Health Reimbursement Arrangements (HRAs) are a type of health benefit plan that allows employers to reimburse employees for their medical expenses. Unlike traditional health insurance plans, HRAs are not tiered, meaning they do not have different levels of coverage or benefits. Instead, HRAs typically cover all eligible medical expenses up to a predetermined limit. This can include doctor visits, prescription medications, and other healthcare costs. HRAs are often used in conjunction with high-deductible health plans (HDHPs) to help employees cover their out-of-pocket expenses. Because HRAs are not tiered, they can provide more flexibility and simplicity for employees when it comes to managing their healthcare costs.

Explore related products

What You'll Learn

- Eligibility Criteria: Requirements to qualify for HRA tiered benefits health insurance

- Coverage Levels: Different tiers of coverage available under HRA health insurance

- Premium Costs: Cost implications for each tier of HRA health insurance benefits

- Claim Process: Steps to file a claim under HRA tiered health insurance

- Provider Network: Healthcare providers and facilities included in HRA's network

![]()

Eligibility Criteria: Requirements to qualify for HRA tiered benefits health insurance

To qualify for HRA tiered benefits health insurance, individuals must meet specific eligibility criteria set by the insurance provider. These criteria typically include factors such as age, income, employment status, and health condition. For instance, some HRA plans may require applicants to be under a certain age or to have a minimum income level to ensure they can afford the premiums. Employment status is another crucial factor, as many HRA plans are designed for full-time employees or those who meet certain work hour requirements. Additionally, health condition plays a significant role, with some plans imposing restrictions or additional premiums for individuals with pre-existing conditions.

The eligibility criteria for HRA tiered benefits health insurance can vary widely among different providers and plans. Some may offer more lenient terms, such as lower income thresholds or broader age ranges, while others may have stricter requirements. It is essential for individuals to carefully review the eligibility criteria of each plan they are considering to ensure they meet the necessary qualifications. Failure to meet these criteria could result in denial of coverage or higher premiums, which could make the insurance less affordable or even inaccessible.

One unique aspect of HRA tiered benefits health insurance is the tiered structure itself, which can impact eligibility. Higher tiers often come with more comprehensive coverage but also have higher premiums and may require individuals to meet more stringent eligibility criteria. Conversely, lower tiers may have more relaxed eligibility requirements but offer less coverage. This tiered approach allows individuals to choose a plan that best fits their needs and budget, provided they meet the eligibility criteria for their desired tier.

Navigating the eligibility criteria for HRA tiered benefits health insurance can be complex, especially for those who are new to the insurance market or have unique circumstances. It is advisable for individuals to seek guidance from insurance professionals or to use online resources to compare different plans and their eligibility requirements. By doing so, they can make informed decisions and find a plan that provides the necessary coverage while also being financially feasible.

In conclusion, understanding and meeting the eligibility criteria is a critical step in obtaining HRA tiered benefits health insurance. By carefully reviewing the requirements and seeking guidance when needed, individuals can increase their chances of securing affordable and comprehensive health coverage that meets their specific needs.

Top-Rated Insurance Companies: Who Leads the Industry Overall?

You may want to see also

Explore related products

![]()

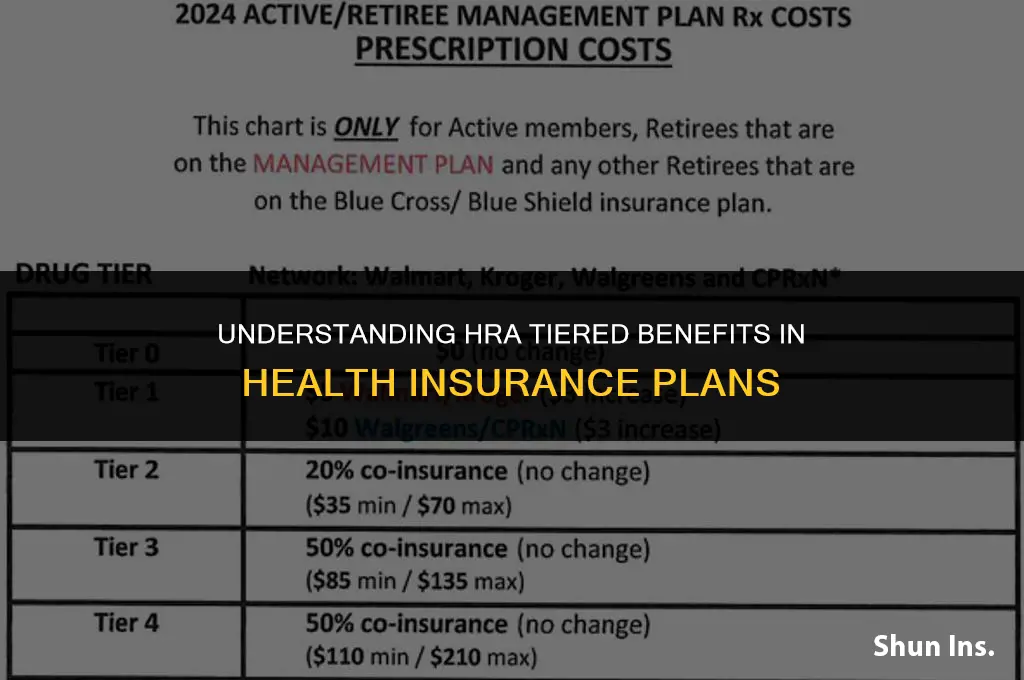

Coverage Levels: Different tiers of coverage available under HRA health insurance

Under the Health Reimbursement Arrangement (HRA) health insurance, coverage levels are structured into different tiers to cater to the diverse needs of policyholders. These tiers typically include Basic, Standard, and Premium plans, each offering a unique combination of benefits and cost-sharing arrangements. The Basic plan usually provides essential coverage with higher out-of-pocket costs, making it suitable for individuals seeking affordable premiums. In contrast, the Standard plan offers a balanced mix of coverage and cost-sharing, appealing to those who want comprehensive benefits without excessive premium costs. The Premium plan, on the other hand, provides the most extensive coverage with lower out-of-pocket expenses, ideal for policyholders willing to pay higher premiums for enhanced benefits.

One of the key advantages of HRA's tiered benefits structure is its flexibility, allowing policyholders to choose a plan that aligns with their specific healthcare needs and budget constraints. This tiered approach enables individuals to customize their coverage based on factors such as age, health status, and anticipated medical expenses. For instance, younger and healthier individuals may opt for the Basic plan to save on premiums, while older or those with chronic conditions might prefer the Premium plan for its more comprehensive coverage.

Moreover, HRA health insurance plans often include additional features such as prescription drug coverage, dental and vision care, and wellness programs, which may vary across different tiers. Policyholders can further tailor their plans by selecting optional riders or add-ons to enhance their coverage. This flexibility not only empowers individuals to make informed decisions about their healthcare but also helps them optimize their insurance costs.

When selecting an HRA health insurance plan, it is crucial to carefully evaluate the coverage levels and associated costs to ensure that the chosen tier meets one's healthcare needs without causing undue financial strain. Policyholders should consider factors such as premium costs, deductibles, copayments, and coinsurance rates when comparing different tiers. Additionally, understanding the plan's limitations, exclusions, and waiting periods is essential to avoid unexpected expenses and ensure seamless access to healthcare services.

In conclusion, the tiered benefits structure of HRA health insurance offers policyholders a range of coverage options to suit their individual needs and preferences. By carefully assessing the different tiers and their associated benefits and costs, individuals can make informed decisions about their healthcare coverage, ensuring that they receive the necessary protection without overburdening their finances.

Animal-Assisted Therapy: Impact on Home Insurance Policies

You may want to see also

Explore related products

![]()

Premium Costs: Cost implications for each tier of HRA health insurance benefits

The premium costs associated with HRA tiered benefits health insurance can vary significantly depending on the tier selected. Generally, the higher the tier, the more comprehensive the coverage, and consequently, the higher the premium. For instance, a basic tier might cover only essential health services with a lower premium, while a premium tier could include additional benefits such as dental, vision, and wellness programs, resulting in a higher cost.

When evaluating the cost implications, it's crucial to consider not only the monthly premium but also other out-of-pocket expenses such as deductibles, copayments, and coinsurance. These costs can add up quickly and impact the overall affordability of the insurance plan. For example, a plan with a lower premium might have a higher deductible, meaning the insured individual will pay more upfront before the insurance coverage kicks in.

Employers offering HRA tiered benefits health insurance may subsidize a portion of the premium costs, which can help make the higher tiers more affordable for employees. However, the extent of this subsidy can vary, and employees should carefully review their employer's contribution before selecting a tier. Additionally, individuals purchasing HRA tiered benefits health insurance independently will need to budget for the full premium cost without any employer assistance.

It's also important to consider the long-term financial implications of choosing a particular tier. While a higher premium tier may offer more comprehensive coverage, it might also lead to higher overall healthcare costs if the individual does not utilize the additional benefits. Conversely, selecting a lower premium tier could result in lower immediate costs but may leave the individual vulnerable to higher out-of-pocket expenses in the event of a major health issue.

To make an informed decision about which tier of HRA tiered benefits health insurance to select, individuals should carefully assess their healthcare needs, budget, and risk tolerance. This may involve consulting with a healthcare professional or a financial advisor to determine the most cost-effective option. By weighing the premium costs against the potential benefits and risks, individuals can choose a plan that best suits their unique circumstances.

Does Bay County, Florida Offer Shop Marketplace Health Insurance?

You may want to see also

Explore related products

![]()

Claim Process: Steps to file a claim under HRA tiered health insurance

To file a claim under HRA tiered health insurance, you must first understand the specific steps involved in the process. This type of insurance typically requires you to follow a tiered system, where you must first meet certain criteria or thresholds before moving on to the next level of coverage. Here's a step-by-step guide to help you navigate the claim process:

- Review your policy: Before filing a claim, it's essential to review your HRA tiered health insurance policy to understand the specific requirements and thresholds for each tier. This will help you determine which tier your claim falls under and what documentation you'll need to provide.

- Gather necessary documentation: Depending on the tier your claim falls under, you may need to provide various documents, such as medical bills, receipts, or proof of income. Make sure to gather all the necessary documentation before submitting your claim to avoid delays or denials.

- Submit your claim: Once you have all the necessary documentation, you can submit your claim to the insurance provider. This can typically be done online, through a mobile app, or by mail. Make sure to follow the specific submission instructions provided by your insurance provider to ensure your claim is processed correctly.

- Wait for processing: After submitting your claim, you'll need to wait for the insurance provider to process it. This can take several days or weeks, depending on the complexity of your claim and the volume of claims being processed.

- Appeal if necessary: If your claim is denied or you're not satisfied with the outcome, you may need to appeal the decision. This typically involves submitting additional documentation or providing further explanation to support your claim. Make sure to follow the specific appeal process outlined by your insurance provider.

By following these steps, you can ensure that your claim under HRA tiered health insurance is filed correctly and processed efficiently. Remember to always review your policy and gather all necessary documentation before submitting your claim to avoid any potential issues.

Understanding the Consequences: Health Insurance Penalty Calculator Explained

You may want to see also

![]()

Provider Network: Healthcare providers and facilities included in HRA's network

The provider network is a critical component of any Health Reimbursement Arrangement (HRA), as it determines the range of healthcare services and facilities available to participants. In the context of tiered benefits health insurance, the provider network plays an even more significant role, as it can directly impact the level of coverage and reimbursement for different types of medical care. Tiered benefit plans typically categorize healthcare providers into different tiers based on their quality, cost, and other factors, with higher tiers offering more comprehensive coverage and lower out-of-pocket costs for participants.

When evaluating an HRA's provider network, it's essential to consider the breadth and depth of the network, as well as the criteria used to tier providers. A broad network ensures that participants have access to a wide range of healthcare options, while a deep network provides multiple choices within a specific geographic area. The tiering criteria should be transparent and based on objective measures, such as quality ratings, patient satisfaction scores, and cost-effectiveness. This helps to ensure that participants are incentivized to choose high-quality, cost-effective providers, which can lead to better health outcomes and lower overall healthcare costs.

In addition to the provider network's structure, it's also important to consider the administrative aspects of the HRA. This includes the process for adding or removing providers from the network, the frequency of network updates, and the availability of online tools or resources to help participants navigate the network. A well-managed provider network can help to streamline the reimbursement process, reduce administrative burdens on participants, and improve overall satisfaction with the HRA.

Finally, when comparing different HRA options, it's crucial to look beyond the provider network and consider other factors, such as the plan's overall cost, the level of participant control over healthcare decisions, and the availability of additional benefits or features. By taking a holistic approach to evaluating HRA options, participants can make informed decisions that best meet their individual healthcare needs and preferences.

Understanding Medical Insurance Coverage After Gaining Employment

You may want to see also

Frequently asked questions

HRA tiered benefits health insurance is a type of health insurance plan that offers different levels of coverage and benefits based on the tier selected. Each tier typically has a different premium cost, with higher tiers offering more comprehensive coverage.

The tiers in HRA tiered benefits health insurance work by categorizing benefits into different levels. For example, a basic tier might cover essential services like doctor visits and prescriptions, while a higher tier might include additional benefits like dental, vision, and wellness programs.

The advantages of HRA tiered benefits health insurance include flexibility in choosing the level of coverage that best fits an individual's needs and budget. It also allows for customization of benefits, so individuals can select the specific types of coverage they require.

One potential disadvantage of HRA tiered benefits health insurance is that it can be complex to understand and navigate the different tiers and benefits. Additionally, individuals may end up paying more in premiums for higher tiers, which could be a financial burden for some.

HRA tiered benefits health insurance is similar to other types of health insurance plans in that it provides coverage for medical expenses. However, it differs in its tiered structure, which allows for more customization and flexibility in choosing benefits. Other plans, such as HMOs or PPOs, may have different structures and limitations on coverage.