomes challenging to obtain homeowners insurance. This is because insurers can delay paying out claims during this period. Nevertheless, it is advisable to prepare for the hurricane season by reviewing your policies and ensuring you have the necessary coverage.

To secure coverage for hurricane damage, it is recommended to consult with a lawyer specializing in this field. They can guide you through the process and advocate for your right to fair compensation. Taking immediate action when filing a claim is crucial, and a lawyer can assist you in navigating the complexities of the insurance system.

Farmers Insurance: Competitive Edge or Costly Coverage?

You may want to see also

Explore related products

![]()

Liability coverage includes medical and legal expenses

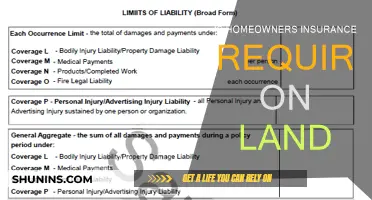

Homeowners insurance in Louisiana typically includes liability coverage, which can protect you from medical and legal expenses in certain situations. This coverage is designed to help you if someone is injured on your property and decides to sue. It can cover medical expenses for the injured person and legal fees if you are sued for negligence.

For example, if a guest slips on your icy driveway and breaks their leg, liability coverage would help cover their medical bills and any legal fees if they decided to take legal action. This type of coverage is crucial for homeowners, especially given the state's unpredictable weather and the risk of natural disasters such as hurricanes and storms, which can cause injuries and damage to your property.

It's important to understand the limits and exclusions of your liability coverage. While it typically covers medical expenses for injuries that occur on your property, there may be situations where the coverage does not apply. Additionally, the coverage limit sets a maximum amount that the insurance company will pay for a covered loss. It's crucial to review your policy carefully to understand what is included and excluded in your liability coverage.

In addition to liability coverage, homeowners insurance in Louisiana typically includes other types of coverage, such as dwelling coverage, which protects against physical damage to the home's structure, and personal property coverage, which protects your belongings inside the home. However, it's worth noting that basic homeowners insurance in Louisiana may not be sufficient for all property owners, especially considering the state's vulnerability to severe weather events. Many homeowners choose to supplement their standard coverage with additional policies for floods or windstorms to strengthen their overall protection.

Cosmetic Repair Insurance: Worth the Cost?

You may want to see also

Explore related products

![]()

Loss of use coverage includes temporary housing and meals

Homeowners in Louisiana face unique challenges due to the state's unpredictable weather and frequent natural calamities, such as hurricanes and floods. As a result, it is crucial for homeowners to have robust insurance policies that provide comprehensive coverage. While basic homeowners insurance policies may cover the physical structure and personal belongings, they may not be sufficient in the event of severe weather damage. Therefore, it is essential to understand the scope of your coverage and consider additional protections, such as flood or windstorm policies.

One important aspect of homeowners insurance in Louisiana is Loss of Use Coverage, also known as "additional living expenses." This type of coverage is typically included in standard homeowners insurance policies and provides financial assistance for temporary housing and meals if you cannot live in your home due to a covered loss. For example, if your home suffers fire damage and becomes uninhabitable, Loss of Use Coverage can help pay for the additional costs of staying in a hotel or renting an apartment during repairs.

Loss of Use Coverage generally covers expenses that exceed your normal living costs. It is designed to reimburse you for the additional expenses you incur when you are temporarily displaced from your home. This can include the cost of a hotel or temporary rental accommodation, as well as additional food expenses if you are unable to cook at home. For instance, if your home's kitchen is damaged and you need to eat out for most meals, Loss of Use Coverage can help offset the extra costs.

It's important to note that Loss of Use Coverage has limits, and policyholders should understand their coverage amounts. The coverage limit for Loss of Use Coverage is typically set as a percentage of your dwelling coverage limit. For example, if your dwelling coverage limit is $200,000 and your Loss of Use Coverage limit is 30%, you would be covered for up to $60,000 in additional living expenses. Policyholders can usually increase their coverage limit by paying an additional cost.

In conclusion, Loss of Use Coverage is an essential component of homeowners insurance in Louisiana, providing financial assistance for temporary housing and meals when policyholders are unable to live in their homes due to covered losses. By understanding the scope of their coverage and the available protections, homeowners can ensure they have the necessary support to recover from unexpected damage caused by severe weather events or other disasters.

Insuring Your Home: A Must or a Choice?

You may want to see also

Explore related products

![]()

Home insurance in Louisiana is expensive

The cost of home insurance in Louisiana can vary depending on several factors, including the age and construction materials of the home, as well as the coverage limits and deductible amounts selected. Homes built with materials that are more resistant to perils, such as fire, or those that are newly constructed, tend to have lower premiums. Additionally, the location of the property plays a significant role, with coastal regions that are prone to hurricanes and flooding having higher average rates than inland areas.

The insurance provider also impacts the premium, with the difference between the lowest and highest premiums offered by different companies reaching $8,076 on average. Homeowners with poor credit scores pay significantly more for their insurance, with an average annual premium of $7,519, while those with excellent credit pay around $3,577. It is worth noting that rates may also fluctuate over time, and comparing insurers can help homeowners find more affordable options.

To ensure adequate protection, Louisiana homeowners often supplement their standard insurance policies with additional coverage for floods or windstorms due to the state's propensity for severe weather. This includes Loss of Use Coverage, which covers additional living expenses incurred if the insured property becomes uninhabitable due to a covered loss, and Personal Liability Coverage, which covers legal expenses in the event of a negligence lawsuit. Given the high costs and complexities of home insurance in Louisiana, it is crucial for homeowners to understand their coverage scope and rights as policyholders.

Home Insurance: The True Cost of Peace of Mind

You may want to see also

Explore related products

![]()

Louisiana's three-year rule for insurance companies has been repealed

Louisiana is no stranger to hurricanes and storms, which can cause flooding and other types of damage. This makes homeowners insurance particularly important in the state. A basic homeowners insurance policy in Louisiana may not be enough for every homeowner, as it often makes sense to add flood or windstorm policies for additional protection.

Louisiana's insurance market has been operating under certain laws that are now being repealed. The state has some of the highest property insurance premiums in the nation. This is due to an increase in the frequency and strength of hurricanes, which has also led some of the largest insurers to stop offering policies in coastal areas or areas below Interstate 10.

Louisiana's three-year rule, a consumer protection law adopted in the early 1990s, prohibits insurance companies from raising deductibles, cancelling, or not renewing homeowner policies that have been in effect for more than three years. The rule was designed to protect consumers from arbitrary cancellations by insurance companies. However, some have argued that the rule has prevented insurance companies from managing their risk effectively and has contributed to high premiums. The rule already had some exceptions that allowed insurance companies to cancel policies that became too risky, such as in the case of a "material change in the risk being insured" or if renewing the policy "endangers the solvency of the insurer."

State lawmakers have recently voted to repeal the three-year rule, with nearly identical bills advancing in both the Senate and the House of Representatives. The new proposals would give the Louisiana insurance commissioner more power to approve mass policy cancellations. If the proposals are approved, insurers would be allowed to cancel up to 5% of their policies each year, provided they are not all in the same parish.

Home Insurance: Burst Pipes, What's Covered?

You may want to see also

Frequently asked questions

Yes, homeowners insurance is required in Louisiana. However, the specific requirements may vary depending on the policy and the insurance provider. It is important to carefully review the terms and conditions of your insurance policy to understand the extent of your coverage.

Homeowners insurance in Louisiana typically covers the physical structure of the home, as well as items such as furniture, appliances, electronics, and clothing. It may also include liability coverage for medical or legal expenses if someone is injured on your property or holds you responsible for their injuries. Additionally, due to the state's susceptibility to hurricanes and storms, many residents opt for supplemental coverage for flood or windstorm damage.

When choosing a homeowners insurance policy in Louisiana, it is essential to consider the unique risks associated with the state's unpredictable weather. Review the coverage limits, exclusions, and additional living expense provisions to ensure they meet your needs. Given the high insurance premiums in Louisiana, it is advisable to shop around and compare policies from multiple providers to find the most comprehensive coverage at a competitive price.

![[30 pcs] Lead Test Kit – Fast & Accurate Lead Paint Test Kit for Home – Lead Test Swab for Dishes, Ceramics and Any Surface – Quick and Easy Lead Test Swabs – Instant and Reliable Results](https://m.media-amazon.com/images/I/61m4I2mbbJL._AC_UL320_.jpg)